Global| Oct 22 2014

Global| Oct 22 2014Japanese Trade Trends Still Feature Deficits

Summary

Japan's trade position remained in substantial deficit in September, as exports and imports both showed some life in September. Goods-exports increased by 3.1% and were surpassed by the 5% growth rate for goods-imports. Over three [...]

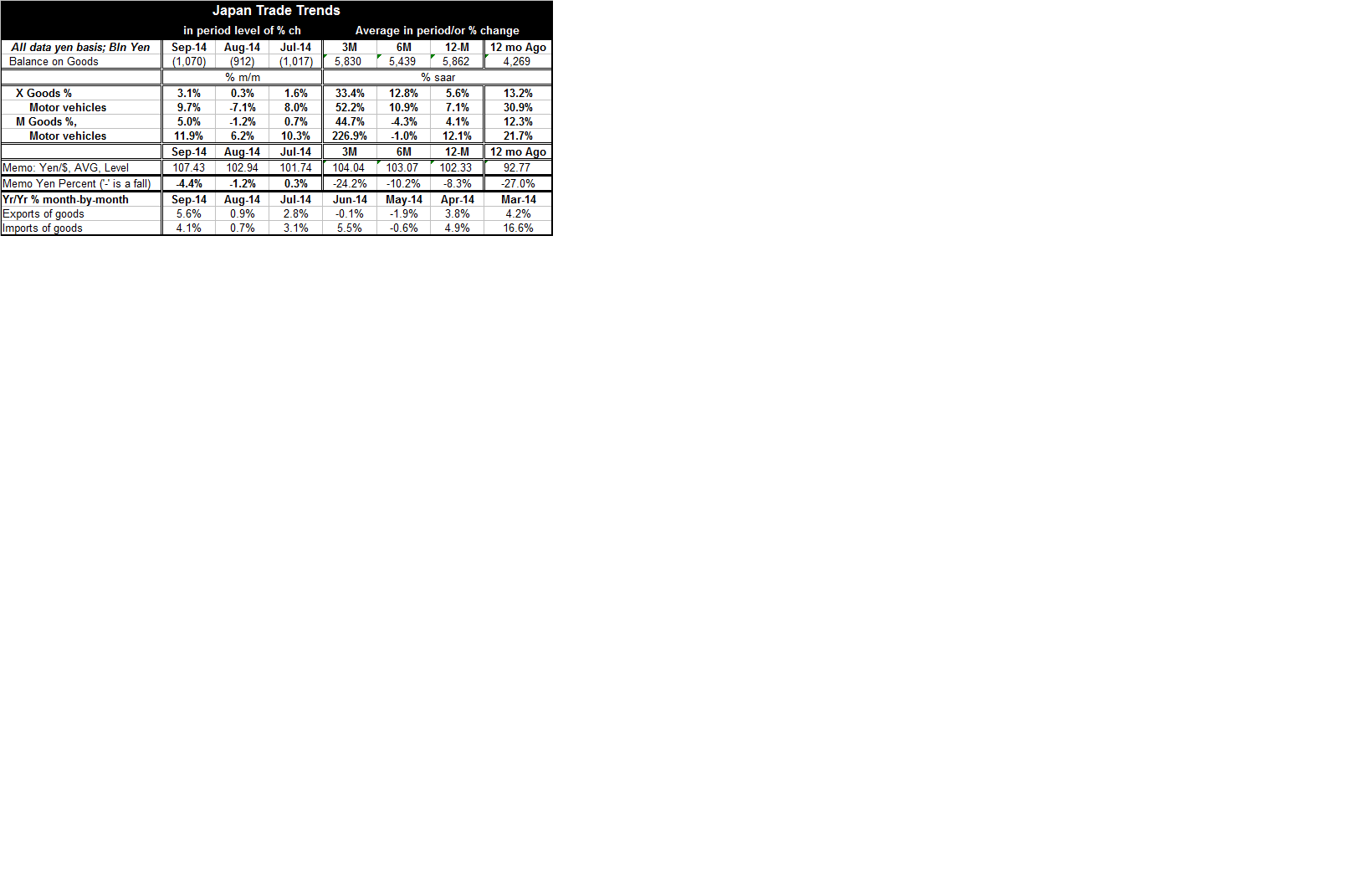

Japan's trade position remained in substantial deficit in September, as exports and imports both showed some life in September. Goods-exports increased by 3.1% and were surpassed by the 5% growth rate for goods-imports. Over three months both exports and imports have highly elevated growth rates. Exports are up at a 33.4% annual rate with imports up at a 44.7% annual rate. Over six months the growth rate settles down with exports up at a 12.8% pace and imports falling at a 4.3% pace. Over 12 months. Exports rise by 5.6% while imports rise by 4.1%.

Japan's trade position remained in substantial deficit in September, as exports and imports both showed some life in September. Goods-exports increased by 3.1% and were surpassed by the 5% growth rate for goods-imports. Over three months both exports and imports have highly elevated growth rates. Exports are up at a 33.4% annual rate with imports up at a 44.7% annual rate. Over six months the growth rate settles down with exports up at a 12.8% pace and imports falling at a 4.3% pace. Over 12 months. Exports rise by 5.6% while imports rise by 4.1%.

Over three months imports are stronger, but over the longer trends, six months and 12 months, exports are relatively stronger.

Over this entire period, the yen has been falling and Japan has been gaining competitiveness. Over three months, the yen is down at a 24% annual rate, over six months it's down at a 10.2% annual rate and over 12 months, it's down at an 8.3% annual rate. The yen's decline has been picking up speed. A weaker yen increases Japan's competitiveness and should push exports to stronger growth. The weaker yen reduces the wealth of Japan, compared other countries and increases the relative price of imports; those effects will cause imports to slow.

For the time being, there is only mild evidence that exports are beginning to benefit from their improved competitiveness and at the same time, there's scant or contradictory- evidence that imports are slowing down.

Japan now has a long string of the trade deficits that extends back to the year 2011. Japan's lost decade then its hammering by the Tsunami that created a nuclear crisis and led to a shuttering of most of Japans nuclear capability have ravaged Japan's economy. Japan's economy continues to struggle and now political problems for the administration have emerged as two ministers have just quit their posts. This could impede economic decision-making. The BOJ is still resolute in its course, and the weakening yen may be the most effective macroeconomic tool that Japan has. However, since Japanese firms have already outsourced so much activity many are now complaining that the too-weak yen is hurting them. However, Japan wants polices that stimulated its domestic economy not policies that create profits for its multinational corporations- especially not at the cost of growth at home.

Japan continues to reel from the costs of its past successes as well as from its ticking demographic time bomb. Japan's past successes caused the yen to become overly strong and that in turn hollowed-out Japan's manufacturing as its multinationals moved operations to other Asian countries and established a production foothold in the U.S.A. At the same time the cost of living in Japan became so high that many Japanese families decided to stay small and many Japanese couples decided not to have families at all to preserve their living standard. Remember... at one point Japanese real estate was so expensive Japan innovated the multigenerational home mortgage,

Japan is not going to conquer its current economic problems using traditional macroeconomic policies. It needs to solve the problem of its ticking demographic time bomb. Japanese couples need to decide to have families again. Japan, as trends stand, is going to be too be overwhelmed by its aging. That is going to be such an enormous burden that the economy will not be able to cope with it. Japan's problems are greater than anything that can be solved by a program of quantitative easing, however large the Bank of Japan's program may be.

Japan as a society has to decide what it wants to be when it grows up and by this I mean what it wants to be as it ages. Japan is facing an aging and a ratio of the old to the young ratio that dwarfs the problems being faced by China which themselves are enormous. Something must be done because the problem will not solve itself. Conditions in Japan only going to get worse unless its demographic trends are altered by a specific, targeted response.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief