Global| Nov 01 2019

Global| Nov 01 2019Manufacturing PMIs Continue to Demonstrate Weakness

Summary

Manufacturing PMI values that feature the ISM in the U.S. and use flash values for Europe demonstrate still weak manufacturing conditions globally. The overall average (unweighted for importance) PMI is unchanged in October at 49.3, [...]

Manufacturing PMI values that feature the ISM in the U.S. and use flash values for Europe demonstrate still weak manufacturing conditions globally. The overall average (unweighted for importance) PMI is unchanged in October at 49.3, still showing contraction. This metric shows contraction in its three-month average as well as its six-month average. The 12-month average offers a minor respite with a PMI value of 50.1, barely signaling expansion instead of contraction. Below values of ‘50’ for the raw PMI scores reflect industry declines. Above ‘50’ scores reflect expansion.

Manufacturing PMI values that feature the ISM in the U.S. and use flash values for Europe demonstrate still weak manufacturing conditions globally. The overall average (unweighted for importance) PMI is unchanged in October at 49.3, still showing contraction. This metric shows contraction in its three-month average as well as its six-month average. The 12-month average offers a minor respite with a PMI value of 50.1, barely signaling expansion instead of contraction. Below values of ‘50’ for the raw PMI scores reflect industry declines. Above ‘50’ scores reflect expansion.

Asia and China

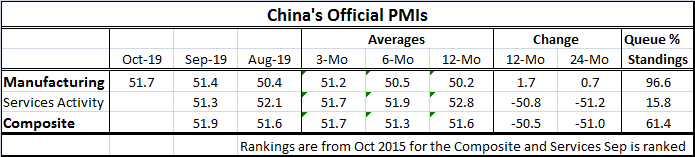

The Asia average weakened slightly in October, falling to 49.5 from 49.7. It shows contraction for three-months, six-months and 12-months which all reside below 50 and are still getting progressively weaker. One exception is that China on the month showed manufacturing improvement. The China PMI at 51.7 is an important and notable exception as it rose and remained above 50, showing expansion for the second month in a row. At this level of 51.7, the manufacturing PMI has a 96.6 percentile standing for China. That means over the ranking period (back to January 2015), it has been stronger than this less than 4% of the time. But we know that 51.7 is a relatively weak reading. So the ranking simply underscores how long China’s manufacturing sector has been exceptionally weak – and it has not all been due to the U.S. trade conflict. The table also shows the services PMI which is not updated. But there we see a contrast as through September; the service sector ranking has only a 14th percentile standing. And that is exceptionally weak. China does appear to be ready to exert any ‘locomotive’ impact on Asia.

Overall trends

Of the 15 separate readings in the table (I ignore France and Germany since they are included in ‘EMU’), ten have PMI values in October below 50, showing contraction. This compares with eight below ‘50’ in September and eleven below ‘50’ in August. Ten also are below 50 for the three-month average, nine for the six-month average and six for the 12-month average. These statistics speak of ongoing deterioration more than of broadening deterioration.

In addition, eight of fifteen countries or regions show deceleration month-to-month compared to seven in September and ten in August. Eight show a worsening of their three-month average compared to its six-month average; eleven show a worsening of their six-month average compared with their 12-month average. And all but two show a worsening of their 12-montha average compared to their average of 12-months before that. So in terms of momentum, the proportion of countries and regions when conditions are worsening is not blossoming; the number showing contraction has picked up a bit especially in October. The overall unweighted averages show slippage from 12-months to six-months then for six-months to three-months and to October conditions seem to have stabilized but at a pace signaling ongoing contraction.

The good news is that there is a sense in which momentum has stabilized even if it is to a pace suggesting manufacturing contraction. Individually China shows a more hopeful pattern while the EMU and Germany hint at ongoing worsening. The U.S. continues to decelerate but to do so moderately and now it is signaling less-pronounced patterns of jobs loss than was the case earlier.

The global economy remains weak. There are hopeful statement being made about a U.S.-China Phase-I trade deal both the U.S. officials and Chinese officials and by the various ministries. We know there are still sticking points. The bargaining process is complicated by the U.S. impeachment proceedings which may seem to weaken President Trump but which make no sign of gaining any traction in the Senate where impeachment would eventually be decided. It is not clear if the Chinese are misreading this as sign of U.S. weakness or not. If they do misread it as a sign of weakness and fail to bargain hard, it could result in a no deal and more tariffs imposed in mid-December. So far, there is no sign that things are headed in that direction.

In short, the good news is that the bad news is no worse and also that it is not worsening. In addition, stronger jobs numbers in the U.S. are encouraging and a China rebound in its manufacturing PMI is as well. But Japan did continue to slip in October. And the rankings that place each country’s or area’s October PMI is a queue of data since January 2015 shows that most countries are near their lows for this period or at least below their medians. Only three reporters have rank values above 50% which implies that they reside above their respective medians. And none of these countries have a strong reading for their manufacturing PMI in October. In fact, Malaysia, with a PMI rank standing of 67.2%, has a PMI value that shows contraction. For some countries, this episode of weakness has been protracted and that is another factor that makes it dangerous.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief