Global| Aug 19 2019

Global| Aug 19 2019Japan's Trade Deficit Remains as Exports Sag

Summary

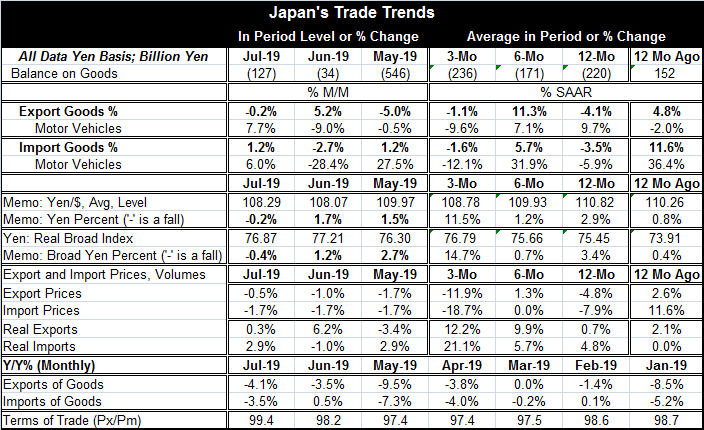

Japan's trade deficit came in at 127 billion yen in July, an enlargement from the 34 billion yen in June. Neither nominal exports nor imports show any clear patterns in the changes over 12 months, six months and three months. Nominal [...]

Japan's trade deficit came in at 127 billion yen in July, an enlargement from the 34 billion yen in June.

Japan's trade deficit came in at 127 billion yen in July, an enlargement from the 34 billion yen in June.

Neither nominal exports nor imports show any clear patterns in the changes over 12 months, six months and three months.

Nominal trendsBut Japanese exports are lower over 12 months and three months. Imports also are lower over 12 months and three months. It's not a steady pace of any sort, but these are some consistencies.

Real trends

Export and import volumes are accelerating from 12-months to six-months to three-months. Real imports are up by 4.8% over 12 months and at a 21.1% rate over three months. Real exports are up at a 12.2% annual rate over three months but up by just under 1% over 12 months. The real trends and nominal trends are nearly opposite over three months, six months and 12 months.

Despite the real export and import revival trends, these are only in place only over about a 12-month period for real flows. Until the last few months, exports and imports in real terms on all horizons were broadly decelerating and weak.

Export and import prices

Export and import prices both show declines over 12 months and sharper declines over three months. And these declines are the reason that nominal flows appear to weak even as real flows continue to advance at a relatively strong pace.

Exchange rates

From 12-months to six-months to three-months, the yen rose vs. the dollar, rising by 2.9% over 12 months and at an 11.5% annual rate over three months. Similarly, the broad yen is up by 3.4% over 12 months and at a 14.7% annual rate over three months. These changes will impact domestic prices and will eventually affect the trajectory of export and import growth. A stronger yen will slow exports and increase imports in addition to the impact of slowing global growth trends.

And yet Japan's two largest trade partners, the U.S. and China are slowing down. China is slowing very rapidly. Japan's real exports don't have any ‘business' being strong even over a short stretch of time based on the growth rates of Japan's main counterparties and on exchange rate shifts. The pop in real exports we observe is probably just a fleeting calculation. The fundamentals will not support such strength on current data at least not for long.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief