Global| Dec 22 2005

Global| Dec 22 2005Japanese Trade Surplus Widens Modestly in November

Summary

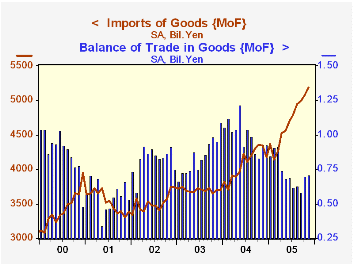

The Japanese trade balance has started to improve, with favorable movements in both exports and imports since the surplus reached a low point in September. In November, the surplus was ¥708.1 billion (seasonally adjusted), almost the [...]

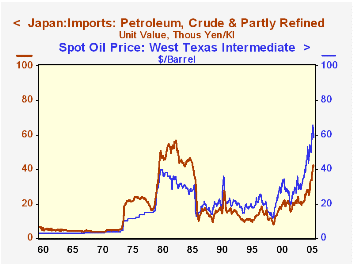

Two months ago, when we last wrote about Japan's trade, we expressed some concern over import growth and the sensitivity to oil prices which it indicated for the health of the Japanese economy generally. This time, we've looked at these import data from a longer perspective, and we find some very interesting facts. In 1980, when petroleum prices were at then historic peaks just under $40/barrel, the value of petroleum imports into Japan was ¥1 trillion monthly. The quantity of petroleum imports averaged 21.2 million kiloliters monthly, making the unit value of petroleum imports ¥47,200 per kiloliter in 1980. Now, the dollar price of oil is far higher, averaging more than $56/barrel for the first 11 months of this year. But the unit value of oil imports into Japan has been only ¥34,800! The peak month was October, with ¥42,700 per kiloliter, still less than the 1980 average. Thus, the stronger yen and weaker dollar have made a tremendous difference for Japan in the burden of this surge in petroleum prices. Granted, the Japanese economy in general is not nearly so robust as it was in 1980 and the recent unit values are much higher than the ¥10,600 of ten years ago. But the impact is clearly more muted. Further, Japan, as elsewhere in the world, has become less dependent on petroleum usage. In fact, based on fixed-weight GDP in 1995 prices, a kiloliter of imported petroleum in 2004 supported ¥6.9 million of GDP (in Q2), 88% more than the 1980 average of ¥3.7 million.

Two months ago, when we last wrote about Japan's trade, we expressed some concern over import growth and the sensitivity to oil prices which it indicated for the health of the Japanese economy generally. This time, we've looked at these import data from a longer perspective, and we find some very interesting facts. In 1980, when petroleum prices were at then historic peaks just under $40/barrel, the value of petroleum imports into Japan was ¥1 trillion monthly. The quantity of petroleum imports averaged 21.2 million kiloliters monthly, making the unit value of petroleum imports ¥47,200 per kiloliter in 1980. Now, the dollar price of oil is far higher, averaging more than $56/barrel for the first 11 months of this year. But the unit value of oil imports into Japan has been only ¥34,800! The peak month was October, with ¥42,700 per kiloliter, still less than the 1980 average. Thus, the stronger yen and weaker dollar have made a tremendous difference for Japan in the burden of this surge in petroleum prices. Granted, the Japanese economy in general is not nearly so robust as it was in 1980 and the recent unit values are much higher than the ¥10,600 of ten years ago. But the impact is clearly more muted. Further, Japan, as elsewhere in the world, has become less dependent on petroleum usage. In fact, based on fixed-weight GDP in 1995 prices, a kiloliter of imported petroleum in 2004 supported ¥6.9 million of GDP (in Q2), 88% more than the 1980 average of ¥3.7 million.

A technical note on these comments. In the third graph, we compare the unit value of Japanese petroleum imports to the price of West Texas Intermediate crude oil. The unit value series is not contained in Haver's JAPAN database, nor reported as such, to our knowledge.The Ministry of Finance reports the yen value of these imports, "petroleum, crude and partly refined", and also the quantity in millions of kiloliters. So, using DLXVG3, we can divide these two series to obtain the unit value. If we used the result as shown, the title of the graph would be the ratio of the codes for the two data series. But we can change that to give it a nicer label: using the drop-down menu under "Graph", we can click on "Titles" and then "Main Titles" to change the wording and the units as we desire. Then, if we want, we can save the modified graph in a "Folder" to be used later. During the New York City transit strike, I have prepared all of these graphs at home and emailed them and their specifications to Haver's office, so that they can be uploaded to this website.

| Japan: Bil.¥ SA except as noted |

Nov 2005 | Oct 2005 | Sept 2005 | Nov 2004 | Monthly Averages|||

|---|---|---|---|---|---|---|---|

| 2004 | 2003 | 2002 | |||||

| Trade Balance | 708.1 | 698.6 | 584.9 | 927.8 | 996.2 | 844.0 | 822.7 |

| Exports | 5894.6 | 5772.9 | 5576.4 | 5272.0 | 5078.6 | 4544.7 | 4339.5 |

| Yr/Yr % Chg (NSA) | 14.7 | 8.0 | 8.8 | 13.4 | 12.1 | 4.7 | 6.4 |

| Imports | 5186.5 | 5074.4 | 4991.5 | 4344.2 | 4082.5 | 3700.7 | 3516.8 |

| Yr/Yr % Chg (NSA) | 16.6 | 17.9 | 17.5 | 28.1 | 10.9 | 5.1 | -0.4 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief