Global| Apr 01 2015

Global| Apr 01 2015Japan's Tankan Results Show Little Progress in Q1 2015

Summary

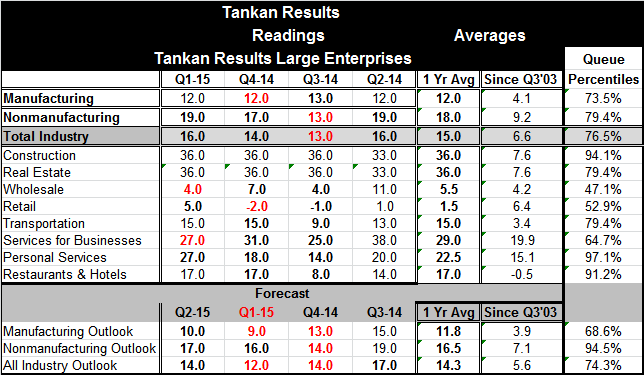

Japan's Q1 2015 Tankan report shows little progress for the overall economy. The al industry reading nudges up to 16 in Q1 2015 from 14 in Q4 2014. The all industry outlook also edges up to 14 from 12 in Q4 2014. The closely-watched [...]

Japan's Q1 2015 Tankan report shows little progress for the overall economy. The al industry reading nudges up to 16 in Q1 2015 from 14 in Q4 2014. The all industry outlook also edges up to 14 from 12 in Q4 2014. The closely-watched manufacturing sector index made no gain in Q1 and its outlook shows only the most minimal progress is expected.

Japan's Q1 2015 Tankan report shows little progress for the overall economy. The al industry reading nudges up to 16 in Q1 2015 from 14 in Q4 2014. The all industry outlook also edges up to 14 from 12 in Q4 2014. The closely-watched manufacturing sector index made no gain in Q1 and its outlook shows only the most minimal progress is expected.

We calculate queue percentiles which place each of these readings in their historic queue of data with the relative position expressed as a percentile standing. The total industrial index stands in the 76.5 percentile of its historic range just inside the top historic quartile, a firm reading. Nonmanufacturing has a slightly higher standing than manufacturing. The nonmanufacturing index is up on the quarter, but the closely watched manufacturing gauge is flat quarter-to-quarter.

As for other sectors and sub-sectors, construction, personal services, and restaurants & hotels each have top 10 percentile standings. The weak sectors are wholesaling, at its 47th percentile standing, retailing, at its 52nd percentile standing, and services for businesses, at its 64th percentile.

Most disappointing are the outlook metrics for this quarter. As the chart shows, these indices had been moving higher in 2014 but have since hit a rough spot and declined from their respective local peaks and are now struggling to regain momentum. All are still off their best values for 2014. The manufacturing outlook is very modest with its outlook index in only its 68th queue percentile. That means it has been higher 32% of the time. The nonmanufacturing sector index is much more robust with a 94th percentile standing. It has been better only 6% of the time. But manufacturing weighs heavily in the overall index. As a result, the all industry index sits only in its 74th percentile, just outside the top quartile of its historic queue of values. At that position, it is not especially strong but not weak either.

On balance, Japan is not showing any follow through to the boost the economy experienced last year. The expectation impact of QE is fading and even the weakening of the exchange rate is not helping because so much production has been off-shored out of Japan. In fact, some complaints have been made that the weaker yen only increases the prices of imports and we do see that the retail sector is lagging substantially.

Japan has few options left. It has already postponed the second phase of its planned consumption tax hike after the first phase hit the economy so hard and that weakness seems to have lingered. More fiscal policy is not an option. Monetary policy is already very stimulative and the usual impact of QE on the exchange rate is not helping much. Japan, more than any other countries, seems to have its fate depending importantly on some pick up in the global economy. Domestic policy has few levers left to pull. Fortunately, the Tankan report is still positive. It's just that it is pointing to continued weak growth, showing tempered momentum.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.