Global| Jun 20 2016

Global| Jun 20 2016Japan's Trade Trends Wither

Summary

Japan is getting a boost to growth through its external sector. Its trade surplus is growing. But the boost is not the type we like to see. Japan's exports are falling year-over-year, but since imports are falling by more the trade [...]

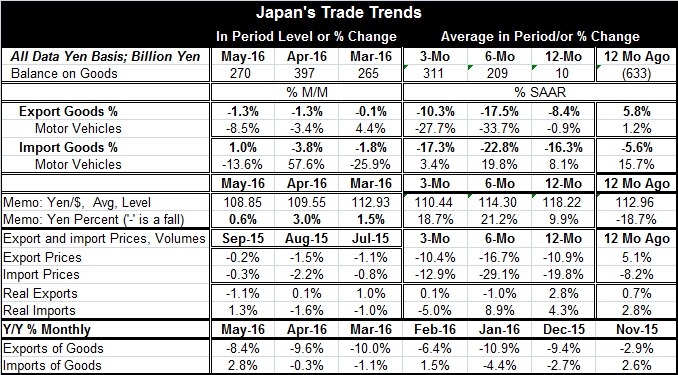

Japan is getting a boost to growth through its external sector. Its trade surplus is growing. But the boost is not the type we like to see. Japan's exports are falling year-over-year, but since imports are falling by more the trade surpluses rises and that feeds into a positive contribution for GDP. When trade affects growth in this manner, I do not think of it as boosting growth as much as softening the blow in a weak economy. Imports would not be falling unless domestic demand remained weak. No economy will ramp itself up into stronger GDP growth on the back of sinking imports. Sinking imports are an automatic stabilizer than tends to breathe some life back into weakening GDP.

Japan is getting a boost to growth through its external sector. Its trade surplus is growing. But the boost is not the type we like to see. Japan's exports are falling year-over-year, but since imports are falling by more the trade surpluses rises and that feeds into a positive contribution for GDP. When trade affects growth in this manner, I do not think of it as boosting growth as much as softening the blow in a weak economy. Imports would not be falling unless domestic demand remained weak. No economy will ramp itself up into stronger GDP growth on the back of sinking imports. Sinking imports are an automatic stabilizer than tends to breathe some life back into weakening GDP.

Japan's main trading partner is China. When we find weak exports in Japan, it likely reflects Chinese domestic demand weakness as well. Japan's nominal exports are falling at a double digit pace over three-months and six-months, but the pace of decline is not cumulating.

Motor vehicle trends

Japan's motor vehicle export and import trends are somewhat peculiar. Imports have been very volatile in the past few months, rising and falling at outsized rates of growth. Overall imports of motor vehicles are growing but may be losing momentum as their pace at 3.4% over three-months compares to an 8.1% pace over 12-months. Motor vehicle exports are lower in two of the last three-months and clearly weaker over three-months and six-months than over 12-months. Over three-months and six-months, motor vehicle exports are contracting at a pace near 30%.

Prices

Some of this weakness is price weakness as both export and import prices are falling by double digits over all horizons of one year or shorter in the table (including monthly). The yen has been rising by nearly 10% over 12-months and rising even faster on shorter horizons. A stronger yen exchange rate will tend to push Japanese export prices down and to reduce import prices as well. Import prices are also being bounced around by commodity prices which have been volatile but are mostly lower over the last three-months.

Trade volumes

Export and import volumes (real exports and real imports in the table) show that trade volumes are nonetheless expanding over 12-months. Imports are up by about 4% while exports are up by less than 3%. Exports are weaker on balance over three-months and six-months while imports show some life over six-months then weaken sharply over three-months. There is nothing in the export or import trends that I find encouraging.

BoJ admits to missing goal

Today Mr. Kuroda officially admitted that the Bank of Japan has failed to boost inflation has it had tried to do. He noted in this remarks how hard it is to break inflation expectations when there is such a legacy of price weakness that continues to affect perceptions.

The dollar and Brexit

Other news was more upbeat with the dollar breathing some life into overseas stocks and by raising oil prices. Markets firmed a bit on the news that the `in-crowd' seems to be gaining momentum on Brexit after a run of strength from the `out crowed' last week.

Quite a week ahead

Globally growth continues weak. With the Fed backing off from its program of normalization, all bets are off as to what it does next. The dollar still seems to be somewhat well-bid, indicating that markets expect the U.S. to remain on the rate-hike warpath at some point. This week should be pivotal because the Fed Chair will give two testimonies on U.S. monetary policy, one each before the Senate and House Fed oversight committees. Last week we learned that the Fed members were cutting their view on the path of interest rates. In the week ahead, we may find out why the outlook for rates changed and if the Fed has any new policy-parameters we need to keep an eye on. Of course, Thursday brings the Brexit vote and everyone will be looking ahead to that. As of today, the Brexit situation is looking a bit less volatile but you never can be sure. Polls can shift at the last minute or simply prove to have been not well anchored in the reality of the electorate's views. The moment of decision approaches.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief