Global| Oct 16 2018

Global| Oct 16 2018Macroeconomic Assessments by ZEW Experts Continue to Sink

Summary

The scene Financial experts responding in the ZEW economic survey found current conditions weaker just about across the board (the U.S. an exception) with macroeconomic expectations cut everywhere with no exceptions. At the same time, [...]

The scene

The scene

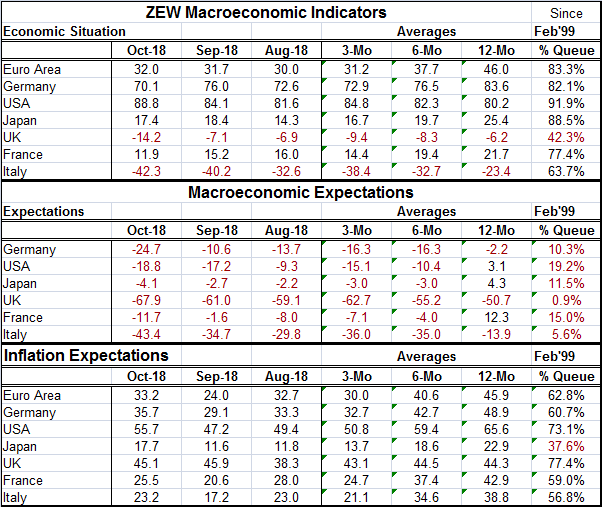

Financial experts responding in the ZEW economic survey found current conditions weaker just about across the board (the U.S. an exception) with macroeconomic expectations cut everywhere with no exceptions. At the same time, inflation expectations worsened everywhere except in the U.K. Long-term interest rate expectations rose in all regions and expectations for equity values fell across the board with Japan holding out as a minor exception. On balance, the ZEW survey participants are a pessimistic lot. Conditions are weaker, expectations are cut, inflation and interest rates will be higher and stocks will weaken as well. Are all those things really internally consistent?

This ZEW ‘scenario’ may in fact come to pass. But it has elements that I find curious especially amid the facts on the ground (true facts, not fake facts).

I do not reject ‘Keynesianism’ - nor do I think it is the only way to look at things. However, in an environment in which inflation has been stable and where economic conditions are expected to deteriorate, why is there so much pessimism about inflation? What is driving inflation even as ZEW members look for official interest rates (short-term rates rise imply official rate hikes) to rise in all survey regions except the U.K.? For the record, on the month, the ZEW crude oil price assessment slipped a bit so inflation is not being pushed by oil in the ZEW view. What is driving inflation?

Current activity is strong

Even admitting that the ZEW forecasts are as they are characterized above, there is (as always) more to the story than ‘just that’ does abrader view reconcile the forecast elements? Well, there is this: for example, the current situation or economic situation, while broadly weakening, still has an 83rd percentile standing in the EMU, an 82nd percentile standing in Germany, and a 91st percentile standing in the U.S. There is a below median 42nd percentile standing in the U.K. and softer readings in France (77th percentile) and Italy (63rd percentile). But on the whole, while the economic situation is seen worsening, the slippage is small, and when viewed year-over-year, it only worsens in the EMU, Germany, and Italy. So despite some current slippage, there is some period in which strength is prevailing.

Expectations plunge

However, macroeconomic expectations are falling month-to-month and usually falling significantly. The small drop in the ‘economic situation’ and its high percentile standing readings are in marked contrast with large monthly declines in macroeconomic expectations - severe declines are logged in expectations year-over-year and extraordinarily low percentile standings are the result with the U.S. having the best macroeconomic expectation at a standing in its lower 20th percentile followed by France in its 15th percentile and most countries and regions are around or below their respective 10th percentile - or lower. This part of the survey is really at odds with rising inflation, especially with the strongest economy (the U.S.) having a central bank that is hiking rates peremptorily.

When beliefs disconnect from the chain of causation

Again my question to the ZEW experts is: how can economic conditions be so broadly deteriorating and the future so rough and still drive inflation higher? As noted above, inflation expectations are up month-to-month everywhere except in the U.K. Year-over-year they are up in the EMU, Germany, and France (barely). The U.S., with the strongest economic situation and the highest-ranking expectations, has a fall in inflation expectations year-over-year but also has the second highest ranking for the level of inflation expectations currently (second to the U.K.). Stock markets are seen higher than 12-months ago in the U.S. and Germany but weaker month-to-month in most places and with below median queue values everywhere. The U.K. stock market assessment is at its weakest ever and Italy is close to its weakest ever stock market assessment. In the case of the U.K., Brexit expectations dominate the analysis and in the case of Italy it is its ‘new’ government and its insistence on breaking EU budget parameters.

Of course, the ZEW survey is a stew of results where every ‘chef’ prepares his or her own menu and dumps it into the same pot. So it should not be surprising that in an amalgamation such as that some curious ‘tastes’ develop. We also have some curious circumstances.

The unexpected paves the way for the long-anticipated

Economic growth has endured longer than many had expected and unemployment rates in the West have fallen to unexpectedly low levels especially in the U.S., Germany, and the U.K. While labor markets have seemed to ‘tighten up,’ wages remain restrained and so does inflation. The ZEW forecasters, certain EMU board members and U.S. officials all seem to have some sort of stopped clock forecasting method or are taking the ‘Godot’ forecasting approach. By that I mean that they all are waiting for an event that may never happen but they are unwilling to give up on it. So they are simply holding their inflation forecasts in place, all but certain that this environment MUST produce inflation. Even though they continue to see these forecasts befuddled by events, they wait.

We are stretching the credibility of the modern post-war world with this run of growth combined with with the low unemployment and with low stable inflation and ‘no one’ (apparently) is prepared to believe it will continue (but markets do; see the U.S. yield curve and note the University of Michigan inflation expectations readings). So that is the worry that underlies all the ZEW forecasts whatever ‘models’ they use to assess events. The U.K. and Italy have a few special problems in the works, but for the rest is matter of looking for ‘historic norms’ to set in and waiting...and waiting.

The weight of the wait

What no one seems willing to deal with is what Donald Trump is dealing with and that is globalization. Globalization changes things. It changes the way things work. It’s as though a new expressway has been built but central bankers want to stick to the old roads and predict traffic jams. Globalization, supported by a number of technological innovations, has broken down national borders, lifted constraints and made national statistics less relevant for policy purposes. Labor services have become more malleable and the internet has shifted where work can be done. Factories have networks and supply chains so that work can actually be shifted abroad easily. On balance, labor does not call the tune on inflation as it once did. But traditionalists are in denial about that. It is not that Keynesianism does not work; it is that the paradigm in which a bottleneck is defined has to be redefined and broadened and perhaps broadened to such an extent that it will lose its empirical meaning. But neither macroeconomics nor policy-economics have come to grips with that. So we sit and wait for... Godot.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief