Global| Apr 01 2009

Global| Apr 01 2009Japan TANKAN Makes Heavy Weight for Pre-Summit

Summary

With the advent of Japan’s Tankan report, the US-UK Japan point of view will line up on the side of more stimulus. It is not clear that they have enough support to carry the day, however. Germany is still opposed to more stimulus now [...]

With the advent of Japan’s Tankan report, the US-UK Japan

point of view will line up on the side of more stimulus. It is not

clear that they have enough support to carry the day, however. Germany

is still opposed to more stimulus now and that position has been stated

again today. Both France and Germany want progress on regulation. Each

has said it wants real progress and agreement on a series of key

principles. So it’s not clear how these very different priorities will

play out at the summit. Where the US president says unity is the most

important theme, claiming that differences among G-20 members have been

exaggerated by the press. Wow, no wonder so many newspapers are failing.

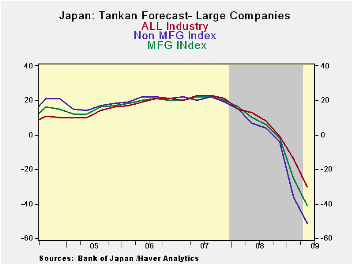

Japan’s Tankan is a worst-ever reading for large corporate

participants in the survey. Each of the survey categories across

various industries points to full period lows. Personal services at

large enterprises are an exception but not much of one.

The MFG reading fell to -58 in Q1-2009 from -24 in Q4-2008.

Non MFG fell to -31 in Q1 from -9 in 2008-Q4.

The MFG outlook index for large firms has dropped to -51 in

2009-Q1 from -36 in 2008-Q4. For non MFG firms the drop in the outlook

is to -30 in Q1 from -14 in 2008-Q4. These are deeply negative numbers

and represent sharp deteriorations from already weak readings in Q4.

Medium and small companies have a similar unraveling in

progress.

Japan has seen its domestic auto production fall sharply as

its exports have been hammered. The exports are lower by over 50%

Yr/Yr. Export markets have generally dried up as recession forces hit

hard on the cusp of the third to fourth quarter last year. Japan is

caught as its main exports are to the US, a very weak economy, and to

China where some growth remains in train but where its exports, too are

being clobbered. As of January US imports from Japan are down by 30%

Yr/Yr. Japan is burdened by a large outstanding balance of public debt

and as a rising yen value has crimped its competitiveness in a fading

market.

| Tankan Results Large Enterprises | |||||||

|---|---|---|---|---|---|---|---|

| Readings | Averages | PERCENTILES | |||||

| Q1-09 | Q4-08 | Q3-08 | Q2-08 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG | -58.0 | -24.0 | -3.0 | 5.0 | -41.0 | 12.1 | 0.0% |

| NonMFG | -31.0 | -9.0 | 1.0 | 10.0 | -20.0 | 11.7 | 0.0% |

| Total Industry | -45.0 | -16.0 | 0.0 | 7.0 | -30.5 | 11.9 | 0.0% |

| Construction | -27.0 | -10.0 | -7.0 | -1.0 | -18.5 | -4.5 | 0.0% |

| Real Estate | -21.0 | -7.0 | 5.0 | 22.0 | -14.0 | 27.7 | 0.0% |

| Wholesale | -44.0 | -7.0 | 11.0 | 12.0 | -25.5 | 14.1 | 0.0% |

| Retail | -42.0 | -18.0 | -5.0 | 0.0 | -30.0 | 2.5 | 0.0% |

| Transportation | -46.0 | -7.0 | 6.0 | 16.0 | -26.5 | 10.9 | 0.0% |

| Services 4 Biz | -21.0 | -1.0 | 4.0 | 20.0 | -11.0 | 20.0 | 0.0% |

| Personal Serv | -9.0 | -11.0 | 6.0 | 10.0 | -10.0 | 8.7 | 6.7% |

| Restaurants & Hotels | -45.0 | -32.0 | -13.0 | -14.0 | -38.5 | 1.9 | 0.0% |

| Forecast | |||||||

| Q2-09 | Q1-09 | Q4-08 | Q3-08 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG-OtLk | -51.0 | -36.0 | -4.0 | 4.0 | -21.8 | 10.4 | 0.0% |

| NonMFG -Otlk | -30.0 | -14.0 | -1.0 | 8.0 | -9.3 | 11.4 | 0.0% |

| All Industry-Otlk | -41.0 | -25.0 | -2.0 | 6.0 | -15.5 | 10.8 | 0.0% |

| Tankan Results Medium Enterprises | |||||||

| Q1-09 | Q4-08 | Q3-08 | 1-Y Avg | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG | -57.0 | -24.0 | -8.0 | -22.8 | -22.8 | 1.5 | 0.0% |

| NonMFG | -37.0 | -21.0 | -12.0 | -18.8 | -18.8 | -3.3 | 0.0% |

| Forecast | |||||||

| Q2-09 | Q1-09 | Q4-08 | Q3-08 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG-OtLk | -61.0 | -45.0 | -12.0 | -5.0 | -30.8 | -2.0 | 0.0% |

| NonMFG -Otlk | -45.0 | -32.0 | -17.0 | -10.0 | -26.0 | -5.6 | 0.0% |

| All Industry-Otlk | -51.0 | -38.0 | -15.0 | -9.0 | -28.3 | -4.1 | 0.0% |

| Tankan Results Small Enterprises | |||||||

| Q2-09 | Q1-09 | Q4-08 | Q3-08 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG | -57.0 | -29.0 | -17.0 | -43.0 | -43.0 | -5.5 | 0.0% |

| NonMFG | -42.0 | -29.0 | -24.0 | -35.5 | -35.5 | -14.9 | 0.0% |

| Total Industry | -42.0 | -29.0 | -24.0 | -35.5 | -35.5 | -14.9 | 0.0% |

| Forecast | |||||||

| Q2-09 | Q1-09 | Q4-08 | Q3-08 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG-OtLk | -63.0 | -48.0 | -25.0 | -15.0 | -37.8 | -8.2 | 0.0% |

| NonMFG -Otlk | -52.0 | -42.0 | -31.0 | -27.0 | -38.0 | -19.0 | 0.0% |

| All Industry-Otlk | -56.0 | -44.0 | -29.0 | -22.0 | -37.8 | -15.1 | 0.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief