Global| Aug 03 2015

Global| Aug 03 2015Manufacturing PMIs in July

Summary

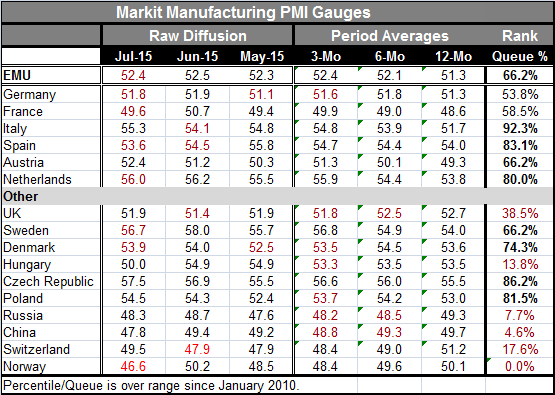

The manufacturing PMIs in the EMU show a monthly reduction in the PMI for the EMU as a whole and declines in four of six early reporters. Only France is showing manufacturing contraction in July. The EMU has a percentile standing at [...]

The manufacturing PMIs in the EMU show a monthly reduction in the PMI for the EMU as a whole and declines in four of six early reporters. Only France is showing manufacturing contraction in July.

The manufacturing PMIs in the EMU show a monthly reduction in the PMI for the EMU as a whole and declines in four of six early reporters. Only France is showing manufacturing contraction in July.

The EMU has a percentile standing at its 66th percentile, right at the border of the top third of its queue. Italy is in the top-eight percentile of its historic queue and Spain is in the top 17%.

The Netherlands stands in the 80th percentile of its historic queue and Austria is with the EMU at its 66th percentile. Germany is at its 53rd percentile and France at its 58th percentile. Both of these are quite moderate standings and disappointing for this stage of the cycle, with the euro exchange rate still so weak. Of course, EMU countries do a lot of intra-area trade where the exchange rate is not an issue and economic performance is poor.

The other section of the table shows a core of European nations with PMIs at or above 50 (U.K., Sweden, Denmark, Czech Republic, and Poland) plus two, Switzerland and Norway, with standings below 50. Russia stands at its 48th percentile with a queue standing of 7.7%. China is at 47.4% with a queue standing of 4.6% (weaker only 4.6% of the time). A number of Asian economies (not listed here) are still struggling.

Even among the European economies with PMIs at or above 50, there is weakness. Hungary, with a manufacturing PMI of 50.0, stands in its historic 13th percentile. The U. K., with a reading of 51.9, has a 38.5 percentile standing. The low percentile standing tells us that the PMI value, whatever it is, is weak by the historic standards of that nation.

The latest PMIs show four of six EMU results are lower in July while only 3 of 10 in the `other' group saw monthly erosion.

Sequential averages show an upward trend in the EMU, but an extremely mild one with the current month on top of the three-month average and the three-month average only 1.1 points higher than the 12-month average. France, despite its contracting, has an upward trend (though July is below its three-month average). Italy has a strong uptrend. Both Austria and the Netherlands are moving higher sequentially. Spain is steadily higher but has a July value below its three-month average and below its 12-month average. Has its improvement stopped? True momentum is hard to find.

Among the other countries, only Sweden and Czech Republic show momentum in their sequential averages.

The story of manufacturing in July is still an erratic one. The EMU gauge moved lower month-to-month despite an upward revision to its flash value. But within the EMU as well as in the selected countries outside of it, momentum is hard to find. Many countries with high percentile standings are doing well only by their own standards as there is only one PMI above 57 (Czech Republic). Globally, manufacturing is still struggling. China is stuck in a rut. And Chinese authorities are still playing shell games with Chinese stocks instead of fixing the fundamentals.

Upon the open today, the first trading allowed in five weeks, the Greek stock market fell by over 20%. While Greece has not been in the headlines, it is still a big thorn in the side of the EMU. It is now trying to make the EMU blink. Leaving the EMU is still a strong possibility for Greece, which posted its lowest manufacturing PMI level ever in today's report and will struggle whatever it does. There is no escape.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief