Global| Sep 21 2016

Global| Sep 21 2016Japan's Yen Surplus Snakes Higher As BOJ `Reinforces' Its Easing

Summary

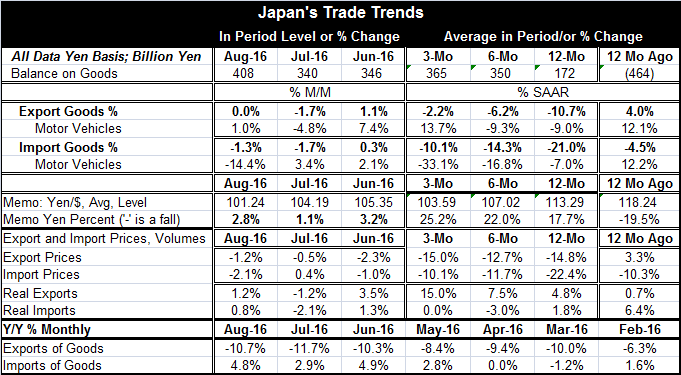

Japan's `swing to surplus,' now 10 months old, continues in August and advances its cause (slightly). The excess of goods exports over goods imports is now the best since April of this year and before that the surplus was last higher [...]

Japan's `swing to surplus,' now 10 months old, continues in August and advances its cause (slightly). The excess of goods exports over goods imports is now the best since April of this year and before that the surplus was last higher in February 2011 after which a string of deficits took hold of Japan's trade as its nuclear utilities capability was taken offline and oil imports surged as a replacement fuel.

Japan's `swing to surplus,' now 10 months old, continues in August and advances its cause (slightly). The excess of goods exports over goods imports is now the best since April of this year and before that the surplus was last higher in February 2011 after which a string of deficits took hold of Japan's trade as its nuclear utilities capability was taken offline and oil imports surged as a replacement fuel.

Fukushima date-stamp

The Fukushima disaster dated to March 11, 2011. Japan's trade picture shifted markedly in the wake of that disaster and is only now being rebuilt.

Ongoing improvement

Japan's trade trends are not yet `warm and friendly', but there is improvement in train. The goods trade balance chart shows that the trend for the goods balance has been improving since it ballooned to its peak deficit reading in March 2014.

The underlying trends

Separately, trends for Japan's exports and imports are both `improving.' First of all, export growth is still negative over three-months, six-months and 12-months. But the annualized rates of growth each are diminishing sequentially. The same is true for imports. Of course, for imports, the negative rates of growth are still larger (in absolute value) than for exports, explaining why trade is improving. To recap: both exports and imports are still falling but each is falling by less and imports are still the relatively weaker flow- but that's still progress.

The FX factor

Still, over this period, the yen has gradually been rising. The yen is up by 17% vs. the dollar over 12-months and rising over shorter horizons at a pace in excess of 20%. A rising yen tends to depress both export and import prices and to undermine Japan's competitiveness on global markets. A stronger yen should eventually speed import volume and lower export volume.

Export and import prices

In fact, Japan's export and import prices are falling on all horizons, but generally the pace of the price drop (annualized) is slowing over shorter periods. This sort of price `firming' is good news but it is not true firming yet; it is just less weakness. Over three-months, Japan's export and import prices still are falling at double-digit annualized rates.

Real export and import trends

Surprisingly, adjusted for inflation and converted to quasi `volume' terms, Japan's exports show life! Exports on this basis are up month-to-month in two of the last three-months. And export volumes are progressively accelerating from 12-months, to six-months to three-months. The growth rate progresses from about a 5% pace over 12-months to 15% over three-months. Imports, however, still show weakness. They are up by only 1.8% in `volume' terms over 12-months and dead flat over three-months. Japan's domestic demand is just not reflating in real terms.

Japan's growth/the BOJ move

Japan still faces huge hurdles for growth as its population shrinks, deflation still rules and growth overseas has been a weak tug for its exports. Japan's export growth has suffered from the impact of the rising yen as well as weak growth globally, especially a slowing of growth in its main market, China. The Bank of Japan is trying hard to break the inflation psychology with aggressive monetary policy and to hit its 2% inflation target. Its new policy announcement today is meant to try to reassure markets and to advance the stimulative effects of monetary policy while eliminating the potential adverse side-effects of a negative rate policy. Japan is trying to hold the 10-year rate in place while it keeps options open for more stimulus in other aspects of policy. This tact, used in the U.S. several times with less than success, has been called `operation twist' as the central bank tries to twist or control the yield curve, bending it to its will.

Problems with Operation Twist

Quite apart from being hard to implement, this policy is received less than enthusiastically by many economists. Many economists are already put out by the degree and nature of outright monetary stimulus: its magnitude as well as the asset classes it already includes. Their ire grows as the central banks tries to dip another tentacle into the capital markets and `control' the long-term rate effectively shutting down the market's own assessment of and reaction to central bank stimulus. To some extent, you can think of it as suppressing the market's free-speech. So if the bank can implement the policy successfully, it is still not clear that the policy will have the intended effect since it will be unclear if market expectations are aligned with the policy tilt or not. One thing this sort of approach does is to blunt the market's ability to react to and give signals about its assessment of the effectiveness of the action that the central bank is pursuing. That is a secondary concern to whether the BOJ will be able effectively to actually bend the yield curve to its will.

Japan's reinforcement of easing: the nuts and bolts

The BOJ is going to attempt to keep the 10-year yield at zero and to adjust its securities purchases to make that rate stick. One thing that makes this different than the U.S. operation twist is the Japan is targeting the 10-year yield and apparently will not be `wedded' to a short-term rate target, but for now this aspect of policy is still left somewhat fuzzy. Still, there are issues here; long-term rates (call them bond yields) are affected by a larger variety of variables than short rates. If the BOJ is to truly stabilize yields, it may wind up transferring the variability that the 10-year yield would otherwise have to short-term rates or to its activities of securities purchases. In theory (famous last words), the BOJ should be able to do this. In practice the price of doing, it may prove to be too dear. Japan calls this plan a reinforcement of easing. We will see if in practice it works or is workable and if the plan can help the bank to hit its 2% inflation target which is the goal of the program.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief