Global| Aug 20 2013

Global| Aug 20 2013Japan Sector Indices Show Recovery

Summary

Japan's economy continues to dig out after its long period of lethargy, after having been embroiled in a global financial collapse, and then, after being struck by an earthquake, a tsunami and a nuclear disaster, the latter being like [...]

Japan's economy continues to dig out after its long period of lethargy, after having been embroiled in a global financial collapse, and then, after being struck by an earthquake, a tsunami and a nuclear disaster, the latter being like extruded toothpaste that Japan is still trying to put back in the tube.

Japan's economy continues to dig out after its long period of lethargy, after having been embroiled in a global financial collapse, and then, after being struck by an earthquake, a tsunami and a nuclear disaster, the latter being like extruded toothpaste that Japan is still trying to put back in the tube.

The chart shows the relatively sharp rebound of the construction sector in Japan. The sector took some time to recover from Japan's disasters but has recovered and is moving ahead strongly. The Industry index and the Tertiary index, the latter which depicts conditions in the services sector, are also on the mend.

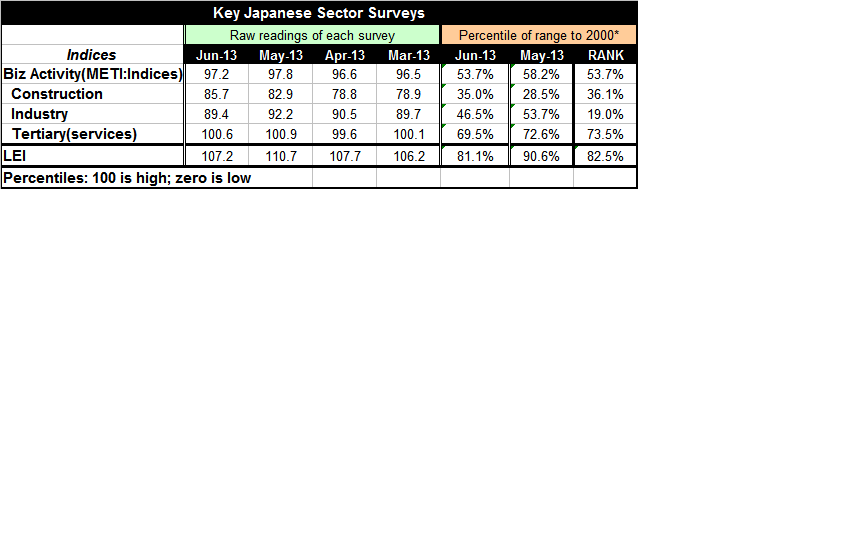

At the far right of the table we present these three sectors as a percentile standing for two months and as a rank standing for the current month in their respective historic range of values since the year 2000. The high-low percentile positions for May and June evaluate the overall activity index as being in its 53rd percentile in June. Among the sector indices the services sector is the strongest at its 69.5 percentile in June.

The high low rankings are useful but we think that the ranking standings are a better description of the relative standings of the various sectors. Those metrics are in the very far right-hand column. The high-to-low percentiles only position the current index between the highest and lowest values of the time chosen. In contrast, the rank data use every single observation to place this month's observation in the historic queue of values. The rank describes where the current month sits in the percentile ranking of all these values. On this basis it's the tertiary or services sector that's doing the best in the 73rd percentile of its historic range; and it is slightly stronger than in the high-to-low ranking format. That standing has helped to carry the overall business activity index up to the 53.7 percentile of its queue. The construction sector that's been so strong in the most recent months is only up to 36th percentile of its historic range. Industry is still very weak in the bottom one-fifth of its historic queue but is relatively (and substantially) stronger in its high-to-low range at the 45th percentile. While Japan's construction sector is providing the near-term surge for output, it is the services sector that continues to climb and is the closest to restoring an important sector to a position of historic normalcy. There is no sector that is restoring prosperity.

Similarly we provide an assessment of the leading economic index. The LEI in June sits at the 81st percentile of its high low range and at about the 82nd percentile of its ranked queue; it sits at approximately the same relative position in both of these treatments. The LEI is stronger than the sector indices from METI. Since the LEI purports to look ahead while the METI indices are simply evaluators of current activity, this is a hopeful signal.

Japan's recovery is substantially a recovery based upon a shift in government policy that has prodded the central bank to take a more activist stand. While we can look at the decade-long slump in Japan, the financial crisis, the impact of the tsunami and of the nuclear disaster as a series of events that buffeted Japan's economy, along with them came an overly-strong yen whose repressive effects were at least as harsh. The more aggressive easing policy by the Bank of Japan has reversed the trend of the yen and the yen's new path is an important reason why Japan's version of quantitative easing is working on such a short lag. The yen clearly had become overly-strong and was strangling the Japanese economy, an economy that was beset with a series of other ills.

Despite this move in the yen, Japan's trade picture continues to be uneven with its trade position still in deficit; that is largely a result of substantial imports of oil that are replacing Japan's past reliance on nuclear power.

Japan's policymakers recognize that past policies have painted them into a corner and they are doing what they can to try to extract themselves from the trap. A tax hike is proposed to try to address the high debt to GDP ratio. But there are concerns that it's too early for a consumption tax increase that could short-circuit the revival of growth and push Japan back into another period of lethargy. Were that to happen the debt to GDP ratio would rise further and the tax hike gambit would backfire. Japan is also aware of how its slow population growth interacts with its high debt to GDP ratio to create a tremendous challenge for the future. Policies are in gear to try to stimulate family formation and to revive population growth.

In Japan, perhaps more than any place else, the policy steps taken by the administration are the most important things determining whether not the economy will actually have escape velocity to keep backsliding at bay. Prime Minister Abe has declared that the episode of deflation is over. He may be right. But it seems that the success or failure of this statement is going to depend upon his administration's judgment and actions. Unfortunately, Abe has conflicting goals, a heavy legacy of bad decisions from previous administrations to overcome, and the clock is ticking on the future.

I am somewhat more encouraged about Japan's prospects than some economists because I think unlike any other economy in the world the Japanese people tend to pull together in a crisis. It's more than having a government creating an edict for people to act in a certain way. Japan is a nation that perceives itself as largely homogeneous and that recognizes more shared interests than do the people in most industrialized economies and that provides for more upward mobility based on merit. Since Japan owes most of its debt to itself, to its own people, I am relatively more certain that it will be able to find a way out of its difficulties despite the enormous burden of that debt. Japan, among all highly industrialized countries, has been able to deal with shared responsibilities and shared burdens. Its society typically has less stratification and gaping in its income distribution. It tends to recognize the needs and rights of all of its workers regardless of their station in life and through this lens it is more likely to be able to figure out a path to a more successful future. I think that simply applying typical Western macroeconomic policy to Japan and assuming that we will see a repeat of some of the debt problems we've seen in Europe is unlikely. Still, Japan is going to have a difficult time digging itself out. Its problems are severe and the solutions to them are not obvious. But it now has focus.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief