Global| Oct 24 2008

Global| Oct 24 2008Lower Prices Spurred U.S. Existing Home Sales

by:Tom Moeller

|in:Economy in Brief

Summary

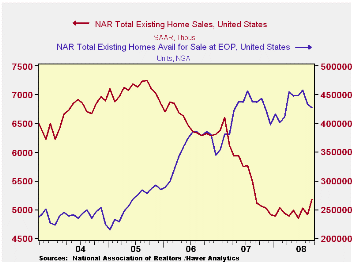

The level of September existing homes jumped 5.5% from August to 5.180 million, according to the National Association of Realtors. The rise followed an unrevised 2.2% August decline and beat Consensus expectations for a selling rate [...]

The level of September existing homes jumped 5.5% from August to 5.180 million, according to the National Association of Realtors. The rise followed an unrevised 2.2% August decline and beat Consensus expectations for a selling rate of 4.95M homes. Total sales include sales of condos and co-ops.

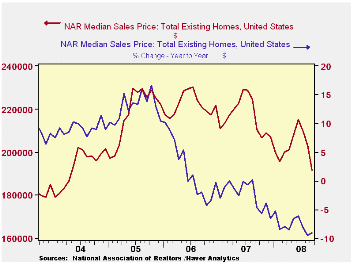

Median home prices fell 5.7% (NSA) last month for the third consecutive monthly drop. That pulled the y/y comparison to -9.0%. Prices have fallen 16.7% since their peak in April 2007.

Sales of existing single-family homes rose 6.2% after an

unrevised 1.4% August decline. The y/y gains in both total sales and

sales of single family homes turned positive for the first time since

November 2005. Sales of existing homes, nonetheless, are down by

one-third from their peak in mid-2005.

By region, home sales in the West led last month's increase with a 16.8% m/m gain. That lifted sales by more than one third versus the year ago level. Sales in the Midwest also rose but by a lesser 4.4%; the y/y change is still a negative 2.5%. In the South rose 2.2% (-7.8% y/y) but sales in the Northeast were off 1.2% (-7.7% y/y).

The number of unsold homes (condos & single-family) on the market fell 1.6% during September (-2.4% y/y) after a 5.2% August drop. At the current sales rate, the inventory fell to a 9.9 months supply versus the April peak of 11.2 months. For single-family homes, however, the inventory fell a bit more to a 9.4 months supply at the current sales rate, down from an 11.0 months supply in June.

Subprime Facts: What (We Think) We Know about the Subprime Crisis and What We Don’t from the Federal Reserve Bank of Boston is available here.

| Existing Home Sales (Thous) | September | y/y % | August | September '07 | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|

| Total | 5,180 | 1.4 | 4,910 | 5,020 | 5,672 | 6,508 | 7,076 |

| Northeast | 840 | -7.7 | 850 | 910 | 1,008 | 1,090 | 1,168 |

| Midwest | 1,190 | -2.5 | 1,140 | 1,220 | 1,331 | 1,491 | 1,589 |

| South | 1,900 | -7.8 | 1,860 | 2,060 | 2,240 | 2,576 | 2,704 |

| West | 1,250 | 34.4 | 1,070 | 930 | 1,093 | 1,353 | 1,617 |

| Single-Family | 4,620 | 3.8 | 4,350 | 4,450 | 4,958 | 5,703 | 6,181 |

| Median Price, Total, $ | 191,600 | -9.0 | 203,100 | 210,500 | 216,617 | 222,000 | 218,217 |

by Robert Brusca October 24, 2008

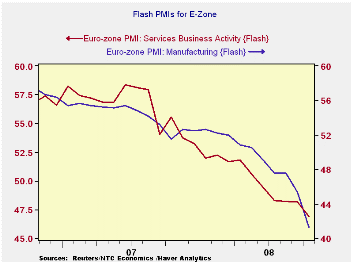

Europe’s PMIs are now weak. They are at or near the lows we

have seen since the services PMI was issued in July of 1998. Both

service sand MFG PMIs are below their respective neutral readings of 50

and are thus indicating CONTRACTION.

The MFG PMI is even at its lowest level since June of 1997

when its survey began.

The month to month drop in the MFG index is the largest over

this period while the services drop ranks as about the 18th smallest

‘gain’ in its history of the 63 drops in the 123 observation of the

series. This months’ drop also ranks 45 in size among all drops or as

the eighteenth largest drop when ranked among drops (or the bottom 28

percentile). In relative magnitude this month’s service sector drop is

a bottom third affair. The MFG sector is taking the relatively larger

hit for this month. It is taking its largest drop on record and falling

to its lowest position in its history.

Europe has been a late comer to weakness but is catching up

with the US. In September the US MFG PMI stood at a level 43.5, below

where Europe was then but above where Europe is now. The US ISM may yet

fall to a lower level in October and be weaker than Europe. But the two

indices are clearly now sharing the same dimension of weakness

regardless of which is the weaker. Last month the US non-MFG PMI stood

at a level of 50 above the service sector reading for EMU. EMU’s drop

to 46.91 seems clearly a weaker reading than what we get out of the US

Non-MFG PMI (where 44.6 is the weakest reading ever) since sharp

declines have not marked its recent trend. But things are changing fast

and maybe the US non-MFG sector will weaken beyond Europe’s reading. We

do not yet know how rapidly the economy descended in October. But this

is not a time that has rewarded optimistic projecting. Maybe the

message from Europe is that we should brace ourselves for even worse

news from the US.

One message from Europe is nonetheless clear. Both MFG and

Services indices are quite weak and the MFG sector is falling very hard

right now. Expect the more conventional readings for Europe to start to

look a lot weaker. Since this report is topical and up-to-date as of

October it is a month or two ahead of the release of more conventional

economic reports form Europe.

| FLASH Readings | ||

|---|---|---|

| Market PMIs for the E-Zone-13 | ||

| MFG | Services | |

| Oct-08 | 41.33 | 46.91 |

| Sep-08 | 44.97 | 48.44 |

| Aug-08 | 47.55 | 48.46 |

| Jul-08 | 47.38 | 48.32 |

| Averages | ||

| 3-Mo | 46.63 | 47.76 |

| 6-Mo | 48.40 | 48.60 |

| 12-Mo | 50.37 | 50.52 |

| 33-Mo Range | ||

| High | 57.61 | 60.65 |

| Low | 41.33 | 46.68 |

| % Range | 0.0% | 1.6% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief