Global| May 06 2014

Global| May 06 2014Markit PMIs Show that Expansion Presses Onward

Summary

The services sector surveys for European economies and the US are completed today, allowing us to calculate total private sector indices for the various economies. The Markit index for the European Monetary Union moved up to 54.0 in [...]

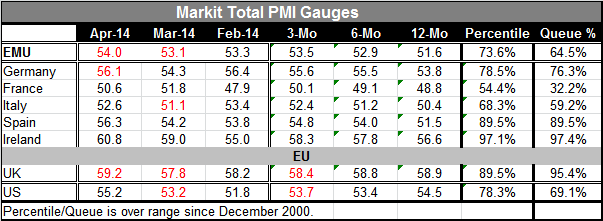

The services sector surveys for European economies and the US are completed today, allowing us to calculate total private sector indices for the various economies. The Markit index for the European Monetary Union moved up to 54.0 in April from 53.1 in March. This moves the EMU reading to the 64.5 percentile of its queue. This is a reasonably firm reading but still a moderate reading. Nor is it reading that indicates substantial momentum since the three-month average at 53.5 is only up from a six-month average of 52.9 and a 12-month average of 51.6. European recovery is moving ahead, but for the most part it is plodding ahead.

The services sector surveys for European economies and the US are completed today, allowing us to calculate total private sector indices for the various economies. The Markit index for the European Monetary Union moved up to 54.0 in April from 53.1 in March. This moves the EMU reading to the 64.5 percentile of its queue. This is a reasonably firm reading but still a moderate reading. Nor is it reading that indicates substantial momentum since the three-month average at 53.5 is only up from a six-month average of 52.9 and a 12-month average of 51.6. European recovery is moving ahead, but for the most part it is plodding ahead.

Looking at the various member countries, we see no declines month-to-month in the five EMU countries in the table. Among these countries Ireland has a strongest queue standing in the top 3% of its historic range. Spain's is in the top 11% of its historic range. Germany's is in the top 24% of its historic range. These numbers compare to poor readings in 59th percentile for Italy and to the extremely bottom-scraping 32nd percentile from France. The second and third largest countries in the EMU are just not in gear. Both of them have raw PMI readings in the top 50th percentile indicating expansion but clearly not much expansion.

The graph shows us the relative positions of the US using the composite ISM index versus the UK composite versus the EMU composite. Among these the US shows the least momentum with its index moving sideways since approximately 2010. The UK has the strongest up-thrust, but it is off-peak and now of uncertain momentum at this high level. The euro area's move up has been a little bit slower and later-coming than the US and the UK, but it shows the best ongoing momentum of the group.

The Euro Area's Retail Sales Challenge

Retail sales are recovering although struggling in the euro area. For all of the euro area retail sales are up by only 0.9% year-over-year while nonfood sales volumes are down by 0.1%. If the euro area is going to mount a successful recovery, it is going to have to get its domestic demand and retail sales in gear. While the performance of the private sector economy exhibited in the Markit overall private sector indices continues to show momentum, the domestic economy and retail sales are going to have to follow through.

For the whole of the euro area, growth and momentum still are not happening although growth in the recent three months is much more encouraging with total sales volumes up at a 5.6% annual rate and up at a 9.4% annual rate for nonfood volumes. Motor vehicle volumes are a much more encouraging, up at a 5.8% pace over 12 months and up at 8.8% annual rate over three months. Motor vehicle registrations also have solid growth in two of the three most recent months.

The country by country performance is somewhat erratic with sales declines in three of the seven most recent months in euro area countries. There are also declines in three of seven of these countries over six months but declines in only two of seven over 12 months. The countries with weak retail sales are France with declines over three months and six months. Italy shows declines over three months, six months and 12 months. Spain also has declines over three months, six months and 12 months. In the case of Italy, the declines are getting to be progressively steeper. That's true for France too. For Spain the pattern is not as progressively weak, but the most recent three month drop is a chilling -7.8% at an annual rate.

In order to keep the improvement in the Markit indices going forward, there will have to be more progress on the retail sales front. Europe cannot continue to build its growth on the back of foreign trade progress. The days are over when euro area members could fill in private sector weakness with public sector spending. Thus, as encouraging as the data are from the Markit PMI surveys, there remain some big question marks and huge hurdles to go over for Europe in terms of getting sustainable growth back on track. Even over three months when the euro arae retail sales growth numbers appear to be robust, there is simply too much erratic performance across key euro area members for that aggregate number to carry the day all the way to optimism.

While the Markit indices are closely watched and are important, it's important also to look beyond them especially to what I call `the real data' rather than survey data. Survey data find some ways to mimic the message of the real data. But we need to continue to look at the real reports on industrial production, retail sales and unemployment. Diffusion indices are much more `of the moment' and are concerned with current momentum. We continue to try to bring the PMI data back to earth by looking at the current values expressed as a percentile of their historic ranges. When we do that, we begin to see some of the flaws in the PMI approach. While Ireland and the UK are flying high in terms of the levels of the PMI readings and especially in terms of their PMIs placed in a historic context, it's quite clear that these two economies are still not performing well compared the past historic standards. PMI data are much more about momentum than they are about perspective. We are encouraged by the momentum in Europe, but we also see substantial issues that Europe will have to address in order to keep its PMI indices moving forward.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief