Global| Dec 01 2014

Global| Dec 01 2014Manufacturing Diffusion Weakness Reveals Global Slowdown

Summary

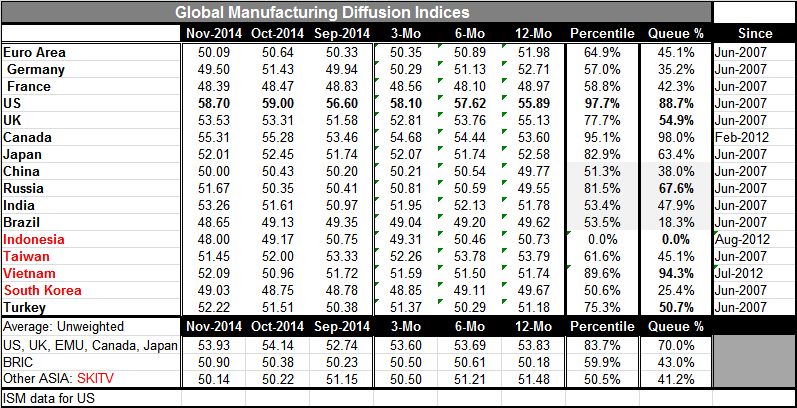

The manufacturing sector on a global basis is expanding in November with five reporting entries contracting (two of them ensconced in the euro area, which itself expanded, but slowed) while 10 showed manufacturing PMI values above 50. [...]

The manufacturing sector on a global basis is expanding in November with five reporting entries contracting (two of them ensconced in the euro area, which itself expanded, but slowed) while 10 showed manufacturing PMI values above 50. China's manufacturing PMI was dead flat at 50 in November. So 10 expanding, one neutral, and five contracting sounds like good odds? Right? Wrong!

The manufacturing sector on a global basis is expanding in November with five reporting entries contracting (two of them ensconced in the euro area, which itself expanded, but slowed) while 10 showed manufacturing PMI values above 50. China's manufacturing PMI was dead flat at 50 in November. So 10 expanding, one neutral, and five contracting sounds like good odds? Right? Wrong!

The U.S. and Russia are the only countries where manufacturing has been consistently accelerating. And while Russia's currency has collapsed, giving a reason for Russia to have increased competition in its manufacturing sector, there are important offsets there. Economic sanctions on Russia are tanking the Russian economy. It is hard to see how in this environment with so much trade cut off by sanctions, the oil sector being gutted and Russia's economy in shambles its manufacturing sector could really be improving as the survey says. We know that Vladimir Putin has been denying any impact on the Russian economy, but we also know that the central bank has been singing a different tune. Russia, just this weekend, offered to drop its sanctions on food imports if the EU would scrap sanctions on Russia. Russia seems more desperate than comfortable. On balance, the Russian survey simply does not make much sense.

That leaves us with the U.S. as the only economy with a progressively improving manufacturing sector. And that is not enough to lead the global economy ahead. Much of the U.S. strength has stemmed from its developing energy sector, a sector that will now be pressured by falling and low energy prices. In addition, the dollar has been rising and that is sure to cut down U.S. manufacturing competitiveness and to adversely affect manufacturing strength.

Evaluating the PMI levels in another way, we turn to the second to the last column in the table. There we are presented with the queue standings of the current PMI values. While the PMI indices themselves focus your attention on the value of `50' as indicating expansion (above it) or contraction (below it), the queue standings place each month's reading in a queue of its historic values, evaluating it as a queue standing in percentage terms. Notice that adjacent column to the left evaluates each current reading as a percentile standing between its historic high and low values. The queue standing is a more powerful concept since it uses all the historic values to reach its assessment, not just three: the current, highest and lowest.

The average queue standing for this group is not bad but is not solid either, at the 53.2 percentile of the average historic queue. But that is actually a distorted high reading that stems mostly from several members with very strong readings like Vietnam (94.3%) and the U.S. (88.7%). If we look at the median reading, we find it at 47.9% showing contraction. Remember that median is the statistic that has half of the readings above it and half below it. India is our median country this month. All the countries ranking below India have PMI standings below their respective 50th percentile mark, putting more than half of the reporting countries at manufacturing values that are below their respective medians. And that is weak. More than half of the countries are doing worse than they usually do more than half of the time!

We think this technique of evaluation is a more productive way for evaluating PMIs. Over time countries grow. Recessions tend to a small part of the time series for most countries (in terms of duration). Therefore, PMI values above 50 in diffusion terms are the norm, not the exception. So assessing each month as if `50' as a standard is the Holy Grail is wrong. `50' is in fact a very low hurdle and being below it or close to it is a bad thing. The U.S. has the longest manufacturing PMI time series. I have taken it back to 1985 and found that it has been below 50 only 17.5% of the time. So it is much more telling to flag of a period of slowdown and anemic growth rather than to wait until it is an outright decline to raise the warning.

Warnings are being raised by the queue standings. They are raised in more than half the countries in that table and there are few above 50% that are strong enough to stop worrying about. There are about three in that class: Vietnam, the U.S., and Russia (if you believe the Russian numbers). If you junk Russia for credibility's sake, you have only the U.S. and Vietnam with strong queue standings. It's not much to go on.

On balance, the PMIs are not definitive for several reasons. One of which is that few of these countries have very long time series to evaluate. Because of that, we have taken the period of analysis only back to June 2007 at the earliest and over that period we expect to find weak diffusion readings; therefore, low percentile standings for that period, in particular, is bad news indeed. It is worse than its own standing may seem as the underlying absolute diffusion values are also weak.

Dropping oil prices should breathe some life into the global consumer. Russia is the most affected oil-producer in this table; everyone else is a net consumer by far. So I don't think the global economy is plunging over the precipice, but I do think this is a time for governments to act to seize the opportunity of low oil prices and its attendant stimulus to try to make the shot in the arm the consumer will get from low oil prices into something that will have staying power.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief