Global| Jun 16 2021

Global| Jun 16 2021Japan's Trade Surplus Withers As Nominal Exports and Imports Surge

Summary

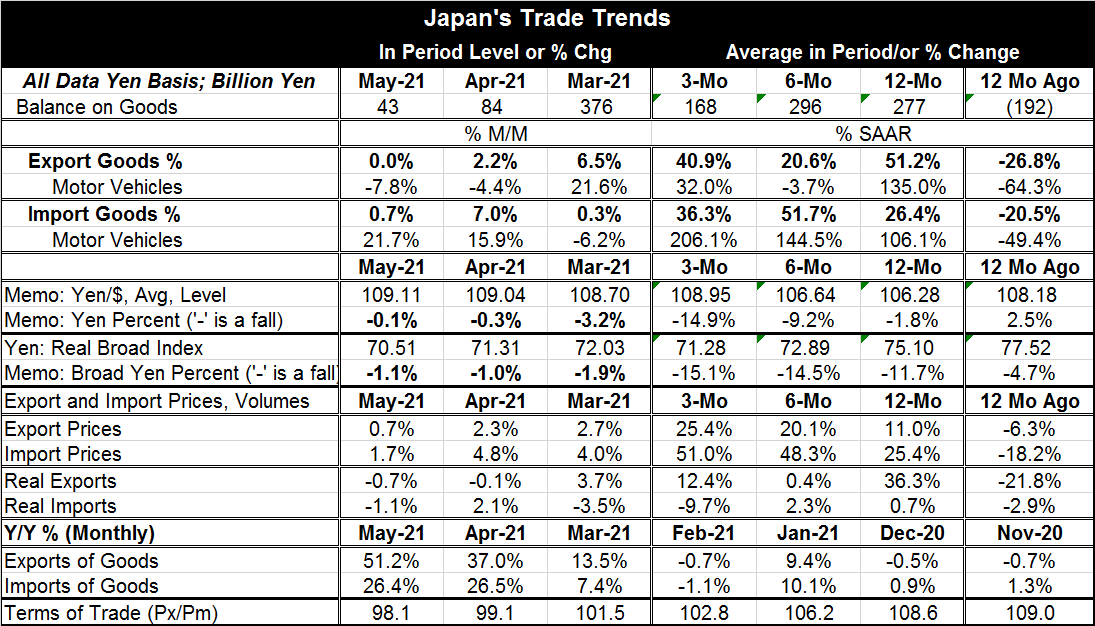

Japan's trade surplus eroded to Ą43bln in May from a surplus of Ą84 bln in April. Compared to its six-month and 12-month averages, the three-month average balance shows a much reduced trade surplus. Japan's exports were dead flat in [...]

Japan's trade surplus eroded to ¥43bln in May from a surplus of ¥84 bln in April. Compared to its six-month and 12-month averages, the three-month average balance shows a much reduced trade surplus.

Japan's trade surplus eroded to ¥43bln in May from a surplus of ¥84 bln in April. Compared to its six-month and 12-month averages, the three-month average balance shows a much reduced trade surplus.

Japan's exports were dead flat in May while imports rose by 0.7%. Imports have now outpaced exports for two months in a row. But over three months, export growth prevails. Exports show an annualized growth rate of 40.9% compared to 36.3% for imports.

Neither exports nor imports show clear trends in their progression of 12-month to six-month to three-month growth rates. But the chart shows that the 12-month growth rates for exports and imports continue to move higher from early-to-mid 2020 even as the trade balance has swung to larger surpluses then swung back to a progression of smaller surpluses.

The yen exchange rate has withered slightly over the past year. That is both against the dollar as well as on a broad trade-weighted basis. Against the dollar the yen is lower by 1.8% over 12 months, but on a broader basis the yen is lower by 11.7%.

Focusing on 12-month changes, real exports (or export volume) are up by 36.3% over 12 months as import volume is higher by only 0.7%. This mix is reversed for prices as export prices are up by 11% over 12 months compared to import prices that are up by 25.4% over 12 months. Nominal exports are up by 51% over 12 months nearly twice the gain of nominal imports whose gain of 26.4% is almost all due to price increases. Exports from Japan are strong; imports are weak.

The monthly series on year-over-year nominal exports and imports show that exports have been outpacing imports on this metric for four months in a row. Japan's exports have been helped by the fact that U.S. growth has stepped up led by very strong consumer spending that has outstripped U.S. production growth leaving a big hole for imports (i.e., for foreign exports to fill). At the same time, Japan's largest trade partner, China, has stepped up its activity. This improvement in its two main trading partners is helping Japan to grow.

Plans to hold the Olympics in Japan are a ‘Go.' The games are scheduled to begin July 23 and to progress through August 8. The virus continues to show a withering trend for infections as well as for deaths. Japan is making the progress it needs to make its economy safe for the Olympics. But Japan's restrictions on activity to support containment of the virus have had an adverse impact on growth. That is one of the reasons that Japan's import volume is so weak. At the same time, Japan's nominal imports have been greatly inflated by the price of oil since Japan is a profligate oil importer.

Overnight Japan's machinery orders data were refreshed. Core machinery orders are up by 0.6% month-to-month in April. While that is an increase, it's a small one and a smaller gain than expected, especially in the wake of an order decline one month ago. While Japan is getting some stimulus from its trade partners' growth pick up, it is still having a hard time getting growth rolling.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief