Global| Nov 01 2017

Global| Nov 01 2017Manufacturing PMIs Show Some Slowing in October

Summary

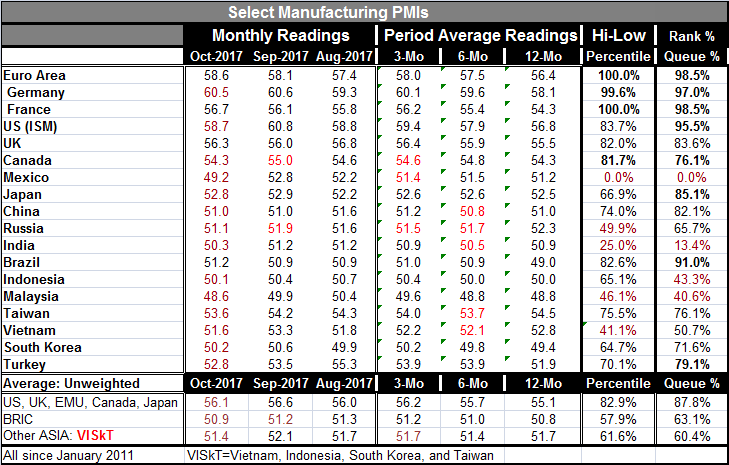

Of the 18 countries/regions in the table, 13 showed weaker readings in October than in September. However, only Mexico and Malaysia logged a manufacturing sector reading below 50 (indicating an outright contraction in output). There [...]

Of the 18 countries/regions in the table, 13 showed weaker readings in October than in September. However, only Mexico and Malaysia logged a manufacturing sector reading below 50 (indicating an outright contraction in output). There are eight readings at a level of 51.2 or lower in October, compared to only four in September and five in August.

Of the 18 countries/regions in the table, 13 showed weaker readings in October than in September. However, only Mexico and Malaysia logged a manufacturing sector reading below 50 (indicating an outright contraction in output). There are eight readings at a level of 51.2 or lower in October, compared to only four in September and five in August.

On an average basis, only three countries are weaker over three months than over six months with two others unchanged. Six months compared to 12-months shows five countries are weaker with two unchanged. Over both three-month and six-month, the average change in the unweighted manufacturing PMI reading from the earlier period is a gain of 0.4 points. Still, the shift from the three-month average to the October level shows declines in 13 countries with gains of only 0.2 elsewhere except in Europe where the EMU and France improved by 0.5 points and Germany improved by 0.4 points. That's a broad slowing.

There is an obvious loss in momentum and we see it across groups. Conditions are weaker month-to-month in the most developed nations in the BRIC group and for a cluster of Asian nations (VISkT). Each of these three groupings is weaker in October than its three-month average as well.

Still, the queue standings since January 2012 show that 5 countries stand in their top 10 percentile. And below that, three stand in their 80th percentile decile. Four stand in their 70th percentile decile. One stands in its 60th percentile decile and one stands in its 50th percentile decile. Only four lie below the 50th percentile that markets each country's median.

There are several clear points here. One is that the queue standings are high. Another is that there is still a loss in momentum. The third is that the loss in momentum is widespread.

The 90th percentile readings are clustered in Europe with another high 90th percentile reading for the United States. Oddly, at a low raw diffusion score of 51.2, Brazil also logs a 91st percentile queue ranking on this timeline, a testament to how weak it has been.

80th percentile readings encompass Japan, the U.K., and surprisingly, China whose high standing corresponds to a weak diffusion score of 51.0; another testament to a country making recovery from past weakness.

Readings in the 70th percentile decile include Canada, Taiwan, South Korea, and Turkey. Russia has the lone 60th percentile standing. Vietnam is the lone 50th percentile standing.

The below-50 crowd features Mexico at its weakest level ever (0 percentile) and India at its 13th percentile. Malaysia and Indonesia are at their respective 40th percentile standings.

This looks a lot like the result of a 'the rich get richer' paradigm. And it might well be, With Donald Trump in the U.S. on the warpath about trade, several things have happened.

* There is weaker growth out of Asian countries that rely on export-led growth. And Mexico, a NAFTA member (that is in the Trump cross-hairs), has been greatly affected.

* The developed economies that can better generate their own demand are now doing better.

* In the U.S., the manufacturing sector is showing unexpected life despite a stronger dollar and some of that might stem from the revived oil sector, but some seems to also be the result of Donald Trump putting firms on notice for switching jobs out of the U.S.

It does not seem to be a coincidence that countries/regions that generate their own domestic demand are doing better. Maybe tough talk on trade is bearing fruit? Economists have rather clumsily endorsed the idea that all trade is good and even perhaps the notion that unfair trade is better than less trade. But as Americans have lost jobs and Asia has grown, it has become clear that this is not true. Certainly, technology has been a factor too, but that does not explain why factories relocate in China- it does not have a lock on technology; it has lock on cheap labor, at least to a point. Relative wage costs and exchange rates do explain Asia's advantages.

As Donald Trump has targeted Mexico and NAFTA for change, the U.S. automakers have tried to slow him down saying that NAFTA works just fine...for them. And that's the point. NAFTA and other trade deals work well for the large, mobile, well capitalized, multinational corporations who can exploit and internalize international differences whether fairly gotten or not. But that does not work just fine for the American worker. If it's good for General Motors, it may NOT be good for America after all. If Ford or GM cars are being made in Mexico by Mexicans and exported to the U.S. under NAFTA, are U.S. workers less damaged than if Volkswagen does it? If Trump is trying to create jobs in America, he is focused on the effect of U.S. job growth not the nationality of the ownership of the firm that is doing business. Trump will want business done in the U.S. using U.S. labor, not just done by U.S. firms through their overseas subsidiaries. This will be something to watch as will the reactions of other nations.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief