Global| Aug 12 2013

Global| Aug 12 2013Japan Slows Quarter-to-Quarter

Summary

Abe's economics (Abe-nomics) is not exactly stumbling, but neither is it hitting the home run that it seemed to be when the program first was launched. GDP in the second quarter is up at a stronger pace year-over-year at 0.9% compared [...]

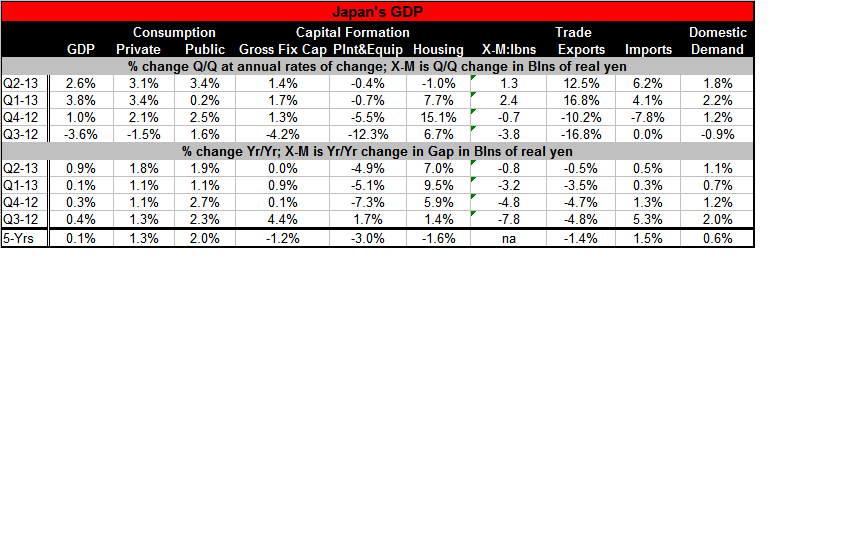

Abe's economics (Abe-nomics) is not exactly stumbling, but neither is it hitting the home run that it seemed to be when the program first was launched. GDP in the second quarter is up at a stronger pace year-over-year at 0.9% compared to 0.1% in Q1. But quarter to quarter the pace of GDP growth has slowed to a 2.6% annual rate from a 3.8% annual rate.

Abe's economics (Abe-nomics) is not exactly stumbling, but neither is it hitting the home run that it seemed to be when the program first was launched. GDP in the second quarter is up at a stronger pace year-over-year at 0.9% compared to 0.1% in Q1. But quarter to quarter the pace of GDP growth has slowed to a 2.6% annual rate from a 3.8% annual rate.

Private consumption spending slowed quarter-to-quarter growing at a 3.1% annual rate compared to 3.4% in the first quarter. Government spending picked up quite strongly, in the quarter growing at a 3.4% annual rate pace compared with a 0.2% pace in the first quarter. Significantly, government spending is pushing the economy forward right now more than private consumption (or investment) spending. Yet, one of the objectives of the Abe administration is to launch a consumption tax to deal with the extraordinarily high debt to GDP ratio in Japan. The government sector is still providing the bulk of the stimulus in 2013-Q2. With the private sector having slowed down slightly in the second quarter, the new GDP result may put plans for some fiscal consolidation on the back burner.

Gross fixed capital formation slowed to a 1.4% annual rate in the second quarter compared to 1.7% in the first quarter. Private plant and equipment spending declined by 0.4% at an annual rate, a slight improvement from the 0.7% annual rate drop in the first quarter. Also, housing, slipped after posting a 7.7% annual rate in Q1 as sector spending fell at a 1% annual rate in the second quarter. Housing investment still has an impressive 7% growth rate year-over-year; plant and equipment spending is falling at a 4.9% annual rate year-over-year.

The contribution of international trade to GDP produced a positive impulse of 1.3 billion but that was less than the 2.4 billion in the first quarter-actually leading to a Q-to-Q detraction from GDP. Exports decelerated but to a still strong growth rate of 12.5% after growing at a 16.8% rate in the first quarter. However, imports of picked up after going 4.1% in the first quarter as they surged at a 6.2% annual rate in Q2. Year-over-year exports are falling by 0.5% as imports are rising by 0.5%. In the annual treatment of GDP the trade sector is still a drag on GDP growth.

Domestic demand has improved but it did slow quarter to 1.8% annual rate of growth in the second quarter, below the first quarter pace 2.2%. But that Q2 pace is still above the 1.1% year-over-year growth rate. It's also higher than the year-over-year growth rates back until Q3 of 2012.

It's not clear that Japan's policy should dwell so much on the second quarter figures compared to the first. If it does that, and the performance of GDP is found wanting, the potential for taking fiscal action is much reduced. However, if Japan evaluates the second quarter numbers compared to the previous trend, there is still a clear pickup in the economy even though there is also a bit of a slowdown quarter to quarter.

Japan's fiscal policy decision is in a box similar to that of monetary policy in the United States. The Federal Reserve declared an intention to taper its easing policies and then saw economic growth revised down and economic statistics turn mixed and in some cases weaker. Now the course of US monetary policy is also up in the air.

Japan's huge debt to GDP ratio means that it has to begin to take some kind of action. There is talk of more of a national program to try to stimulate household formation in childbirth. Japan continues to be opposed to solving there contracting population problem with immigration. Japan continues to be very homogeneous nation with many shared national objectives in a culture that sees a great deal of symbiosis, although it's Westernization in recent years has eroded some of those traditional values.

It's not clear where the Abe administration is going to go with its policy objectives next. There has been opposition to the idea of a consumption tax to address Japan's large fiscal deficit and debt situation. Japan has in the past raised consumption taxes just as the economy was beginning to grow and discovered that it had raise taxes too soon and that the tax helped to nip a rising growth rate in the bud. We will have to watch the Abe administration for signs that either it's going to put this policy on hold or that it's going to press ahead because it thinks growth can take the shot of a tax increase.

In any event, Japan's growth is better than it was. The 0.9% growth rate is the strongest year-over-year rate since second quarter of 2012. In Q1 and Q2 of 2012 it posted two year-over-year growth rates above 3%. However, the key to Japan is not how large of a quarterly growth rate it can produce, but whether it can sustain growth and reverse deflation. Those objectives remain 'job one' although getting control of the debt as an objective is close on the heels of those two needs.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief