Global| Mar 11 2010

Global| Mar 11 2010Japan’s GDP Still Up Sharply But Less Than Before Revision

Summary

The back off in Japan’s core machinery orders this week began to deflate expectations for a capital formation jolt to spur growth. Still, gross capital formation did fall much more slowly in Q4 compared to Q3 as plant and equipment [...]

The back off in Japan’s core machinery orders this week began to deflate expectations for a capital formation jolt to spur growth. Still, gross capital formation did fall much more slowly in Q4 compared to Q3 as plant and equipment spending swung to post positive results for the quarter. Residential construction continued to fall but the drop is only at about half the pace of the decline of earlier quarters. Domestic demand is up by a mere 2.1% annualized in Q4. Public spending rose at a 2.5% annual rate. But exports are flying, leading growth with a 21% growth rate. That is slower than previous quarters but still, obviously, a very strong rate of growth. Imports, once up a 23% pace in Q3 edged higher at just a 5.1% annual rate in Q4.

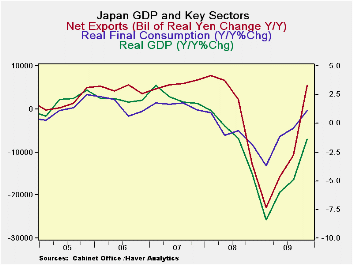

Yr-over-year trends show a more pronounced export slowing and more stability in imports. Domestic demand is shrinking year-over-year. Japan’s growth posted a drop of only 1.4% Yr/Yr in Q4 compared to a Yr/Yr drop of 4.9% in Q3.

On balance the Japanese economy is doing better but its improvement is mostly in the hands of the export sector. Fortunately for Japan its two largest export markets, China and the US, are posting improved growth; China’s growth has been very strong. Japan’s strength still derives mostly from its export sector. The domestic economy is marking some growth but with no vigor. Since the main impetus to growth is exports there is some hope that that will translate into expansion and to more capital spending in export and export-related industries. This would help to boost Japan’s output internally even though the real cause of the investment would be external demand. The drop off in core machinery orders this past week began to dash hope that such an effect was gathering steam in the pipeline. Japan’s recovery is still very dependent on what goes on outside its borders. The domestic support for its expansion is minimal. More disturbing is the conclusion that there is little evidence that its export strength is rekindling domestic sources of growth.

| Japan's GDP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Consumption | Capital Formation | Trade | Domestic Demand |

|||||||

| GDP | Private | Public | Gross Fix Cap |

Plnt& Equip |

Housing | X-M: lbns E |

Exports | Imports | ||

| Change Q/Q at annual rates of change; X-M is Q/Q change in Blns of real yen | ||||||||||

| Q4-09 | 3.8% | 2.8% | 2.5% | -0.4% | 3.8% | -12.5% | 2.9 | 21.7% | 5.1% | 1.5% |

| Q3-09 | -0.6% | 2.4% | 0.3% | -11.7% | -9.8% | -27.7% | 2.8 | 37.8% | 23.3% | -1.9% |

| Q2-09 | 6.0% | 4.6% | 1.1% | -11.0% | -15.6% | -32.6% | 7.5 | 42.2% | -14.7% | -1.1% |

| Q1-09 | -13.7% | -5.2% | 3.2% | -22.6% | -30.6% | -23.7% | -7.7 | -66.3% | -53.9% | -11.3% |

| Change Yr/Yr; X-M is Yr/Yr change in Gap in Blns of real yen | ||||||||||

| Q4-09 | -1.4% | 1.1% | 1.8% | -11.8% | -13.9% | -24.5% | 5.5 | -5.3% | -15.5% | -3.3% |

| Q3-09 | -4.9% | -0.4% | 2.3% | -15.8% | -20.9% | -20.0% | -10.7 | -22.9% | -16.5% | -3.7% |

| Q2-09 | -6.0% | -1.1% | 2.0% | -15.0% | -22.0% | -9.8% | -15.8 | -29.4% | -18.7% | -3.9% |

| Q1-09 | -8.4% | -3.7% | 0.5% | -13.9% | -19.6% | -0.3% | -22.9 | -36.3% | -17.7% | -4.9% |

| 5-Yrs | 0.1% | 0.8% | 1.1% | -3.6% | -2.3% | -8.5% | na | 1.1% | -1.4% | -0.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief