Global| Feb 02 2009

Global| Feb 02 2009MFG PMIs Stop Their Descent

Summary

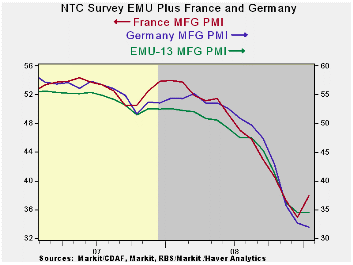

The PMIs for Europe reside very near the bottom of their respective ranges. Generally the readings are bottom 10% of range or less across large EMU members and the UK. Germany is now one of the relative weakest countries on this [...]

The PMIs for Europe reside very near the bottom of their

respective ranges. Generally the readings are bottom 10% of range or

less across large EMU members and the UK. Germany is now one of the

relative weakest countries on this measure – it is at its range low

point. Germany is one of four countries to see its MFG PMI drop further

in January.

PMIs: what they are:

PMIs are super sensitive gauges of activity. And they usually detect

turning points in a sector before more convention indicators do. The

MFG PMIs have only just stopped their declining ways for the EMU

region; for several countries the bottom has not yet been hit (as far

as we know). Even for those that have rebounded this month we do not

know with any degree of confidence that they have firmly put their past

low point behind them for the duration of this cycle.

Too soon for the end?

It is too soon to call this a turning point signal. But the first step

to getting to a turning point is to build a base that signals that the

PACE OF decline has bottomed out. Remember that these are diffusion

indices and even if they move ‘sideways’, as long as the value is below

50 it is signaling further declines in the sector they measure. Also

recall that PMIs are formally indicators of the breadth of a decline or

the breadth of an increase in industry; they are not indicators of

STRENGTH.

What about the beginning of the end?

It may also be too soon to look even for bottoming, but it may also be

that such a bottoming process has begun. The levels of the PMIs are

extremely low, and that is the sort of pace we would expect a true

stabilization process to begin at in a cycle such as this. We know MFG

is hard-hit so unless the PMIs reached very low readings we would

continue to think that worse results would still lay ahead. Now that a

first criterion for stabilization has been met (new all-time lows or

readings near to that) we can look for a second, namely a period of

time in which the PMIs either make modest gains or establish a base by

moving sideways. The final step would be for them to rise and

eventually to poke their heads above the level of 50. That one is still

quite a way off.

| NTC/Markit MFG Indices | |||||||

|---|---|---|---|---|---|---|---|

| Jan-09 | Dec-08 | Nov-08 | 3Mo | 6Mo | 12Mo | Percentile | |

| Euro-13 | 34.42 | 33.88 | 35.58 | 34.63 | 39.58 | 44.98 | 2.1% |

| Germany | 31.96 | 32.66 | 35.66 | 33.43 | 40.03 | 46.69 | 0.0% |

| France | 37.90 | 34.91 | 37.28 | 36.70 | 39.91 | 45.34 | 10.1% |

| Italy | 36.06 | 35.54 | 34.95 | 35.52 | 39.62 | 43.86 | 4.9% |

| Spain | 31.51 | 28.49 | 29.42 | 29.81 | 34.12 | 38.89 | 10.5% |

| Austria | 33.12 | 35.01 | 38.26 | 35.46 | 40.74 | 45.43 | 0.0% |

| Greece | 39.98 | 40.96 | 42.25 | 41.06 | 45.77 | 49.44 | 0.0% |

| Ireland | 38.94 | 37.87 | 37.10 | 37.97 | 40.36 | 43.00 | 10.1% |

| Netherlands | 36.29 | 38.42 | 38.71 | 37.81 | 42.80 | 46.99 | 0.0% |

| EU | |||||||

| UK | 35.78 | 34.91 | 34.48 | 35.06 | 38.64 | 43.65 | 6.0% |

| percentile is over range since March 2000 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief