Global| Nov 30 2017

Global| Nov 30 2017Manufacturing and Services PMIs Weaken in China

Summary

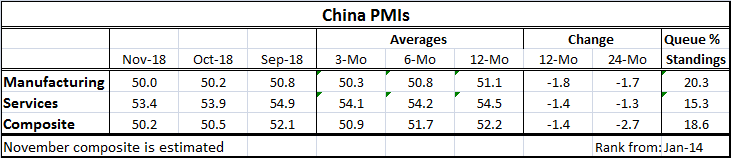

The manufacturing PMI slipped again in November, dropping for three months in a row. It extends a broader continuing a string of slippages. Manufacturing has been eroding as its six-month average is below its 12-month average and its [...]

The manufacturing PMI slipped again in November, dropping for three months in a row. It extends a broader continuing a string of slippages. Manufacturing has been eroding as its six-month average is below its 12-month average and its three-month average is below its six-month average. Service has the same broad slippages as manufacturing with only two monthly drops in a row.

The manufacturing PMI slipped again in November, dropping for three months in a row. It extends a broader continuing a string of slippages. Manufacturing has been eroding as its six-month average is below its 12-month average and its three-month average is below its six-month average. Service has the same broad slippages as manufacturing with only two monthly drops in a row.

The queue standings of the manufacturing and services indexes are positioned in their 20th and 15th percentiles, respectively. The composite index has an 18th percentile standing. These are on timelines back to January 2014.

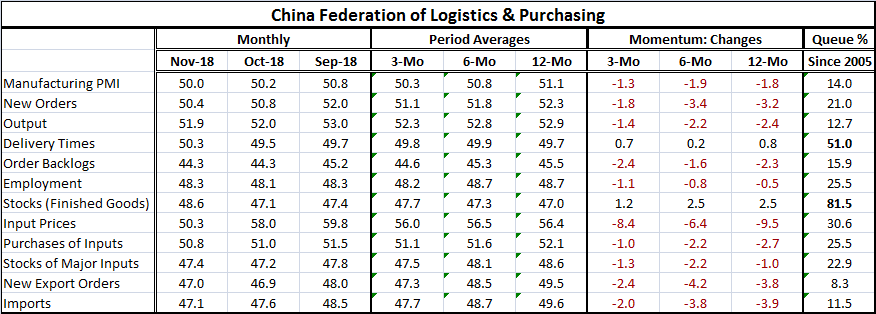

The chart looks at momentum for several measures in the manufacturing sector. It shows the ramp up of manufacturing and peaking in early-2017 followed by the ongoing wind-down that is still in progress and largely ongoing.

The manufacturing PMI for China in November dropped to 50, a dead neutral reading indicating industrial stagnation.

The manufacturing detail is provided on a much longer timeline back to 2005. On this timeline, the manufacturing queue percentile standing is at its 14th percentile. And all components standings, save two, are in their 30th percentile (bottom 30% of all readings) or weaker.

The table also carries data on momentum, changes in readings over 12 months, six months and three months. The momentum changes are sweeping across all categories on all horizons with only two exceptions. This is remarkably consistent erosion. The two exceptions are stocks where levels have been drawn down by less (diffusion readings for inventories are below 50), and oddly for supplier deliveries where delivery speeds are getting slower, not faster as should be the case when slack appears. However, delivery speeds have gone from below 50 up to a neutral reading at 50.3 from 49.5. In this case, it appears that delivery speeds that have been getting ‘faster’ have moved to a more static situation where speeds in fact are little changed. The slippage in demand might be the reason for delivery speed not picking up faster despite the appearance of more slack in the economy. There is more slack, but there is also less demand.

China is showing a great deal of weakness.

Globally, attention is shifting from economic events to geopolitical events with the G20 meeting in Argentina in progress. Since all the world leaders are gathered together at the summit, the date and the place have become a focal point for all the conflicts that are in train- and there are many of those. Russia’s latest grab of three ships in the Black Sea approach to the Gulf of Azov has set in motion a new string of events and of countermeasures. Trump cancelled his planned meeting with Putin. The killing of Jamal Khashoggi also hangs over this conference not the least because the Crown Prince from Saudi Arabia himself is attending. And in the U.S., with Democrats getting ready to assume their new position and wield their new powers in Congress, political events back home are starting to unfold. All this makes the meeting in Argentina a flash point for news of all sorts.

Today markets flew higher on an offhanded comment by Trade Representative Robert Lighthizer who said he would be surprised if Saturday’s dinner between U.S. President Donald Trump and his Chinese counterpart Xi Jinping “wasn’t a success”.

And on another front, while Mario Draghi has affirmed that European QE will end, the new comments from U.S. Fed Chair Powell and minutes from the last Fed meeting confirm that the Fed may be preparing to change pace and slow its tightening pace after December.

A lot of news is breaking. Evidence of weakness sweeps across Europe as well as in China. The U.S. shows signs of slowing but also of lingering strength. Both cyclical and structural elements of policy are in flux. The impact on uncertainty is substantial in such an environment. Markets seem to be caught in cross currents with the DJIA currently down, the NASDAQ higher, bond yields rising and oil prices falling all on the day as I write this report. It is a menagerie of effects that is hard to make sense of. Next week there is a solid offering of economic data again with the U.S. jobs report on tap. Life goes on even when the heat gets turned up.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief