Global| Aug 19 2015

Global| Aug 19 2015Japan's Trade Deficit Continues to Be Nettlesome

Summary

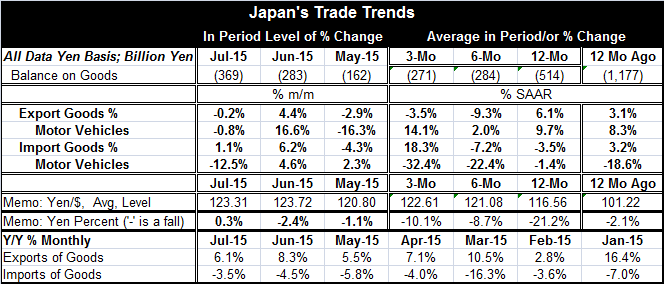

The chart shows that after a period of deficit narrowing, there is a re-imposition of a trend to having trade deficits widen over the last five months. However, a look in the table and at moving averages shows that deficits are lower [...]

The chart shows that after a period of deficit narrowing, there is a re-imposition of a trend to having trade deficits widen over the last five months. However, a look in the table and at moving averages shows that deficits are lower on average over six months compared to 12 months and over three months compared to six months. Data can be confusing. In this case, the chart tells the clearest story since it shows that deficit trends are deteriorating but that deficits still are lower than they had been for 12 months on average. Averages tells us nothing about trends and are really only meaningful if trends are flat. These trends are not flat.

The chart shows that after a period of deficit narrowing, there is a re-imposition of a trend to having trade deficits widen over the last five months. However, a look in the table and at moving averages shows that deficits are lower on average over six months compared to 12 months and over three months compared to six months. Data can be confusing. In this case, the chart tells the clearest story since it shows that deficit trends are deteriorating but that deficits still are lower than they had been for 12 months on average. Averages tells us nothing about trends and are really only meaningful if trends are flat. These trends are not flat.

Japan shows somewhat convoluted trends as well. Exports are stronger than imports over 12 months. On that horizon, export growth is at 6.1% while import growth is at -3.5%. This is why the current deficits are smaller than those of one year ago. But over three months exports are down 3.5% and imports are up at an 18% growth rate. This is why the deficits are starting to increase again over the past few months.

Monthly data on year-over-year percent changes (bottom of the table) show that the export growth has been slowing from 16% in January to 6% in July. Meanwhile, imports on that same basis, are getting less weak and they are net lower year-over-year by 3.5% instead of 7% as they were at the turn of the year.

Japan has just recently restarted the first of its shuttered nuclear reactors. As other reactors restart, Japan's dependence on imported energy will decline and imports will slow and not for the reason of less domestic demand. The slowing will aid Japan's balance of trade and growth.

For now Japan's data are on an upswing. Department store sales rose for the fourth straight month in July at a pace of 3.4%. Japan's all-industry activity index for June made an unexpected gain, rising by 0.3%. But Japan's stock market today has fallen as woes in China are having negative knock-on impacts all over Asia. Japan needs external demand to develop. Instead, China, Japan's most important trade partner, is weak and China's currency is falling. Today Vietnam devalued its currency again. Global markets are tough place to try to gain a foothold for growth. Japan's own currency is sharply lower vs. the dollar over 12 months, moving from 116 yen per dollar on year ago to 123 in July. But most of those competitiveness gains were made as of six months ago. Over the last six months, the yen has fallen by only 2 yen per dollar and the yen actually rose vs. the dollar month-to-month.

Japan is still struggling. Its Q2 GDP report was a disappointment. Monetary stimulus is still in full gear. Yet, because of global weakness and a shrinking domestic population, Japan continues to fall short of its growth targets. Inflation is still hard to start and keep going. The Bank of Japan has pushed out its target date to achieve 2% inflation. June and July have been relatively good months for Japan. It needs to continue to make this sort of progress, but events in Asia are going to make that difficult to do.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief