Global| Apr 20 2017

Global| Apr 20 2017Japan's 'Trade Trends' Stabilize on an Unstable Foundation

Summary

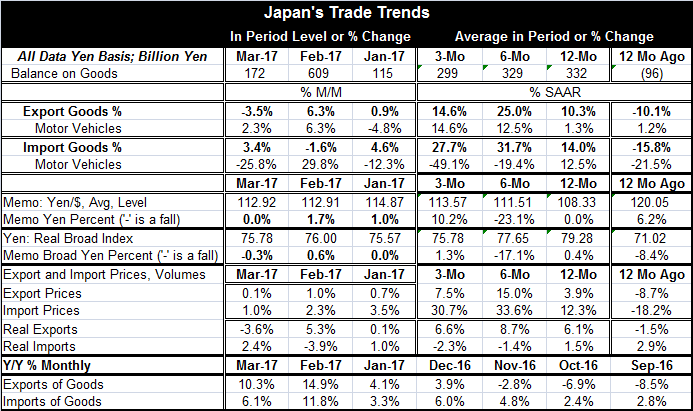

Japan trade trends, broadly considered, seem to be stabilizing. At 172 billion yen, Japan's March surplus is lower than in February but higher than January and about 100 billion yen below its three-month average. But in broad terms, [...]

Japan trade trends, broadly considered, seem to be stabilizing. At 172 billion yen, Japan's March surplus is lower than in February but higher than January and about 100 billion yen below its three-month average. But in broad terms, the surplus position seems to be stabilizing in this range that is somewhat lower than its 12-month average but above its previous 12-month average which was in deficit.

Japan trade trends, broadly considered, seem to be stabilizing. At 172 billion yen, Japan's March surplus is lower than in February but higher than January and about 100 billion yen below its three-month average. But in broad terms, the surplus position seems to be stabilizing in this range that is somewhat lower than its 12-month average but above its previous 12-month average which was in deficit.

Trade trends: value, volume and price

For now both exports and imports are posting double-digit growth rates over 12 months, six months and three months. Of course, the import value figures are boosted by higher oil prices. Looking farther down the table, we find export and import volumes and prices. The story there shows export prices up by 4% over 12 months and expanding at higher growth rates over six months and three months (annualized). For imports, prices are up by 12% over 12 months and at growth rates of 30% or more over six months and three months on rising oil import prices. Lower in the table are the trade volume data that show export volumes have been reasonably steady with 12-monht to three-month growth rates in a range of 6% to 9%. Real imports show a gain of only 1.5% over 12 months and a range in growth rates on that same span of -2.3% to 1.5%. With import prices rising so fast, import volumes are reacting adversely.

Fundamentals

As for the fundamentals underlying the trade surplus, Japan's export value trends are solid, built on rising volumes and prices. Import volumes are weak; that should push the surplus up. But volumes are not as weak as import prices so import values for the moment have surged but because of their link to oil prices- that should not last. Meanwhile, export prices show some life and will augment what appears to be steady export volume as global trade flows firm. Half of the trade picture is on very solid ground and the other half seems poised to improve as oil prices stop rising (...when they stop rising).

FX effects

The broad real yen index has fallen slightly over 12 months but is mostly stable on three-month and six-month horizons. The falling index would be expected to add slightly to import prices are to allow faster yen-currency gains in export prices even as foreign currency-based yen prices fall increasing Japan's competitiveness and augmenting its export pace. Of course, Japan is still one of six nations on the U.S. foreign exchange rate manipulation list.

Japan: a brief macro overview

Japan's economic data generally show some continuing advancement. This week Moody's review of Japan found some evidence of reflation. Over the last three months, the LEI has held to slightly higher levels than it did previously, but there is no surge indicated. The Miti and Teikoku sector indexes generally show expansion. Order growth, volatile as it is, seems on track for expansion. Japan's manufacturing PMI has been steady showing moderate expansion is in place. Services are expanding. Japan's core consumer prices are rising.

Japan's trade and economic trends: summing up

The trade data reflect moderate economic growth and for now a cessation of deflation forces. But with a tailwind from oil prices, that is still not a decisive 'win' for the BOJ. Its policies continue to be full bore into backing stimulus. Japan is benefiting from the pickup in global growth that the IMF sees as it is well plugged into the global economy with its strongest connection to China and with the U.S. in second position. For now Japan seems to be on an even keel. It is dealing with the oil price surge as are all other oil-importing countries. Japan seems to be in a stable position for now. And while that is good, it still fails to show any real acceleration. The pickup in prices is too weak and mixed to hang your hat on as oil prices begin to waffle on world markets. Japan continues to fight the ongoing forces of deflation that comes from having a shrinking population.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief