Global| Nov 02 2020

Global| Nov 02 2020Manufacturing PMIs Continue to Move Higher But the Virus Spreads

Summary

The global manufacturing sector continues to recover or move toward recovery after the initial body slam from the coronavirus and the policies engaged to corral it. And while October data continue to paint a picture of ongoing [...]

The global manufacturing sector continues to recover or move toward recovery after the initial body slam from the coronavirus and the policies engaged to corral it. And while October data continue to paint a picture of ongoing recovery in the manufacturing sector, the virus is back! It is insidiously spreading especially across Europe and in the U.S. and once again making economic trend analysis irrelevant.

The global manufacturing sector continues to recover or move toward recovery after the initial body slam from the coronavirus and the policies engaged to corral it. And while October data continue to paint a picture of ongoing recovery in the manufacturing sector, the virus is back! It is insidiously spreading especially across Europe and in the U.S. and once again making economic trend analysis irrelevant.

Outlook gets grimmer

As lockdowns cascade across Europe according to national dictates, the outlook for GDP is getting grimmer. Germany's DIW Institute forecasts that German GDP will fall by 1% in the fourth quarter after its sharp 8.2% rebound in the third quarter. DIW sees less impact on industry (and hence on manufacturing PMIs) but more of a hit on services. DIW expects an additional 400,000 worker to be put on short time as virus fighting progresses. Some estimate that France could experience a GDP decline of as much as 3% to 4%. The U.K. is in a world of hurt and uncertainty as it continues to fail to reach a post-Brexit deal with the EU adding to its uncertainty about the virus that is already a serious problem in the Britain. That helps to ramp up the uncertainty. Estimates for the potential U.K. growth setback range from a moderate -1.5% to an outsized -5.5%. France and the U.K. are adopting the most complete lockdowns in Europe. The lockdowns are being calibrated for one month, but where the virus is concerned there are no guarantees. So while the economic trends in Europe are very favorable, they may not be as extendable over the next few months as the virus has become resurgent and corralling it will take priority.

The trends

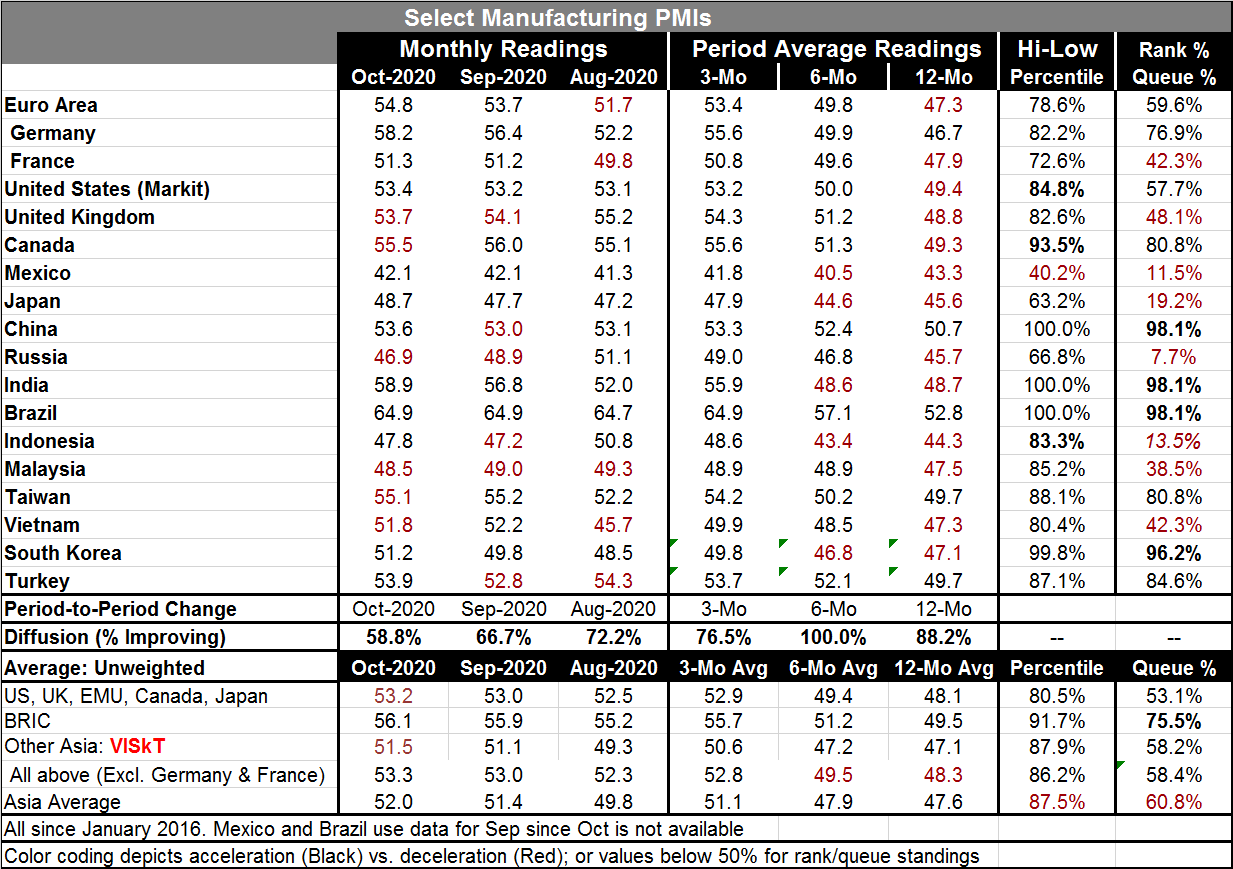

Among the 18 entries in the table, eight are below their median values calculated since January 2016. Four are in the top 10 percentile of their historic queue of values. Looking at changes in PMI values over three-, six-, and 12-months, all show diffusion readings well above 50. That means there is improvement in train on all horizons.

Month-to-month only six areas show deterioration in manufacturing in October, the same as September. Also in October, only 5 show PMI readings below 50 indicating outright sector shrinkage.

Currently the momentum looks solid. But we know it is not the way to look at things when the virus is kicking up its heels and that is the problem this month. In the U.S., the virus has resurged across many states with some intense readings in the large population centers of California, Texas and Florida as well as others. States that were hit hard in the first round are being less impacted for now; that includes both New York and Louisiana.

We continue to live in this strange world dominated by a virus that has proved to be hard to detect and to eradicate but is less lethal than originally thought but lethal enough to be scary. Nations continue to run policies intended to stop the spread. Even Sweden that has been more encouraging of people continuing to live a life of normalcy and get a natural acquired immunity from that has decided to take firmer steps to block spread this time around. But while Sweden has some new more restrictive guidelines, it also is less restrictive than other European countries.

We are once again in the grip of the virus and we will be subject to its whims until public policy takes a different approach.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief