Global| May 02 2014

Global| May 02 2014Manufacturing Continues to Recover in Europe but Slowly

Summary

The manufacturing PMI gauge for the European Monetary Union rose to 53.4 in April from 53.0 in March. The April level is barely above its February level of 53.2. The EMU manufacturing sector continues to improve, but improvement is [...]

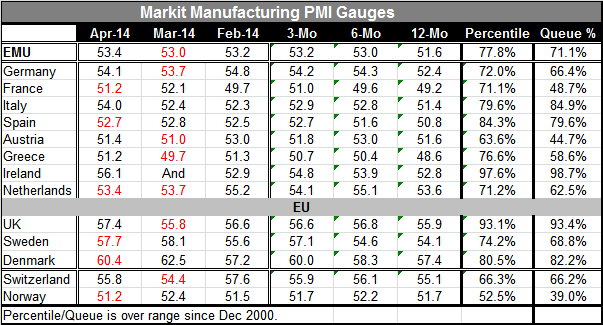

The manufacturing PMI gauge for the European Monetary Union rose to 53.4 in April from 53.0 in March. The April level is barely above its February level of 53.2. The EMU manufacturing sector continues to improve, but improvement is extremely slow. The three-month averages tell the tale. The PMI's three-month average at 53.2 is barely ahead of the 6-month average at 53.0. The 12-month average at 51.6 is well below the 6-month average. From 12 months to six months, there was a relatively rapid improvement in the manufacturing sector in Europe. However, over the last six months, improvement is coming at a slow pace. Even so, the manufacturing sector sits in the 71st percentile of its historic queue, implying that it's higher only about 29% of the time. This is not a strong reading, but it is a relatively firm reading.

The manufacturing PMI gauge for the European Monetary Union rose to 53.4 in April from 53.0 in March. The April level is barely above its February level of 53.2. The EMU manufacturing sector continues to improve, but improvement is extremely slow. The three-month averages tell the tale. The PMI's three-month average at 53.2 is barely ahead of the 6-month average at 53.0. The 12-month average at 51.6 is well below the 6-month average. From 12 months to six months, there was a relatively rapid improvement in the manufacturing sector in Europe. However, over the last six months, improvement is coming at a slow pace. Even so, the manufacturing sector sits in the 71st percentile of its historic queue, implying that it's higher only about 29% of the time. This is not a strong reading, but it is a relatively firm reading.

Among the member countries listed in the table, Ireland has the strongest PMI at 56.1, and next is Germany at 54.15 followed by Italy at 54.0. However, if we order countries according to where the PMI stands compared to its historic queue, the strongest manufacturing sector is in Ireland which stands in the 98th percentile of its historic queue followed by Italy in the 85th percentile of its historic queue and Spain in the 79th percentile. The relative ratings rank each country based upon its historic distribution rather than as an absolute score.

Austria is the weakest country in terms of its relative standing. It stands in the 63.6 percentile of its historic range and its raw score of 51.4 is only slightly ahead Greece and France at 51.2. Furthermore, Austria shows almost no momentum; its 12-month average is 51.6 compared to the three-month average at 51.8. With its current score of 51.4, there is very little in the way of positive momentum for Austria.

The non-EMU member countries in the table include the UK, Sweden, Denmark, Switzerland and Norway. Among them only Norway is weak. Norway's gauge at 51.2 is as weak as France and Greece and even weaker than its historic profile. Its current value sits in the 39th percentile of its historic queue, well below its median value which lies at the 50th percentile mark. The remaining nine EMU members would rank in the top echelons of the EMU, with raw scores ranging from 55.8 to 60.4. The UK and Denmark have extremely strong percentile standings in the 93rd and 82nd percentiles, respectively. Sweden and Switzerland, however, show moderate percentile standings considering their high raw scores. This tells us that these countries are used to having relatively strong manufacturing sectors.

The chart shows us the comparison of the UK, the EMU region and the United States. The US and the UK have had leading manufacturing sectors for some time, but the US has recently fallen off its pace. The UK reading continues to be strong while the EMU reading has been stable and is moving up slowly. While the US has had a recent setback, it's clear that manufacturing in these three key regions continues to expand. In the US case, there is a question as to how much of the recent manufacturing weakness has been due to weather. Economic data on this are unclear, but there seems to be some revival engaged in the US economy. So despite its setback, the US seems to be poised to recover its past pace. The world manufacturing sector continues to show growth. Even China that saw some setback to its manufacturing sector shows growth in April.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief