Global| Aug 01 2017

Global| Aug 01 2017Manufacturing PMIs Gain Some Traction in July But Also Show Divergences

Summary

The PMI readings for manufacturing in July are solid or rising in the countries whose economic leadership matters most. In Asia, China's manufacturing gauge is up to 51.1 in July from 50.4 in June. While Japan's gauge is lower, it is [...]

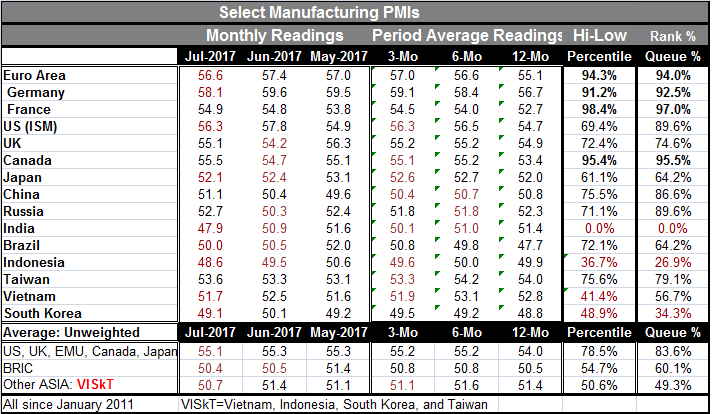

The PMI readings for manufacturing in July are solid or rising in the countries whose economic leadership matters most. In Asia, China's manufacturing gauge is up to 51.1 in July from 50.4 in June. While Japan's gauge is lower, it is still above 50 and in the 64th percentile of its historic queue of values. In Europe, the EMU gauge is lower but at a very solid 56.6 reading and is down from a multi-month high. Its current level logs a very strong 94th percentile standing in its own historic queue of data over the last five and one-half years. The U.S. (ISM) reading also works lower to a near 90th percentile standing. On balance, the global manufacturing signals remain strong this month for the countries that matter most. And that is what markets are going to react to most strongly.

The PMI readings for manufacturing in July are solid or rising in the countries whose economic leadership matters most. In Asia, China's manufacturing gauge is up to 51.1 in July from 50.4 in June. While Japan's gauge is lower, it is still above 50 and in the 64th percentile of its historic queue of values. In Europe, the EMU gauge is lower but at a very solid 56.6 reading and is down from a multi-month high. Its current level logs a very strong 94th percentile standing in its own historic queue of data over the last five and one-half years. The U.S. (ISM) reading also works lower to a near 90th percentile standing. On balance, the global manufacturing signals remain strong this month for the countries that matter most. And that is what markets are going to react to most strongly.

Your slip is showing...

On the other hand, there also is a core of countries with PMI gauges slipping. Of the 15 countries in the table, eight showed PMI declines in July. Seven had showed declines in June. There also are eight whose three-month PMI averages are lower than their respective six-month averages. But there are only three six-month averages below their respective 12-month averages. Moreover, only China, Russia, India, Indonesia, Taiwan and Vietnam have three-month averages below their 12-month averages. On balance, most places are seeing manufacturing growth over the last month better than it has been on average over the past year.

Special strength

The PMI gauges are especially strong in Europe where the EMU gauge, the German gauge and the French gauge each is above the 90th percentile queue level. Canada is also in the over 90th percentile club. The U.S. and Russia each with 89th percentile standings are knocking on the door. The Russian standing is peculiar given the importance of the oil market to Russia and the pressure that sector has been under.

Still, others are weak...

There are particularly weak queue standings logged in India which is at a five and one half year PMI low. Indonesia, whose PMI is just barely up out of the bottom quartile of this five and one half year queue and South Korea, whose sub 50 reading is just above the bottom third of its historic queue of values.

PMI view of the world

On balance, the manufacturing PMI view of the world is a pretty solid one. The PMIs recorded in the table are a global sampling of the data released on the day. There are a number of counties in Asia that have seen slowing in train and in Europe too where Spain, Italy and Ireland all logged somewhat lower readings on the month despite being surrounded by more upbeat conditions.

Eco-signals are positive but not unflawed

Economic signals are still expansive, but there are also some troubling straws in the winding. While monetary stimulus is largely credited with creating the expansion, money and credit growth in the U.S. and in EMU do not play a particularly strong hand as direct stimulants taking the data at face value. This raises the question of what is really behind the pick-up we have experienced. The global stock market is doing well, but there are also concerns about lofty stock valuations. As central banks get ready to cross the key Rubicon's from more stimulus to less stimulus and in some cases to outright higher interest rates, it is important to keep an eye on growth since we do not really know what underpins it. Fresh inflation data and consumer spending metrics in the U.S. are not supportive to the outlook for economic strength or to the Fed hitting its inflation target soon. Even vehicle sales in the U.S. are sputtering. It's a good time to keep your eye on more than just PMI gauges.

And then there is the land of geopolitics

Geopolitically, there is also a lot of heating up as Russia today is starting to invoke containment on the U.S. in its country as U.S. diplomats complain that they have been denied access to places that they sought to enter and empty in the wake of just-announced Russia's countersanctions. In Venezuela, security forces are going house to house to round up opposition leaders. Xi Jinping in China is saying that China likes peace but it will enforce its own security. It previously disavowed any culpability for what North Korea is dong by saying that is all that is going on there is inside the North Korean borders. But really, who does North Korea trade with? Which borders do its imports cross? We are seeing more North Koreans flee that country across the Thai border. Meanwhile, at home, Anthony Scaramucci has gone in and been tossed out of the revolving doors at the White House. The President has a new mega issue he may not even appreciate as he is reputed to have helped his son write an account of his meeting with Russia that is less than true. If this is true, there could be an obstruction of justice charge for the President. Interfering with an investigation is serious stuff regardless of the issue as Martha Stewart once found out and Bill Clinton too, although Bill evaded an adverse verdict. There is a good slug of positive economic news, but there is also enough of the other unsettling stuff to keep us on our heels for a while. So don't cheer the PMIs too loudly. They are only part of a multilayered and very complex unfolding story.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief