Global| Jun 12 2019

Global| Jun 12 2019Japan’s Orders Surge in April

Summary

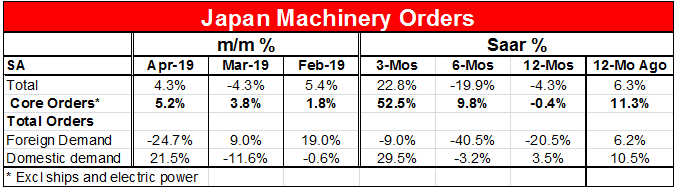

Japan's orders surged in April. Both overall and core orders rose briskly in April with each gaining more than 4% month-to-month. The paths taken by total and core orders are quite different, however, Total orders decline over [...]

Japan's orders surged in April. Both overall and core orders rose briskly in April with each gaining more than 4% month-to-month. The paths taken by total and core orders are quite different, however, Total orders decline over 12-months and fall even faster over 6-months, but log a strong 22.8% annual rate gain over three-months on strong gains in two of the past three months.

Core orders show accumulating strength. Core orders are barely lower falling by 0.4% over 12-months then they rise at a strong 9.8% pace over six months and at a whopping 52.5% annualized rate over three-months. Core orders have been rising by solid-to-strong amounts in each of the past three-months.

The core orders report is designed to be more stable by omitting the kinds of very large projects that are not consistent, that come and go, and can wreak havoc with the calculation of growth rates for orders. However, over three months both versions of the order series are looking hot.

Clearly orders are driven by domestic demand where they are up by 3.5% over 12-months, lower at a 3.2% annual rate over six-months, then rising at a strong annualized rate of 29.5% over three-months. Domestic orders are up extremely strongly in April driving the 3-month results against declines in each of the two previous months.

Foreign demand has been persistently weak. Foreign orders are down by 20.5% over 12-months they are down at a steep 40.5% annualized plunge over six-months and then are falling at a more moderate but sill fast annualized pace of 9.0% over three-months. Foreign demand is off very sharply in April falling by 24.7% month-to-month after solid-to-strong increases in each of the previous two months.

Japan’s PMI data tell an expanded story about the economy. The PMI story shows a moderate but expanding service sector against a manufacturing sector that has been weakening since late 2018 and that has been is a state of contraction since February of this year. Against that background the orders report is surprisingly strong. Clearly foreign weakness is depressing orders and holding back the manufacturing sector. And there must be negative knock-on effects for services as well. Fortunately there has been strength in domestic orders despite still moderate (below target) inflation and ongoing demographic headwinds.

On balance the orders report is encouraging. But orders are too volatile to be reassuring. The global environment remains difficult with Japan’s two largest trade partners locked in a trade war. The strong-seeming domestic environment for now is a backstop but with a consumption tax still scheduled for this year how long can that underpinning last?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief