Global| Aug 01 2016

Global| Aug 01 2016Key Global MFG PMIs Mostly Weaken

Summary

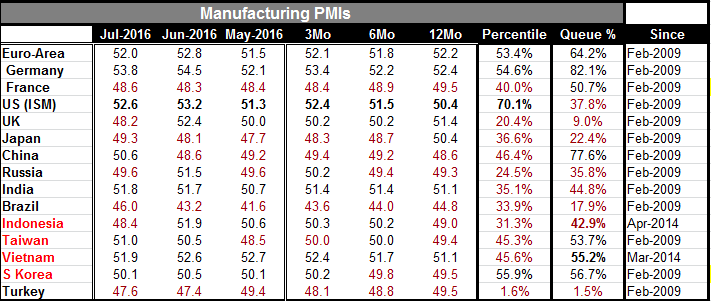

Global manufacturing gauges stuck close to the 50 breakeven mark or fell below it in July. Seven reporters in this group of 15 have values below 50. The highest MFG PMI value is from Germany at 53.8 and for the period from February of [...]

Global manufacturing gauges stuck close to the 50 breakeven mark or fell below it in July. Seven reporters in this group of 15 have values below 50. The highest MFG PMI value is from Germany at 53.8 and for the period from February of 2009 that reading is in the top 18% of all the readings on that period for Germany, which should underscore how weak the recovery process is rather than flag this as a 'strong' reading in July.

Global manufacturing gauges stuck close to the 50 breakeven mark or fell below it in July. Seven reporters in this group of 15 have values below 50. The highest MFG PMI value is from Germany at 53.8 and for the period from February of 2009 that reading is in the top 18% of all the readings on that period for Germany, which should underscore how weak the recovery process is rather than flag this as a 'strong' reading in July.

Apart from Germany no reporter in this table has a queue standing for the period of its final MFG gauge that is any higher than South Korea's 56.7% except for China's 'official gauge' which is at a diffusion reading of 50.6, barely above breakeven, yet has a 77th percentile standing, underscoring how weak conditions have been in China. The private sector Caixin survey for China is still below the diffusion value of 50 in July.

In the US, the door barely open to a rate hike, seems shut

Global manufacturing conditions remain weak. Oil prices find West Texas Intermediate slipping toward $40/barrel after a period of struggling higher. Demand is simply not coming on stream. The U.S. reported out a weak 1.2% Q2 GDP reading and that has been the catalyst for markets to improve today. It is now more widely believed that the Fed will once again not be able to keep the door open for a rate hike. The job reports that the Fed has relied on in the past are still pending. But now three GDP numbers in a row with growth rates near 1% would seem to put and to keep the Fed on the sidelines. But, of course, those conclusions are ephemeral... GDP gets revised and employment numbers if robust enough can continue to cast doubts on GDP. For now the markets have their scenario firmly in hand.

What we know is that manufacturing globally remains weak. Not only are PMI gauges near 50 but many are below 50 and most are weak even by the standards of this weak recovery.

Momentum is missing

As for momentum it is mostly missing. The current month is below the 3-month average in 7 of these 15 countries/regions. The 3-month average is below the 6-month average in five of them. The 6-month average is below the 12-month average in 7. This underscores the broad-based state of weakness: the PMI readings are low, their queue standings are moderate to weak and their momentum is poor-to-mixed at best.

Steps on a treadmill

Central banks continue to take steps toward stimulus, except in the U.S. where the central bank seems to want to take steps to remove stimulus, but just can't get conditions right enough to do it. Japan's latest policy foray was not embraced by markets. The ECB has been essentially stuck for some time with money and credit flows showing no signs of responding to past ECB actions. Recent U.K. data, of course, show a weakening in train in the wake of the Brexit decision, and the BOE is widely expected to take some counter steps to prop up flagging sentiment.

The dog that still won't bark

There is no underlying source of stimulus except for some fiscal measures in China and some pending in Japan. Still, that is all small potatoes compared to the need. The problem remains excess global supply and an adverse systemic global trading system that makes progress like trying to walk up a hill against a strong wind every day. Asian economics are still the lowest cost producers, they pay low wages and their employees have a high savings rate despite their pay. That makes the Asian multiplier weak. There is no demand in the West to fulfill the excess Asian capacity. Conditions in the West remain weak as fiscal policy stays largely taboo and Asia does not reflate. There is a steady but slow drum beat of population growth globally (but not in Japan) but that is barebones underpinning. The boost to growth to take up the usual slack in recovery was smaller and shorter lived this time around, plus there was a severe structural change that ensued lowering growth rates across the most developed and industrialized nations. This displaced a good deal of labor in the West and left Asia with unexpectedly weak export markets. The usual higher than trend recovery period of growth simply did not develop or endure leaving economies to slump back into their morass of excess supply. Solutions remain elusive; slow growth remains protracted. Finger pointing, economic and social unrest, and backtracking on trade progress are ongoing issues as a result. Brexit was a result as well. The global risks remain heightened regardless of what the Fed decided at its last meeting.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief