Global| Oct 01 2004

Global| Oct 01 2004Japan "TANKAN" Better Than Forecast for Q3

Summary

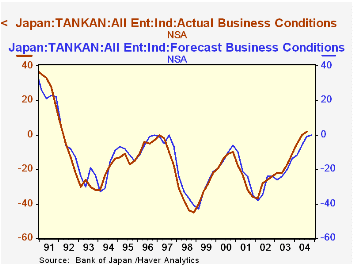

Japanese business prospered more in Q3, relative to both the Q2 performance and to their own expectations for Q3. In the Bank of Japan's huge TANKAN survey (10,312 firms), all size firms in all industries garnered a reading of +2, up [...]

Japanese business prospered more in Q3, relative to both the Q2 performance and to their own expectations for Q3. In the Bank of Japan's huge TANKAN survey (10,312 firms), all size firms in all industries garnered a reading of +2, up from 0 in Q2 and an expectation of -1. The better known "headline series" of large manufacturing firms came in at +26 compared with Q2's +22 and a forecast of +21. Every broad size category, large, medium and small, as well as the manufacturing/non-manufacturing breakdown, had better readings.

Among individual industries, large firms in lumber, paper, petroleum, building products, iron and steel and shipbuilding all exceeded their Q3 forecasts by more than 10 points. By contrast, large firms in a few industries did fall short of projections, including textiles, some metals and machinery, transportation and business services. The retailing sector remained weak, with negative results in all firm-size groups which were also less than expected.

Some commentators speaking to the press this morning expressed the view that this report might mark a peak for business activity in Japan. They cite the survey's own forecast of moderation in December, as well as high energy prices and the deliberate policies of restraint in the big neighboring economy, China. It's possible that the latter two fundamental factors will hold sway in slowing Japanese growth, but the mere fact that the forecast points to slower growth in December should probably be taken cautiously; so far this year businesses' forecasts have underestimated economic gains pretty consistently.

In the Haver databases, we present the TANKAN data two ways. Owing to the restructuring of the survey classification scheme and new sampling last March, we have segregated the recent detail data into new series in the "Japan" database. In summary data in the "G10" database, we link the all industry-all enterprise data with the history that uses the old methodology. This broad aggregate is less affected by the Bank of Japan's reorganization of the categories. By this special, linked measure, the Q3 result at +2 is the first positive reading since Q1 of 1992, more than 12 years ago.

| Business Conditions: % Favorable minus % Unfavorable | September 2004 June 2004 March 2004||||||

|---|---|---|---|---|---|---|

| Actual | Forecast for Dec | Actual | Forecast for Sept | Actual | Forecast for June | |

| All Firms | 2 | 0 | 0 | -1 | -5 | -6 |

| Large Firms* | 19 | 15 | 16 | 16 | 9 | 9 |

| Manufacturing ("Headline Series") | 26 | 21 | 22 | 21 | 12 | 12 |

| Non-manufacturing | 11 | 10 | 9 | 11 | 5 | 7 |

| Medium-sized Firms** | 5 | 3 | 3 | 1 | -2 | -2 |

| Manufacturing | 14 | 10 | 11 | 7 | 5 | 1 |

| Non-manufacturing | -2 | -2 | -1 | -3 | -7 | -6 |

| Small Firms*** | -9 | -9 | -10 | -10 | -13 | -15 |

| Manufacturing | 5 | 3 | 2 | 2 | -3 | -3 |

| Non-manufacturing | -17 | -16 | -18 | -18 | -20 | -21 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief