Global| Nov 04 2013

Global| Nov 04 2013Manufacturing PMI Changes Are Negative in October

Summary

The chart of the manufacturing indices for the four largest EMU members Germany, France, Italy, and Spain shows a clear topping out over the last months. France even seems to be faltering and losing ground. This evidence bristles [...]

The chart of the manufacturing indices for the four largest EMU members Germany, France, Italy, and Spain shows a clear topping out over the last months. France even seems to be faltering and losing ground. This evidence bristles against conventional wisdom which is that EMU is in a bracing recovery. EMU manufacturing sectors do not seem to strongly embrace that notion over the past two months.

The chart of the manufacturing indices for the four largest EMU members Germany, France, Italy, and Spain shows a clear topping out over the last months. France even seems to be faltering and losing ground. This evidence bristles against conventional wisdom which is that EMU is in a bracing recovery. EMU manufacturing sectors do not seem to strongly embrace that notion over the past two months.

Of course, growth in PMI terms is not about the change in the PMI index but about its level. So when we look at the gradient of the PMI index, we are looking at momentum. EMU momentum has been lacking over the past two months, but the PMI indices are much higher than they were back in April. Momentum is not an absolute. It may be that the broader move up in the EMU PMI indices still is in gear. It is also possible that the last two months represent a morass. After all, the PMI index level is why matters and the PMIs are higher on balance, but they are not yet firmly entrenched in a region signaling growth.

The PMI levels are higher in a way that is not very reassuring. Their levels have risen from some very weak positions depicting severe declines in manufacturing output by rising to a point where the best of respondents are barley registering growth!

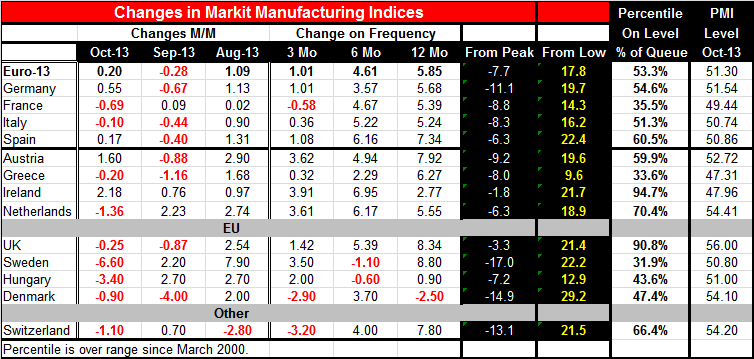

Of the EMU members the highest PMI is at 54.41 in the Netherlands, followed by 52.72 in Austria and 51.54 in Germany. The overall EMU measure itself stands at 52.3. The Netherlands measure is the strongest relative to its history, having been higher only about 30% of the time since 2002. Austria's PMI measure is higher about 40% of the time. Germany's PMI is higher about 45% of the time. The German PMI, the third strongest reading in our group of eight EMU countries, has an index that stands in just the 55th percentile of its historic queue, a very middling value. And it is supposed to the `strongman' of Europe. Good luck with that.

The non EMU members that are chronicled in the table, the UK, Sweden Hungary, and Denmark each slipped in the month, but each of them still holds manufacturing PMI values above 50. But all except the UK have weak PMI standings when evaluated against their respective historic standards.

The table shows in one of its columns the strong gains each country has had from its respective cycle low and, in another column, the much smaller increments that they stand below their respective cycle peaks. There has been clear and substantial progress made in Europe. But the questions of the future and of momentum are questions that still are up in the air and not well addressed by current trends.

Europe's banks continue to shed assets. The European Central Bank like the Federal Reserve has done a lot and, while some press for more action, the Germans remain the keepers of the Treaty; that seems to be a limiting factor for any substantial additional ECB measures.

EMU's momentum is in question. Its level of growth is weak. Its future is still clouded and it is still lacking in public institutions that can provide assistance. That is why I am slow to jump on the optimists' European bandwagon.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief