Global| Jul 10 2014

Global| Jul 10 2014May Euro Area IP Takes a Battering across All Members; Does All This Weakness Mean Something?

Summary

Industrial production across the euro area has taken a hammering in May. It began with weaker than expected results from Germany, followed by unexpected weakness in Italy and then in France. All the early reporters of industrial [...]

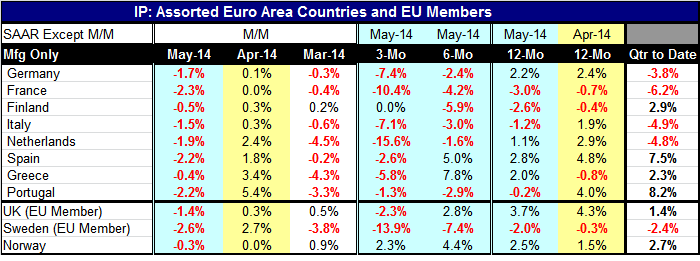

Industrial production across the euro area has taken a hammering in May. It began with weaker than expected results from Germany, followed by unexpected weakness in Italy and then in France. All the early reporters of industrial production data in the euro area are showing declines. Finland and Greece, two countries that have had ongoing and substantial weaknesses, show the smallest declines in industrial production in May. The largest declines are coming from France, Spain and Portugal. But Germany's 1.7% drop is not insignificant and it is supposed to be the strongest economy in the European Monetary Union, at least in the sense of being the most resilient.

Industrial production across the euro area has taken a hammering in May. It began with weaker than expected results from Germany, followed by unexpected weakness in Italy and then in France. All the early reporters of industrial production data in the euro area are showing declines. Finland and Greece, two countries that have had ongoing and substantial weaknesses, show the smallest declines in industrial production in May. The largest declines are coming from France, Spain and Portugal. But Germany's 1.7% drop is not insignificant and it is supposed to be the strongest economy in the European Monetary Union, at least in the sense of being the most resilient.

Outside of the EMU, we have declines as well with the UK, a country that has been showing substantial strength, joining in with another unexpected drop in industrial output with that index falling by 1.4% in May. Sweden and Norway round out the declines reported outside of the EMU.

When we look at trends, seven of these eight reporters have output declining over three months. The exception is Finland where output is flat. Over six months, only two of these countries fail to show declines in output, the exceptions being Spain and Greece. Over 12 months, the sample is split with four countries showing increases and four showing decreases in industrial output. Spain and Germany have the largest increases over 12 months, followed by Greece and the Netherlands. The biggest declines over 12 months come from France at -3%, followed by Finland, Italy and Portugal.

The declines of the most part are progressive as the 3-month pace is weaker than the 12-month pace for all these EMU members. But for declines in the Netherlands, Italy, France and Germany, growth rates are getting progressively worse on all shorter horizons from 12-month to 6-month to 3-month.

In addition to this unexpected weakening, we have an ongoing theme, the issue of France being so weak; it's not clear how the situation will be remedied. Over three months. France has the second-largest declines in industrial production exceeded only by the Netherlands. Over six months, France has the second largest declined exceeded only by Finland. Over 12 months, France's industrial production has the biggest decline of all.

We are two months into the second quarter. In the second quarter to date, once again we have a split sample of countries with four of them showing declines in output and four of them showing increases. Although the sample is split, strangely, all the growth rates are high in absolute value in the second quarter. The biggest decline in industrial production is from France at a -6.2% annual rate, followed by Italy at a -4.9% annual rate. The Netherlands is at a -4.8% annual rate and Germany at a -3.8% annual rate. These are substantial rates of decline. On the other hand, the countries with increasing industrial output are improving at a rapid pace. Portugal's output is still increasing at an 8.2% annual rate. Spain's is improving at a 7.5% annual rate, Finland's at a 2.9% annual rate and Greece's output is rising at a 2.3% annual rate.

The quarterly results are somewhat of an enigma since the May data and the trends are so much in line. Perhaps the quarter-to-date data will sort out more when the quarter finalizes the data in June. For the time being, we have the first, second and third largest EMU countries with substantial declines in industrial production in the quarter-to-date. Spain, the fourth largest country, has a significant increase but the country also has notoriously volatile data and that growth could be muted with next month's report.

On balance, this weakness in industrial production, coupled with other weaknesses that we've seen, have to make us wonder what's going on in Europe. Is Europe really losing its growth mojo? Have events in Ukraine had an outsized impact on trade, business and sentiment and is that being reflected in traditional growth statistics? Certainly, the diffusion indices for manufacturing and services have been showing some backtracking. When we reported the unexpected decline in Germany, it was a bit of a shock. But now a number of countries have fallen in line with their own surprises of the same sort. Germany also has weak export orders. In the data released today, the UK trade deficit widened and weak exports to Europe were one of the factors. Increasingly reports are coming to the same conclusion: the growth in Europe has weakened. However, interest rates in Europe already are low; for all intents and purposes, they cannot really go any farther. The European Central Bank has come to the party a bit late with policies trying to improve credit growth. But if economic activity is winding down, trying to stimulate the economy through credit growth incentives is like trying to bring a dead horse back to life with an electric cattle prod.

Interestingly, at the same time Europe has started to slow down, the United States has showed some speed up. Some of the US industrial data have shown some pickup and the US labor market over the last five months has produced over 1.2 million jobs for the first time in this cycle. However, US growth spurts have come and gone in the past. We can't be sure if the weakness in Europe is real or if the strength in the US is real. But it certainly appears as though there is change in the offing and enough that markets are undoubtedly going to be reacting to it.

While we can see that the ECB has a program in place, it's not clear that this program will be effective. On the US side, the Federal Reserve just released the minutes from its previous meeting in June. Apart from the end date for its quantitative easing program, the Fed doesn't seem sure of much of anything. There apparently are still some disagreements about how its new policy setting is going to work in this era with large bank reserves. In addition to questions about how the economy is performing, there are disagreements over what policy is likely to do next. In short, central banks don't appear to be much of a source of solace in this period of turbulence and uncertainty - all rhetoric to the contrary aside.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief