Global| Jun 29 2005

Global| Jun 29 2005Japanese Industrial Output Sluggish; Korea's Grows Unevenly

Summary

Industrial activity in Japan and Korea shows sharply varying patterns, both in recent months and over the past several years. In Japan, mining and manufacturing output in May stood at 100.1, that is, barely above the amount five years [...]

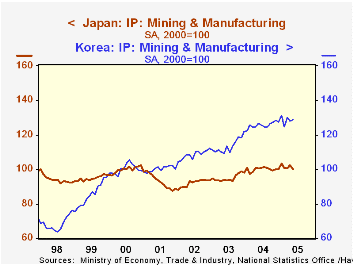

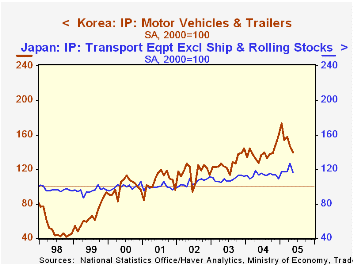

Industrial activity in Japan and Korea shows sharply varying patterns, both in recent months and over the past several years. In Japan, mining and manufacturing output in May stood at 100.1, that is, barely above the amount five years ago for this index based at 100 in 2000. Looking at these endpoints, though, masks the recession in 2001 and a recovery in 2003 and 2004. However, the evolution over the past few months has started to show renewed hesitation. An industry segment in which Japan and Korea compete actively is motor vehicles. For Japan, the corresponding production sector, transport equipment (excluding ships and rolling stock), has been relatively volatile of late, but at 116.3 in May, the sector shows growth since 2000 averaging just over 3%.

Total output in Korea has been considerably more vigorous, with the May 2005 index standing a 128.8, an average annualized gain of 5.1% since the base year in 2000. Despite this attractive average, the gains have been uneven over time and across industries. Chemicals and products have been strong fairly consistently, and radio, TV and communications equipment showed sizable increases in 2003 and 2004, but some recent hesitation. The motor vehicle sector, illustrated in the second graph along with that in Japan, has grown 9% - 10% yearly, but after a spike in December and January, has weakened markedly. These latest declines carried total vehicle production down to the lowest in seven months and to a level just equal to the average monthly output in the last two years. They are probably just an adjustment to that end-2004 surge, but may skittishness some skittishness as world energy prices stay high.

| Indexes, 2000=100, Monthly, Seasonally adjusted |

May 2005 | Apr 2005 | Mar 2005 | Year Ago (Yr/Yr % Chg) | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|

| Japan: Mining & Manufacturing | 100.1 | 102.5 | 100.6 | 100.5 | 100.2 | 95.0 | 92.0 |

| % Change | -2.3 | 1.9 | -0.2 | 0.9 | 5.5 | 3.2 | -1.2 |

| Transport Equipment* | 116.3 | 126.4 | 117.7 | 113.4 | 113.5 | 108.5 | 105.2 |

| % Change | -8.0 | 7.4 | 0.3 | 5.0 | 4.6 | 3.1 | 5.9 |

| Korea: Mining & Manufacturing | 128.8 | 128.0 | 129.9 | 126.6 | 125.7 | 113.7 | 108.4 |

| % Change | 0.6 | -1.5 | 4.3 | 4.0 | 10.8 | 4.9 | 8.1 |

| Motor Vehicles | 139.8 | 146.7 | 157.4 | 127.8 | 139.1 | 127.5 | 116.7 |

| % Change | -4.7 | -6.8 | 1.9 | 9.3 | 9.1 | 9.2 | 9.9 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief