Global| May 08 2007

Global| May 08 2007JOLTS Data Show Some Softening in Labor Market Conditions

Summary

JOLTS data for the Quit rate, a very good directions signal for the job market, show that quit rates have been drifting lower. A lower quit rate is a sign of less confidence in a workers ability (or perceived ability) to get a job. [...]

JOLTS data for the Quit rate, a very good directions signal for the job market, show that quit rates have been drifting lower. A lower quit rate is a sign of less confidence in a worker’s ability (or perceived ability) to get a job. The table below shows that quit rates in the West and the Midwest are still pretty high in their respective ranges. In the South they are still in the top 30% showing a lingering confidence that people can quit their jobs and find a new one. But in the Northeast quit rates are scraping the bottom, in the lower 16 percentile of their range and are well below average.

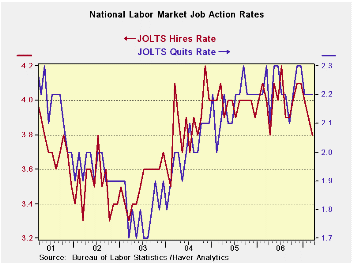

Nationally the quit rate is a bit lower but not very far off peak. Mostly it is steady at what has been a persisting high level for the quit rate since early 2006. But the hire rate has fallen more noticeably (See chart above). And while we know that the economy has matured and labor force growth has slowed the drop in the hire rate seems to be more than what demographics might thrust upon us. It is a disturbing sign.

Next we look at JOLTS data arrayed by industry. These data do not exist in the data base but have been constructed using weights to create a services sector. The other sectors are based on primary JOLTS data and sector definitions. I always like to create a services sector since goods and services sectors have such different forces putting pressure on them. Of course, construction is also quite different, these days. We don’t want the manufacturing/nonmanufacturing breakdown to bury that, as the ISM currently is doing. And government is, well, government. It is the alpha–omega sector. It’s where you go to get your first job when you are inexperienced and where you go to take a prestige job when you’ve ‘retired’ (Paulson).

These sectors show that Manufacturing and Services still sport firm levels of openings in terms of their percentile readings. Openings are in the top 25% of their respective ranges or better. Yet services and manufacturing have seen slippages recently (see raw readings in the bottom of the table). Quits are still quite strong and the quit rates have not showed much erosion for Manufacturing or Services. Hires are no longer strong in any sector. Oddly, it shows some improvement in Construction. Hires are still best (in the 57th percentile) for services and near the one-third mark or so in other sectors – clearly sub-par outside of services.

Seeing hires gain for construction is odd especially with the weakest quit rate it has seen since 2000. The government sector has a lot of openings VS moderate percentiles for hires and quits.

These data speak of slippage in the labor market. Despite the fact that the two key sectors, Manufacturing and Services, are still emitting firm readings in absolute terms, they are nonetheless slipping. Combined with other reports, such as the NFIB survey, these readings underscore that weakness seems to be spreading. What it does not tell us is if the odd early Easter and disruptive weather is responsible for it or not. But things -‘things’- are undeniably looking weaker.

One very interesting things about JOLTS is that we can get a geographical cut at the data and an industry cut as well. It is a very useful report for that reason. It shows US that the Northeast is sagging the most but hires are still weakening across the board with the exception of the West. As such, this report confirms themes we have seen in other reports.

It confirms that:

That services sector is the strongest sector.

That the services sector is showing some weakening

That things are weaker out East and stronger in the West.

While we still struggle for better quantitative assessments and to understand the causes, these general observations hold true.

| Since Sep-02 | Northeast | South | Midwest | West | |

| Quit | Quit | Quit | Quit | average | |

| Mar-07 | 1.3 | 2.3 | 1.9 | 2.1 | 1.9 |

| Feb-07 | 1.3 | 2.3 | 1.9 | 2.0 | 1.9 |

| Jan-07 | 1.4 | 2.2 | 1.9 | 2.0 | 1.9 |

| Max | 1.8 | 2.5 | 2.0 | 2.2 | 2.0 |

| Average | 1.4 | 2.1 | 1.7 | 1.9 | 1.8 |

| Min | 1.2 | 1.8 | 1.4 | 1.4 | 1.5 |

| Range | 0.6 | 0.7 | 0.6 | 0.8 | 0.6 |

| %-Tile | 16.7% | 71.4% | 83.3% | 87.5% | 77.3% |

| % AVG | 93.1% | 109.4% | 112.8% | 111.8% | 107.3% |

| Min date | Feb-04* | Sep-03* | Dec-03* | Dec-03* | -- |

| *Last Occurrence | |||||

| Major Job Sectors | ||||

| Mar-07 | Services | MFG | Constructions | Government |

| Job Openings | 79.6% | 76.9% | 47.6% | 87.5% |

| Hires | 57.3% | 33.3% | 30.0% | 40.0% |

| Separations | 64.2% | 66.7% | 8.0% | 25.0% |

| Quits | 82.3% | 100.0% | 0.0% | 50.0% |

| Raw readings by Industry | ||||

| OPENINGS | Services | MFG | Constructions | Government |

| Mar-07 | 2.3 | 2.2 | 1.8 | 2.1 |

| Feb-07 | 2.6 | 2.3 | 2.9 | 2.1 |

| Jan-07 | 2.6 | 2.3 | 1.8 | 2.1 |

| Dec-06 | 2.7 | 2.5 | 1.4 | 2.1 |

| HIRES | Services | MFG | Constructions | Government |

| Mar-07 | 4.3 | 2.3 | 4.8 | 1.5 |

| Feb-07 | 4.5 | 2.6 | 3.9 | 1.7 |

| Jan-07 | 4.5 | 2.6 | 3.9 | 1.7 |

| Dec-06 | 4.5 | 2.7 | 4.4 | 1.7 |

| SEPARATIONS | Services | MFG | Constructions | Government |

| Mar-07 | 4.1 | 2.8 | 4.3 | 1.2 |

| Feb-07 | 4.0 | 3.0 | 4.2 | 1.3 |

| Jan-07 | 4.0 | 2.8 | 5.2 | 1.4 |

| Dec-06 | 4.1 | 2.6 | 5.0 | 1.3 |

| QUITS | Services | MFG | Constructions | Government |

| Mar-07 | 2.5 | 1.6 | 1.5 | 0.6 |

| Feb-07 | 2.6 | 1.5 | 1.6 | 0.6 |

| Jan-07 | 2.5 | 1.6 | 1.8 | 0.7 |

| Since 2000 | ||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief