Global| Sep 03 2013

Global| Sep 03 2013Markit Manufacturing Indices for EMU and Europe Advance

Summary

This may not turn out to be a watershed month for Europe, or for the European Monetary Union, but the manufacturing PMIs for the countries listed in the table including some of the key countries from the economic union as well as in [...]

This may not turn out to be a watershed month for Europe, or for the European Monetary Union, but the manufacturing PMIs for the countries listed in the table including some of the key countries from the economic union as well as in the monetary union and Switzerland all are showing net improvements over three months. This is the first time since August 2009 that this is happened. It may simply be a bit of a statistical quirk, but clearly there has to be some pickup in activity across the region that has helped to raise all boats and over three-months on balance.

This may not turn out to be a watershed month for Europe, or for the European Monetary Union, but the manufacturing PMIs for the countries listed in the table including some of the key countries from the economic union as well as in the monetary union and Switzerland all are showing net improvements over three months. This is the first time since August 2009 that this is happened. It may simply be a bit of a statistical quirk, but clearly there has to be some pickup in activity across the region that has helped to raise all boats and over three-months on balance.

So that's the good news.

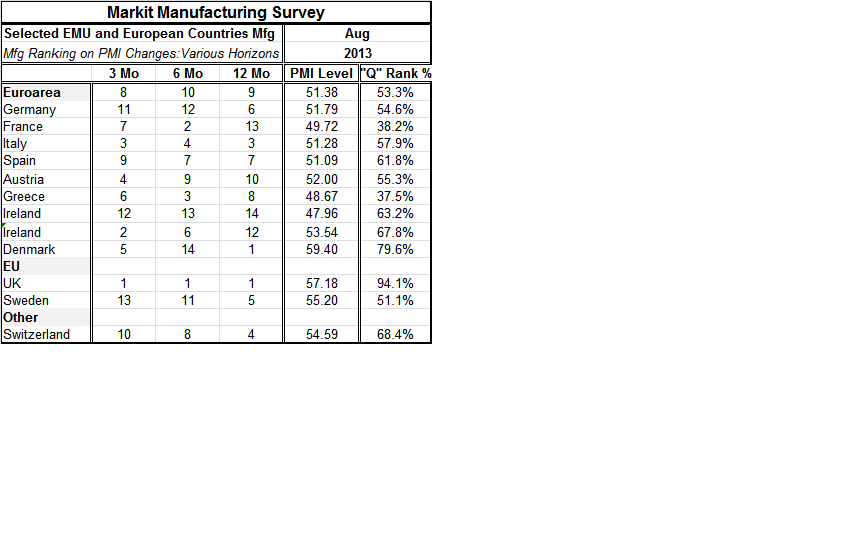

And of course it's always true that when an area has been hit by recession there will be a period of time when it will be recovering and its key economic metrics will still be weak-even as they recover. The table above shows the queue percentile rankings (labeled as "Q") and other growth diagnostics. The queue rankings evaluate the standing of the various PMI readings for the national manufacturing sectors, by placing each in a string of its own data back to October 2003. A number of EMU members now have firm readings that are above the 50% mark in terms of raw diffusion, and, in addition to that, many have queue rankings -or standings - that are above the 50th percentile of their range, which means that they above their midpoints.

Among monetary union members, only France, Greece and Ireland are below their 50 percentile levels in terms of their raw PMI indices. In the case of France it's barely below it at a level of 49.72. However, that reading for France is actually exceptionally low as the queue standing for France's 49.72 level is only in the 38th percentile of its historic queue of manufacturing readings. Germany's 51.79 is in the 54th percentile of its queue. For the whole EMU area we see PMI readings above 50 at 51.38. And for the euro-Areas a whole the queue ranking is in the 53rd percentile, indicating a moderate standing in its historic queue.

The EMU reading above 50 sends a message that manufacturing is expanding in the monetary union. The queue reading at the 53rd percentile tells us that it's a speed of expansion that clusters pretty close to the middle of the pack. Of course, that's an improvement compared to where it's been, but it's still not very strong.

The rankings in the table rank the changes by country or region over three months, six months and 12 months in the manufacturing diffusion index. What's clear from those rankings is that Germany is not leading the pack forward.

There are 13 economic units (12 countries and the Euro-area as a whole) in this group and Germany's net change in its manufacturing index ranks as 11 best over three months and 12th best over six months ;it's in the middle the packet at sixth-best over 12 months.

Over the most recent three months the leading contributors to growth in Europe have been the UK followed by Ireland and Italy. The laggards over three months have been Sweden, Ireland, Germany, and Switzerland. By contribution we are looking at the change in the manufacturing PMI not the level -and we are abstracting from formal weights, of course (Since Germany's weight is so large a sneeze that's in the positive direction could dominate a surge for Ireland).

Over six months the leaders in terms of changes in the manufacturing PMI levels have been the UK, France, Greece, and Italy. Over the same six months the smallest changes in the PMI indices have come from Ireland, Germany, Sweden and Austria (the euro-Area itself actually ranked 10th over six months).

It's clear from this information that the UK has been an exceptionally strong economy. It also has been the leader along with Denmark over 12 months. It's an economy, however, that continues to have a banking sector that it has to pay a great deal of attention to and, like the United States, it is benefiting from an extremely accommodative monetary policy.

Since much of the improvement in the euro-Zone comes from its countries that have lagged the most and been under the burden of austerity programs, it gives us pause. We have to wonder somewhat about whether it makes sense to have the train propelled by its caboose instead of buy its locomotive.

In a declaration issued just today the OECD has put its stamp of approval on the ongoing improvement in the most industrialized economies but has warned about ongoing difficulties in developing economies. Some have been looking back at this broad episode that has followed the financial crisis and pointed out that a number of developing economies have also been somewhat active and putting various trade restrictions in place. This sort of thing is common when growth slows and the size of the economic pie shrinks then is slower about growing and gaining back lost ground.

A large Japanese research house has today announced that it thinks that the Asian economies have passed their worst damage in this cycle. Since growth is still limping and China has a lot of adjusting yet to do I am wary of that declaration. Japan itself is still trying to find its way out of the woods.

The messages here I think are clear. There has been a good deal of improvement in Europe and its manufacturing level at least is back more in the range of normal. Still it's a very middling view of `normal' that we should associate more with the grade of "C" rather than "C+" or "B" or anything higher. Way too much `progress' has come to Europe in a somewhat unusual way as growth has been trickling up, instead of trickling down and this is going to be something to watch.

The German wise-man, Peter Bofinger, has warned that ongoing austerity in the periphery of the Zone is not going to be sustainable; he claims it already has created negative blowback effects for countries at the core of the European Monetary Union. In short while there is progress in Europe there continues to be a lot of risk. The OECD is wary of progress in developing economies but in fact we still have that special sauce of monetary policy being slopped over all of the economic indicators in the world's most industrialized and largest economies: United States, the UK and Japan and to some extent in EMU. We need to worry about these policies as well.

As the Fed is looking to pull back in its quantitative easing, it's an interesting time to think about how growth is going to be affected if other central banks follow the Fed's footsteps... especially if the Fed starts making new footsteps this month.

This is the key week for US economic data as the monthly employment report is on tap and the Fed's most important short-term gauge will be refreshed by the new employment release. The world as we have known it could be on the verge of changing and having to find some new areas of stimulus. Are we ready for it? Or is the incipient rise of protectionism a sign that we are not?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief