Global| Sep 17 2015

Global| Sep 17 2015Japan's Trade Erosion Abates Slightly in August

Summary

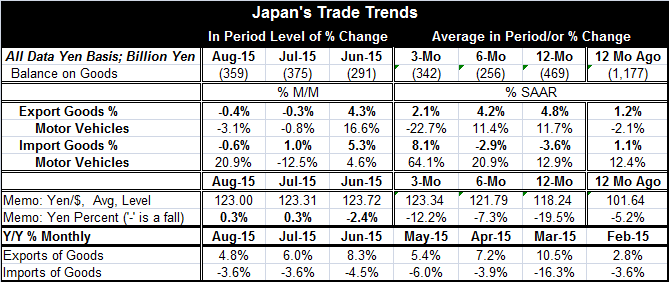

On a trend basis, Japan's exports are still stronger than its imports; thus, a move to surplus should still lie ahead for Japan. However, in the last few months, the import decline has abated (month-to-month growth) and imports have [...]

On a trend basis, Japan's exports are still stronger than its imports; thus, a move to surplus should still lie ahead for Japan. However, in the last few months, the import decline has abated (month-to-month growth) and imports have grown as exports have weakened. Is there a new trend afoot?

On a trend basis, Japan's exports are still stronger than its imports; thus, a move to surplus should still lie ahead for Japan. However, in the last few months, the import decline has abated (month-to-month growth) and imports have grown as exports have weakened. Is there a new trend afoot?

Year-over-year exports are up 4.8% as imports are falling by 3.6%. That disparity in growth rates causes a move toward surplus. In the chart, you can see that the deficit is smaller currently than it was 12 month ago. Over six months, export growth is at a slower 4.2% pace as imports fall by more slowly at a -2.9% pace. Over three months, exports slow further to 2.1%. Meanwhile, on this horizon, imports are suddenly surging, rising at an 8.1% pace. These trends are reflected, too, in the trends for motor vehicles where exports have slowed and imports have speeded up.

The outlook for trade depends on whether the short-term trends have taken over or whether the long-term trends will reassert themselves.Japan as an economy continues to struggle. S&P has just downgraded Japan because it does not see any turnaround soon. China is slowing and it is Japan's largest trade partner. That will pose an added burden for Japan to get growth going.

If Japan cannot get its export growth going, there is little chance that the pick-up in imports will remain in force. Japan has substantial domestic demand. But its international performance is also very important. Japan has an enormous fiscal deficit and the government still has plans to raise the consumption tax again at some unnamed point in the future. Of course, that plan remains dormant as long as the economy is so weak. There will be no fiscal help for growth in Japan, quite the contrary. So it is not reasonable to think that the domestic economy is going to continue to perform well if the international part is under pressure. I do not see the pick-up in imports as sustainable for that reason.

Japan's currency has continued to make steady losses. It is lower by 12% over three months and by nearly 20% over 12 months. The rise in competitiveness does not help Japan's growth that much because it has outsourced so much of its production. Still, there is some impact.

In the deficit data depicted in the chart, you can see clearly the short-run and long-run trends at work. Japan's deficits have gotten much smaller over the last six months than any time since early 2011 when it was running persistent surpluses. But over this short six-month period, these small deficits also show a minor trend toward becoming larger deficits.

Japan's exports depend on global growth as well as competitiveness. But as we have seen with the EMU where its currency has dropped substantially, there is no magic for export growth from currency depreciation in a world of weak growth. A country might be better off being moderately competitive in a fast growing economy than being very competitive in a weak economy.

While Japan is struggling, it is a country with a homogenous culture and a determined people. Japan will get through this period of difficulty. Central banks around the world are doing all they can to stimulate growth. And now that fiscal policy has gotten a bad name, the prospect for a renewed surge from fiscal spending is dead worldwide except for China. I expect the global recovery to continue but slowly. So I expect Japan's exports to regain traction slowly. I do not expect Japan's short-term trends to persist.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.