Global| Jul 05 2007

Global| Jul 05 2007Japan’s LEI Rose in May: Signal Still Uncertain

Summary

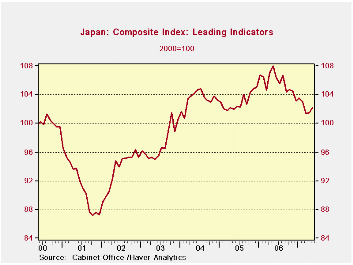

Japans May rise in its LEI is the second in a two months technically, but is still not very impressive. Most growth rates still show it declining (see chart and table). However, over two years the index does post an annualized rate [...]

Japan’s May rise in its LEI is the second in a two months technically, but is still not very impressive. Most growth rates still show it declining (see chart and table). However, over two years the index does post an annualized rate of growth of +0.2%. Japan’s economy has been vexing in this cycle.

After a period of weakness Japan posted a rise in its LEI and of course in the underlying conditions that this index represents. The LEI’s growth rate from October 2001 to July of 2004 was at an annual rate of 7.1%, pretty impressive. But then it peaked dipped and expanded again. The next result was that from the peak to next peak from roughly July 2004 – May 2006 the growth of the index dropped off to a pace of 2.6%. Then really bad things began to happen as from that second peak in May 2006 the index fell to a low in March 2007 at 101.4 During that period the LEI was dropping at very fast 8.3% pace. Still the period of decline was less than a year. From the bottom of the LEI’s trough back in October of 2001 the LEI is still growing but at a much more modest pace of 2.9%.

While the two-month rebound in the LEI is not definitive or a reliable guide of the future it did arrest this extended period of decline the LEI.

During this period Japan has continued to be dogged by deflation and its growth statistics have continued to be irregular, as the LEI attests. But the BOJ has been making noise as though it nonetheless wanted to hike interest rates. While the LEI does not tell a comprehensive story on the economy it does tell a capsulated story and one that should be viewed as cautionary with respect to growth conditions in Japan.

Japan at one time turned the corner fast but then it slowed and has since backtracked. Weakness in the yen attests to the mixed situation there and how investors view it. While we do not like to see governments telling central banks the kind of policies they want it is understandable in this environment that Japan’s governing party is wary of the BoJ’s apparent intent to go back to a rate hiking cycle so soon.

The BOJ and the Japanese government are ever mindful of the demographics and fiscal difficulties that lie ahead for them. If anything these concerns have kept them too eager to restrict fiscal policy (by hiking taxes) and too quick to raise interest rates (or too slow to cut them). Japan remains a country with the opposite policy tendencies to most Western nations even if it faces many of the same problems.

| Levels | Growth (saar) | ||||||

| May-07 | Apr-07 | Mar-07 | 3M0 | 6M0 | 12Mo | 24MO | |

| LEI | 102.2 | 101.5 | 101.4 | -2.7% | -4.4% | -5.4% | 0.2% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief