Global| Nov 03 2008

Global| Nov 03 2008MFG is HOW Weak? Worst Since at Least March 2000 Across Much of EMU

Summary

The e-Zone economy shrank by 0.2% in 2008-Q2 and further weakness lies ahead according to the EU Commission. The EU Commission issued a statement warning that “In 2009, the EU economy is expected to grind to a standstill.’ The [...]

The e-Zone economy shrank by 0.2% in 2008-Q2 and further weakness lies ahead according to the EU Commission. The EU Commission issued a statement warning that “In 2009, the EU economy is expected to grind to a standstill.’ The Commission forecasts tiny GDP declines for the Zone in Q4 2008 and in Q1 of 2009.

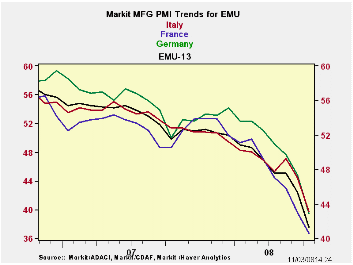

But the Markit PMI’s today seem to hint at the potential for deeper declines. MFG tends to be one of the more volatile sectors in recession so these PMIs, taken alone, overstate the case. The service sector holds up better and service sector employment typically holds up much better in recession in comparison to MFG. But both the Services and the MFG PMIs for Europe have been weak. The e-Zone has not experienced a recession since its formation. But as of September the EMU services PMI was in the bottom 12% of its range and now the MFG sector in EMU is the worst ever.

Sneezing in Frankfurt - Some might view the lack of recession since the region’s formation as an asset for the region, but to me, it’s another sign: it points out how poorly interconnected the various countries still are in EMU. It is not a sign of greater resilience - far form it. Europe’s economy is much less flexible than the US economy. One view is that a diversified area has been put together and since we add up GDP across the whole region it has become more stable than its individual parts. But that is a portfolio theory argument and the parts can only do this if they are not highly mutually correlated or less that fully integrated. So the lack of commonality proves the point of poor integration. Until someone can sneeze in Frankfurt and give someone a cold in Paris, Europe is fragmented.

The US is a much larger geographic and economic region and it is so connected that the region – even with its differences - experiences recessions. The resilience of EMU is yet another manifestation of how the region is not yet fully integrated. Workers within Europe are NOT indifferent as to whether they work in London, in Frankfurt or in Paris, or more broadly, the UK, Germany or France. Language and culture still separate European nations. Yet the downturn this time has such common themes that it is dragging even the disparate EMU into recession. That’s testament to the strength of the negative forces this time around.

Some Structural differences Persist: Not surprisingly, for Germany, France, Italy, Spain, Ireland and the UK, the average country level correlation with OVERALL EMU MFG is 0.86. For SERVICES it is a lower 0.82. Only in the UK and Ireland is the service sector better correlated with the EMU–wide measure than is the MFG index with its Europe-wide measure. That is probably due to the UK’s separate use of the pound in lieu of the euro and the faster impact on MFG flows than on services that FX rates exhibit. In the case of Ireland, the fact that Ireland is geographically more plugged into the UK economy and its cycles drives the rogue result. So it is basically the similarity in MFG that binds Europe together while Services differences largely persist across regions and tend to isolate euro-regions. This is in keeping with the way competition has been meted out within Europe and with the obviously more competitive nature of MFG with MFG anywhere – at least in comparison with services. Even with wide open competition in services, some services simply are local, like table service by a waiter at a restaurant, plumbing and electrician services on site and dry cleaning. Still, we know that some services that seem to be ‘intrinsically local’ have found ways to break down borders (ie video rentals delivered either over the internet or by mail instead of via the neighborhood store).

We will have to wait and see if the recession in Europe turns out to be as benign as the EU commission forecast suggests. The German finance ministry continues to tell how much better prepared Germany is to take this recession than other countries. Time will tell. I remain a Euro-skeptic.

| NTC MFG Indices | |||||||

|---|---|---|---|---|---|---|---|

| Oct-08 | Sep-08 | Aug-08 | 3Mo | 6Mo | 12Mo | Percentile | |

| Euro-13 | 41.10 | 44.97 | 47.55 | 44.54 | 46.79 | 49.50 | 0.0% |

| Germany | 42.88 | 47.36 | 49.68 | 46.64 | 49.49 | 51.81 | 4.6% |

| France | 40.59 | 42.97 | 45.79 | 43.12 | 46.19 | 49.52 | 0.0% |

| Italy | 39.67 | 44.42 | 47.07 | 43.72 | 45.24 | 47.72 | 0.0% |

| Spain | 34.60 | 38.32 | 42.40 | 38.44 | 39.82 | 43.94 | 0.0% |

| Austria | 43.44 | 46.01 | 48.61 | 46.02 | 47.20 | 50.09 | 0.7% |

| Greece | 48.14 | 50.81 | 52.46 | 50.47 | 51.77 | 52.37 | 5.3% |

| Ireland | 39.69 | 43.70 | 44.88 | 42.76 | 43.60 | 45.86 | 0.0% |

| Netherlands | 45.28 | 48.30 | 49.82 | 47.80 | 48.99 | 51.03 | 16.2% |

| EU | |||||||

| UK | 41.49 | 41.15 | 45.28 | 42.64 | 44.51 | 48.05 | 2.2% |

| Percentile is over range since March 2000 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief