Global| Oct 01 2009

Global| Oct 01 2009Japan's Tankan Shows Up-Swing... And Less

Summary

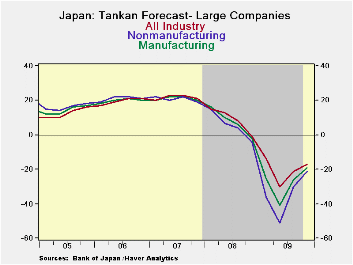

Yes, Japan’s Tankan survey has legs and the rise in the various large company Tankan indices is ongoing. There is somewhat less vigor in the rise of the future improvement expected but it is still advancing at a solid pace and the [...]

Yes, Japan’s Tankan survey has legs and the rise in the

various large company Tankan indices is ongoing. There is somewhat less

vigor in the rise of the future improvement expected but it is still

advancing at a solid pace and the current situation has improved more

rapidly. The fly in the ointment this quarter is that despite ‘improved

confidence’ the plans for capital expenditure have been cut back. In

the end that casts some doubt about the rise in confidence itself.

Firms with profits still under pressure are acting to conserve cash

instead of aggressively re-deploying themselves for growth ahead. That

kind of behavior could help to torpedo recovery even as survey

respondents say that things are getting better.

The table above shows that manufacturing, wholesaling and personal

services are best sectors in terms of the percentile standing of their

respective indices. Even so these sectors are in the bottom 30th

percentile of their respective ranges or lower. Non MFG as a whole is

in the bottom 13 percentile of its range. Manufacturing’s outlook, at a

raw reading of -21, is in the 41st percentile of its range. That is

somewhat better, than the current assessment but still far from good.

Medium sized firms assess their MFG index as in the 23rd percentile of

its ranges for small enterprises it is much worse as they stand in the

bottom 7th percentile of their range. The nonMFG percentiles for the

medium and small enterprises are comparable to the Tankan Large Company

readings for Non MFG – very weak.

Yes Japan has made progress. But the current state of business is still

poor even though it has improved. While the expected improvement is at

a slightly better level than the assessment of current conditions,

firms continue to react to the recession instead of planning ahead for

recovery. As a result, one of the great forces of recovery has yet to

be unleashed- optimism. Japan’s recovery remains cautiously guarded and

in the end that will be a drag on its momentum. Until firms see the

need to invest for the future and as long as they cut and hack at

existing spending plans the look will remain touch and go.

| Tankan Results Large Enterprises | |||||||

|---|---|---|---|---|---|---|---|

| Readings | Averages | PERCENTILES | |||||

| Q3-09 | Q2-09 | Q1-09 | Q4-08 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG | -33.0 | -48.0 | -58.0 | -24.0 | -40.5 | 5.3 | 29.8% |

| NonMFG | -24.0 | -29.0 | -31.0 | -9.0 | -26.5 | 7.8 | 13.2% |

| Total Industry | -28.0 | -39.0 | -45.0 | -16.0 | -33.5 | 6.5 | 25.0% |

| Construction | -23.0 | -29.0 | -27.0 | -10.0 | -26.0 | -5.9 | 18.2% |

| Real Estate | -11.0 | -24.0 | -21.0 | -7.0 | -17.5 | 24.3 | 16.9% |

| Wholesale | -29.0 | -41.0 | -44.0 | -7.0 | -35.0 | 8.2 | 22.1% |

| Retail | -32.0 | -39.0 | -42.0 | -18.0 | -35.5 | -0.9 | 17.2% |

| Transportation | -35.0 | -43.0 | -46.0 | -7.0 | -39.0 | 5.8 | 15.7% |

| Services 4 Biz | -22.0 | -30.0 | -21.0 | -1.0 | -26.0 | 15.2 | 11.9% |

| Personal Serv | -4.0 | -11.0 | -9.0 | -11.0 | -7.5 | 7.1 | 23.3% |

| Restaurants & Hotels | -50.0 | -46.0 | -45.0 | -32.0 | -48.0 | -3.3 | 0.0% |

| Forecast | |||||||

| Q4-09 | Q3-09 | Q2-09 | Q1-09 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG-OtLk | -21.0 | -30.0 | -51.0 | -36.0 | -34.5 | 5.8 | 41.1% |

| NonMFG -Otlk | -17.0 | -21.0 | -30.0 | -14.0 | -20.5 | 8.4 | 24.5% |

| All Industry-Otlk | -19.0 | -26.0 | -41.0 | -25.0 | -27.8 | 7.0 | 34.9% |

| Tankan Results Medium Enterprises | |||||||

| Q3-09 | Q2-09 | Q1-09 | 1-Y Avg | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG | -40.0 | -55.0 | -57.0 | -44.0 | -44.0 | -7.8 | 23.0% |

| NonMFG | -30.0 | -36.0 | -37.0 | -31.0 | -31.0 | -8.9 | 15.6% |

| Forecast | |||||||

| Q4-09 | Q3-09 | Q2-09 | Q1-09 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG-OtLk | -35.0 | -46.0 | -61.0 | -45.0 | -46.8 | -9.1 | 34.7% |

| NonMFG -Otlk | -28.0 | -32.0 | -45.0 | -32.0 | -34.3 | -10.5 | 32.7% |

| All Industry-Otlk | -31.0 | -39.0 | -51.0 | -38.0 | -39.8 | -10.1 | 32.8% |

| Tankan Results Small Enterprises | |||||||

| Q4-09 | Q3-09 | Q2-09 | Q1-09 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG | -52.0 | -57.0 | -57.0 | -54.5 | -54.5 | -15.0 | 7.5% |

| NonMFG | -39.0 | -44.0 | -42.0 | -41.5 | -41.5 | -20.2 | 13.2% |

| Total Industry | -39.0 | -44.0 | -42.0 | -41.5 | -41.5 | -20.2 | 12.2% |

| Forecast | |||||||

| Q4-09 | Q3-09 | Q2-09 | Q1-09 | 1-Y Avg | Since Q3'03 | Since Q1'04 | |

| MFG-OtLk | -44.0 | -53.0 | -63.0 | -48.0 | -52.0 | -16.2 | 26.4% |

| NonMFG -Otlk | -40.0 | -45.0 | -52.0 | -42.0 | -44.8 | -23.9 | 27.3% |

| All Industry-Otlk | -41.0 | -48.0 | -56.0 | -44.0 | -47.3 | -21.1 | 27.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief