Global| May 03 2021

Global| May 03 2021Manufacturing PMIs Step Up and Step Out

Summary

The Markit PMIs rose on a broad basis this month. Although they had risen more broadly in the past, this month’s rise is impressive. What this month brings that is most compelling is a paucity of anything but episodic weakness (only [...]

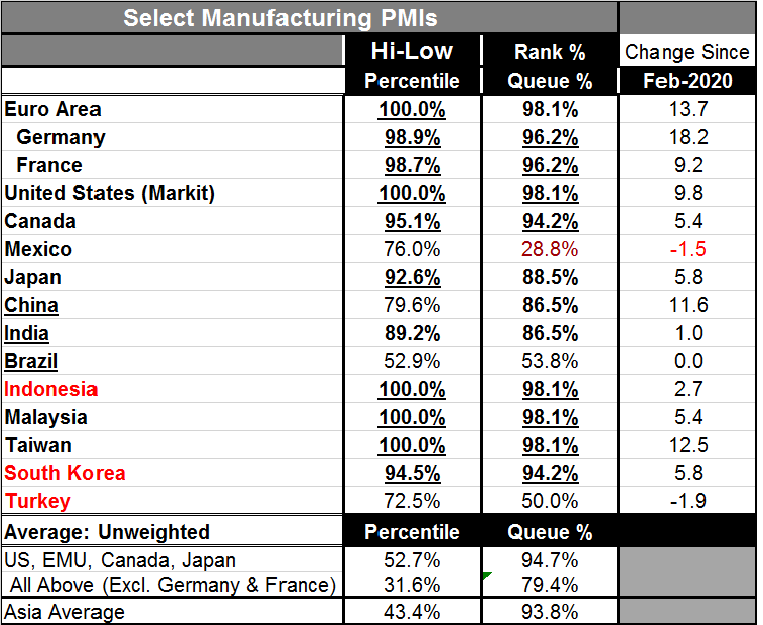

The Markit PMIs rose on a broad basis this month. Although they had risen more broadly in the past, this month’s rise is impressive. What this month brings that is most compelling is a paucity of anything but episodic weakness (only Mexico has a manufacturing reading below 50). Queue standings are impressive; they rank 9 of the table’s 15 readings in the top 10% of all readings since January 2007. Three other table entries have PMI queue standings is their upper 80th percentiles. Turkey and Brazil have rank standings at or barely above their respective medians while only Mexico is below its median with a queue standing in its 28.8 percentile.

The Markit PMIs rose on a broad basis this month. Although they had risen more broadly in the past, this month’s rise is impressive. What this month brings that is most compelling is a paucity of anything but episodic weakness (only Mexico has a manufacturing reading below 50). Queue standings are impressive; they rank 9 of the table’s 15 readings in the top 10% of all readings since January 2007. Three other table entries have PMI queue standings is their upper 80th percentiles. Turkey and Brazil have rank standings at or barely above their respective medians while only Mexico is below its median with a queue standing in its 28.8 percentile.

For the most part, the global manufacturing sector is on a really good run right now. This 15 reporter sample averages a PMI standing of 56.2 for all entries; that ranks as the best unweighted PMI score for this group of countries since at least December 2016. In addition, five of the reporters in this table are on period highs over the past 53 months. Another five are in the top ten percentile of all readings posted over those 53 months. This is a very strong batch of readings.

However, caution is still required of this analysis. For example, India’s manufacturing sector improved month-to-month rising to 55.5 from 55.4. But we know that country is having an extremely harsh outbreak of the virus, its hospitals are overrun and it has a life-threatening shortage of oxygen supplies. Despite India’s looking ‘pretty good’ in this grid format on manufacturing, in reality India is on the cusp of an economic breakdown. These data are a testament to how the manufacturing sector seems to have been able to separate itself from the virus woes. I still would not be confident that India will continue to report a robust figure next month. In fact, I would be quite surprised if it did.

The Baltic Dry Index shows the tremendous progress in global manufacturing and shipping made since December as well as the recent ramp up in late-April. The global economy is making a recovery even as the virus circulates and in some places still with great lethality. If all this does not confuse you, you are just not paying attention.

The Baltic Dry Index shows the tremendous progress in global manufacturing and shipping made since December as well as the recent ramp up in late-April. The global economy is making a recovery even as the virus circulates and in some places still with great lethality. If all this does not confuse you, you are just not paying attention.

We can draw a few, unfortunately conflicting conclusions here: (1) One is that the recovery is gaining pace and picking up momentum. (2) From the U.S. ISM manufacturing report today, we see evidence that manufacturing is running hot and yet encountering some bottlenecks that are nonetheless slowing progress. Yet, (3) progress is spreading internationally as we can see by the PMI readings this month. (4) And while the PMI readings are improving and strengthening, we can see there is still risk of infection spreading and it is unclear if that is still a risk for the more widely inoculated countries like the U.S. and the U.K. or if it is a problem that mostly is stalking the less inoculated developing economies. (5) In the U.S., the CDC seems to take an extreme position on the issue of how much inoculation is needed to reach the illusive concept of herd immunity. Of course, whatever the true proportion is, it gets higher the more easily the virus spreads. If mutations take it in that direction, at the extreme, all countries could be put back to square one. This is one of the concerns driving efforts to vaccinate the entire world population. No one can be sure what proportion of vaccination – short of 100%- will be safe.

So while this month we see a very encouraging set of readings for the manufacturing sector, the recovery is still not baked in the cake. And we do expect to see a similar if not stronger move to improvement out of the services PMI’s for April later this week. But all the progress remains at risk. It is probably not as much at risk in the most vaccinated countries, but then health officials are not taking any chances and they continue to make way in a slow step-wise fashion. The EU that still lags in vaccinations is already making plans to open up for tourism. Time will tell what speed of recovery can be sustained. One thing seems very clear and is that it will be a multispeed recovery. Some economies are ahead and will stay ahead. And that means there will be virus circulating in the slower recovering areas for some time to come even as the global economy steps up its pace and begins to look more normal. At this point, we still have a very incomplete picture of how to evaluate the risk from the virus. Have we, for the most part, passed by the worst of it, or does significant risk still linger?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief