Global| Sep 01 2015

Global| Sep 01 2015Manufacturing PMI Gauges Offer Little Optimism

Summary

Economic weakening is real. Oil tried to put on a brave face earlier this week. The rumors of some unspecified Saudi deal swirled. But in the end there is no Saudi deal. And global growth is weak, undermining the ability for any deal [...]

Economic weakening is real. Oil tried to put on a brave face earlier this week. The rumors of some unspecified Saudi deal swirled. But in the end there is no Saudi deal. And global growth is weak, undermining the ability for any deal to be struck. Deal-making cannot trump the fundamentals here. Weakness is not a mirage. The PMIs tell us so. And with demand low, oil is in a glut phases and there is no deal the Saudis can make with anyone to keep output low. They are the cartel; no one else is. So ignore oil rumors. Oil IS IN EXCESS SUPPLY - chronic excess supply. And commodity prices are weak- ample evidence of weak global demand. Look at the chart of the PMIs of several of the BRICs (on the left). And Christine Lagarde has just announced that the IMF is once again looking for weaker growth ahead.

Economic weakening is real. Oil tried to put on a brave face earlier this week. The rumors of some unspecified Saudi deal swirled. But in the end there is no Saudi deal. And global growth is weak, undermining the ability for any deal to be struck. Deal-making cannot trump the fundamentals here. Weakness is not a mirage. The PMIs tell us so. And with demand low, oil is in a glut phases and there is no deal the Saudis can make with anyone to keep output low. They are the cartel; no one else is. So ignore oil rumors. Oil IS IN EXCESS SUPPLY - chronic excess supply. And commodity prices are weak- ample evidence of weak global demand. Look at the chart of the PMIs of several of the BRICs (on the left). And Christine Lagarde has just announced that the IMF is once again looking for weaker growth ahead.

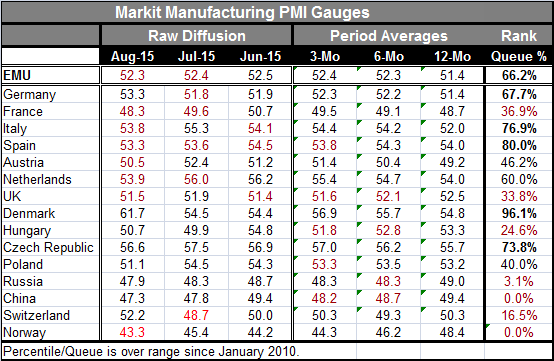

The PMI data in the table below are telling. In the far right hand column, we position the indices in their queue of data since January 2010. Note this is a period of weakness. So even a strong standing over this period is not necessarily good news; it may be just less bad news. We choose such a short period to try to evaluate more countries on a common timeline. I prefer to evaluate PMI data by their percentile standing in their historic queue of data. In other words, I don't care much about the absolute reading or the value relative to 50, the PMIs alleged neutral reading. I want to know, how often is the gauge higher or lower? The percentile standings show how often the PMI data by country have been lower. Hint, for China the answer is ZERO: zero percent of the time China's manufacturing PMI has been lower.uh oh.

Of course, there are the occasional strong responses such as Denmark's 96% standing, Spain's 80% standing and Italy's 76% standing. But let's also remember the timeline: Italy's `strong' 76% standing comes on a raw diffusion reading of only 53.8.

Note that of the 15 countries in the table, 7 of them are weaker month-to-month. Four are below 50, (breakeven). And four more are below readings of 52. In addition, the EMU reading backed off this month even as Germany's heavy weight tried to boost the PMI against a plethora of weaker readings in the rest of the community. Still, if we look at the sequential averages for three-month, six-month, and 12-month, three of the four largest EMU economies are still showing progressive gains (except Spain). But the recent monthly observations for August show values below those averaged sequential values for most members except for Germany. Is August a break in momentum?

Once again the bifurcation of the euro area is showing through. There is Germany behaving strongly and then there is everyone else in the EMU.struggling.

Of the 14 countries listed in the table, 11of them have a PMI values for August that are below their respective three-month average. For nine of them the current month's value is below their respective six-month average. We find this month's manufacturing PMI data wanting if it's reassurance about growth we are looking for.

This does not look like the sort of downtick that is the result of simple volatility and will be undone with a rebound next month. The weakness in the manufacturing PMIs comes amidst a number of poor economic developments. China today reported extreme weakness in both its manufacturing and services PMIs as its equity markets have been unraveling and as domestic indictors of growth have been withering (retail sales, car sales, industrial output, etc.). China has been a catalyst for stock market declines across the globe and here they go again today.

In a development that can't regarded as good, Japan's Economics Minister today said that it is too early to say that Japan has escaped the risk of deflation. This is 180 degrees from the pledge of the central bank to enforce 2% inflation. It is an admission of another bad development. Japan's deflation risk was something we thought policy was making progress on. Guess not.

The global slowdown is real. You can see in the table of manufacturing data. You can see it in stock market gauges. It's true that today the EMU reported a drop in unemployment to the lowest rate in 3.5 years. But unemployment data do lag; they do not lead. And the EMU unemployment rate is still high.

The EMU and all of Europe will be further grappling with problems of immigration and of an influx of people with poor identity papers. There has been more one report of how terrorists are using this as an opportunity to infiltrate Europe. As if the migration problems alone were not enough.

I short the day's PMI data are chilling. They combine with another global shattering of stock market values and the wave of wealth loss associated with it that will sweep through economies, adversely impacting consumption trends around the world.

A U.S. Aside

In this environment with U.S. inflation still very weak and with the force of inflation around the world weak and with global conditions weak, the Federal Reserve is still reported to be headed for its rate hike possibly in September- this very month. As someone with a PhD in economics, a specialty in international economics, who worked at the Fed for five years and was a dedicated Fed watcher for three more years, I can only wonder what point of view has infiltrated the Fed. Even claiming to be `still considering' a rate hike in this environment is at the very least unhelpful. Apart from the international scene, the Fed hardly has strong support for its rate hike on domestic terms since its precondition on inflation certainly is not met. The unemployment rate signal is distorted by the huge drop in the labor force participation rate. The Fed can pretend that inflation is on a path for 2% in the medium term, but as always wishing does not make it so. I hope the Fed comes to its senses before it meets in September, for everyone's sake.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief