Global| Apr 03 2017

Global| Apr 03 2017Japan's Tankan Report Picks Up as the Global Rebound Slows

Summary

Japan's current Tankan assessment shows pick-up The bellwether in Japan's Tankan report is the large company response particularly for manufacturing concerns. In Q1 2017 and in the outlook for Q2, manufacturers form a strong part of [...]

Japan's current Tankan assessment shows pick-up

Japan's current Tankan assessment shows pick-up

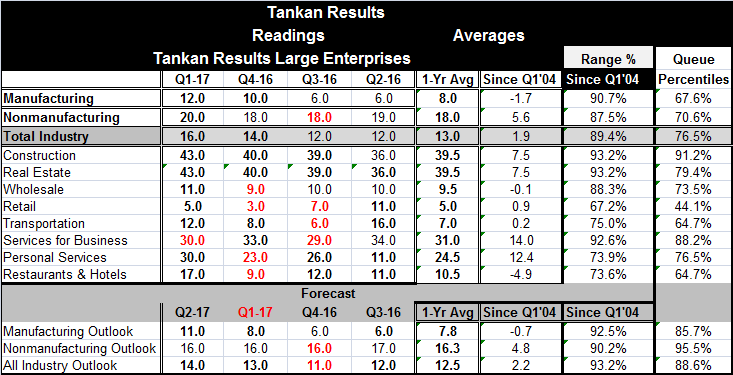

The bellwether in Japan's Tankan report is the large company response particularly for manufacturing concerns. In Q1 2017 and in the outlook for Q2, manufacturers form a strong part of the report. The manufacturing firms logged an increase in their Q1 assessment to 12 from 10. Nonmanufacturers also logged an increases to 20 from 18. The manufacturers' readings rank in the top 67% of their historic queue of data while for nonmanufacturers the ranking is in its 70th percentile. However, the joint strength of the two sectors boosts the overall large company index to its 76th percentile standing, better only one-quarter of the time.

Japan's outlook improves

The outlook portion of the survey for Q2 2017 finds the manufacturers' reading up to 11 for Q2 from 8 in Q1. The nonmanufacturers outlook is flat at 16 for the last three quarters in a row. Still, the nonmanufacturers' index has a 95th percentile standing; it has been higher only about 5% of the time. Despite its jump in Q2, the manufacturers' index has a lower 85th percentile standing. Manufacturing has been lagging in Japan. The all-industry outlook is one-point higher in Q2 than in Q1 and has an 88th percentile standing.

The global manufacturing scene

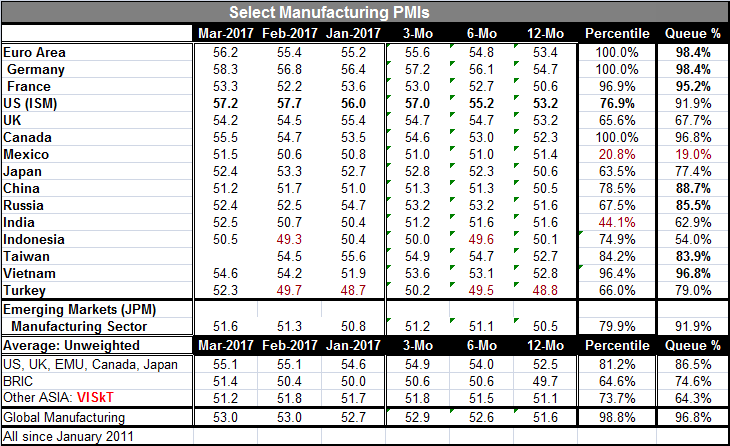

However PMI data also were released on the day and Japan's manufacturing PMI reading slipped back to 52.4 in March from 53.3 in February. The U.S. and China saw their respective manufacturing PMIs also slip back on the month. These are Japan's two largest trade partners. The global manufacturing PMI data were more mixed than strong this month and emerging markets were on balance still improving on mixed internal trends. For the group, the U.S., UK, Canada, EMU and Japan, the manufacturing PMI was unchanged in March. For BRIC countries, there is an improvement. For other Asian developing economies, excluding China, there was a modest setback. The global manufacturing gauge is assessed as unchanged based on these early global returns.

Manufacturing trends

All reporting countries except Turkey, Mexico and South Korea have manufacturing gains over 12 months. Among the 13 countries reporting year-on-year gains, the median rise over 12 months is 3.6 points, a sizeable gain. The strength is centered more in the West with Germany making the largest 12-month gain at 7.6 points, followed by the U.S. at 5.5 points and Russia at 4.1 points. The weakest gainers (and recall that two of the three declining indexes are for Asian economies) are India at a 12-month gain of just 0.1 and China at a 12-month gain of just 1.5. After being a driver of activity for so long, Asia is still struggling. Japan's manufacturing sector is up by a solid 3.3 points over 12 months, but that still lags the median gain slightly

European unemployment rates- some perspective

European unemployment rates for February also were released today and unemployment rates fell in only five on 13 reporting EMU countries plus the U.K. (if we include the U.K. and Greece with two-month lagging unemployment rates). Compare this lower breadth with the falling unemployment rates in 10 countries over three months and six month and in rates dropping in 12 of 13 of them over 12 months. In Europe, 6 of 13 countries have unemployment rate levels below their medians calculated since 1991. And five members still have unemployment rates in the top 31st percentile of their historic queues of data. Five of 13 countries have unemployment rates that are still in double digits. This is not the spot where anyone wants upward momentum to slow. Nor is it a place to choose to make a stand to fight expected inflation that we 'fear' with no sign of it. The lack of inflation, plus weakness in oil prices, and slowing in unemployment rate reduction trends, simply are red flags to the kinds of regime-change policy changes central banks in Europe and the U.S. have been considering.

Monetary policies in need of a rethink

On balance, the global environment is holding its gains this month with shuffling around among different groups but with uptrends largely intact. Monetary authorities have fiddled with the idea of scaling back. It is not so clear that momentum is strongly supporting that action as manufacturing momentum has slowed this month after two strong monthly gains. For inflation-targeting central banks, the lingering weakness in oil prices is no longer helping them to achieve their 'targets' artificially. And with inflation lackluster and below target, neither momentum, nor growth, nor the level of global unemployment rates, support a central bank backing off the gas at this point. And tapping the brakes hardly seems productive as the Fed is doing in the U.S. and there even with the threat of engaging its ABS system. Such dramatic braking (rate hiking) proposals have come out of the blue in the U.S. and would say they have been encourage more by OPEC's past success in getting oil prices higher than in any real inflation pickup. While growth has showed some upside, there is nothing there that needs to be resisted artificially by central banks.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief