Global| Jul 03 2006

Global| Jul 03 2006Japan's "TANKAN" Steady at Higher Readings; High Investment Forecast Adds to Expectations of Hike in BoJ Interest Rate

Summary

We've haven't commented on the Bank of Japan's TANKAN report since December, so even though we just talked about Japan's employment data on Friday, this information bears examination promptly as well. Large manufacturing firms, the [...]

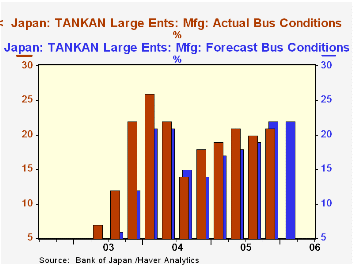

We've haven't commented on the Bank of Japan's TANKAN report since December, so even though we just talked about Japan's employment data on Friday, this information bears examination promptly as well. Large manufacturing firms, the widely followed "headline" segment, saw business conditions in June at +21%, up 1 point from March's 20% reading (a %-balance measure: % favorable less % unfavorable). This result was just below the group's forecast of 22%. They anticipate another 21% in September.

All size firms in all industries also firmed by 1 point from March, from +5% to +6% in June. This performance met their expectations and they look to repeat the +6% in September. All large firms have been holding at 20% with a prospect for 21% in September. Medium-sized companies moved up from +7% in March to +8% in June and hope for +9% in the next period. Small firms continue to struggle, however, with a -2% reading in this survey, a little better than March's -3%, although they look to some deterioration over the summer to -4%.

The large manufacturing companies report that their sales growth this fiscal year continues to come mainly from export customers, with a projection of a 5.2% gain; fiscal 2005 ended with a substantial 11.7% rise, 3.1% more than their last estimate. This year's estimate represents a 6.0 point upward revision of the previous export sales forecast. Domestic sales are not doing as well. The FY2005 outcome was 5.1% growth, even with the previous estimate, but the expectation for this year is just 1.7%, a downward revision of 0.9-point from the last forecast. A breakout by customer is not shown for other firm sizes or industries, but they all expect further gains in total sales this fiscal year and have raised their forecasts after 2005 came in better than forecast.

News reports highlighted forecasts for capital investment this year. Last year's actual spending amounts were in fact somewhat lower than forecast, albeit at still good rates; for example, large manufacturing firms expanded capital spending by 13.9%, but this was 2.6% lower than expected. However, rather than revising down this year's forecasts after that modest shortfall, these firms raised their 2006 plans by 8.2 points to 16.4%. This high number prompted a number of analysts to assert that it would add to the evidence favoring an increase in the BoJ's target overnight call rate at its meeting next week (July 13 & 14). The employment data we reported on Friday and another positive CPI for May (+0.6% year/year) also add to that argument. The call rate, which has been virtually 0% since September 2001, edged upward to 0.02% (2 basis points) last Friday, end-June.

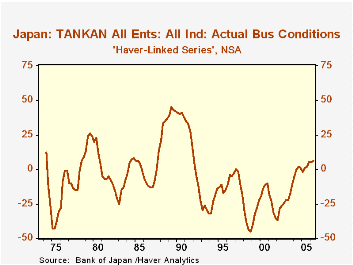

Finally, as we call to your attention frequently, the TANKAN survey was dramatically reorganized two years ago, most significantly changing the very definition of "size" from employee-based to capital-based. Thus, for example, firms counted as "small" before because they employed fewer than 300 people might now be "large" because they have substantial capital; this is particularly true for high-tech companies. Thus, we continue to separate data for the two periods in the survey in our JAPAN database. However, in the Haver database "G10", where we include some customized series that we calculate, we show a long history for "all firms", which would not have been affected by the modified size criterion. That series, seen in the second graph, was +6 this quarter, the highest reading since December 1991, 14-1/2 years ago.

| Business Conditions: % Favorable minus % Unfavorable | June 2006 March 2006 December 2005Sept 2005 | ||||||

|---|---|---|---|---|---|---|---|

| Forecast for Sept | Actual | Forecast for June | Actual | Forecast for Mar | Actual | Forecast for Dec | |

| All Firms | 6 | 6 | 6 | 5 | 4 | 5 | 2 |

| Large Firms* | 21 | 20 | 20 | 20 | 18 | 19 | 17 |

| Manufacturing ("Headline Series") | 22 | 21 | 22 | 20 | 19 | 21 | 18 |

| Nonmanufacturing | 21 | 20 | 19 | 18 | 17 | 17 | 16 |

| Medium-Sized Firms** | 9 | 8 | 8 | 7 | 5 | 5 | 3 |

| Small Firms*** | -4 | -2 | -2 | -3 | -4 | -2 | -5 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief