Global| Apr 01 2014

Global| Apr 01 2014Japan's Tankan Eases as Tax Anxiety Rises (Not an April Fools Joke)

Summary

Japan's much awaited Tankan report for large enterprises showed an increase for manufacturing firms in the first quarter to 17 from 16 in the fourth quarter. But nonmanufacturing firms saw an increase to 24 from 20 in the fourth [...]

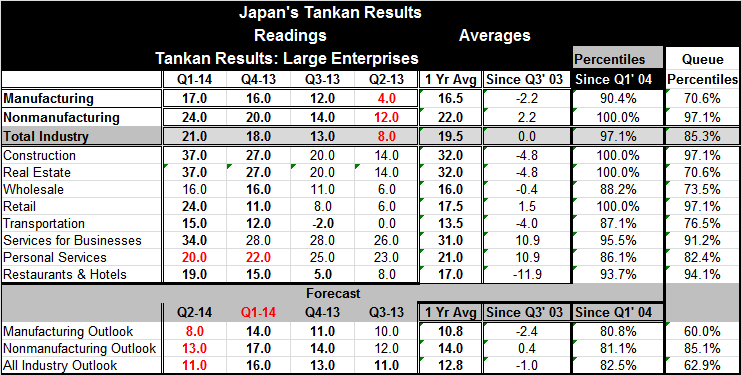

Japan's much awaited Tankan report for large enterprises showed an increase for manufacturing firms in the first quarter to 17 from 16 in the fourth quarter. But nonmanufacturing firms saw an increase to 24 from 20 in the fourth quarter. The total industry gauge rose to 21 from 18. Despite the advance, the quarterly increases were less than expected and it's widely believed that the culprit is the nationwide sales tax increase that is taking effect on April 1 this year (today).

Japan's much awaited Tankan report for large enterprises showed an increase for manufacturing firms in the first quarter to 17 from 16 in the fourth quarter. But nonmanufacturing firms saw an increase to 24 from 20 in the fourth quarter. The total industry gauge rose to 21 from 18. Despite the advance, the quarterly increases were less than expected and it's widely believed that the culprit is the nationwide sales tax increase that is taking effect on April 1 this year (today).

In 1997, Japan also had raised its consumption tax, trying to battle its problem with large government debt. At that time in the wake of the tax hike, Japan's economy slipped into recession and banking sector problems emerged. It's not surprising that firms are wary of what will happen this time: once burned, twice shy.

In this episode, Japan's economy is growing. Japan appears to have just shaken off the yoke of deflation. However, even that conclusion is tentative; Japan's growth is not particularly strong. Its export-led growth has not been able to fire up the economy because of weakness in China, its main trade partner and sluggishness in the rest of the world. In such a circumstance, it is not surprising that concerns turned to something that can harm domestic demand, a consumption tax hike. Moreover, there is some evidence that spending patterns may have been accelerated in Q1 2014 to squeeze purchases in ahead of the tax hike. If so, the impact of the hike in Q2 will appear to be even larger though this lead-effect.

The large company results of the Tankan show increases month-to-month and all sectors except personal services. That sector has shown some backtracking for two consecutive quarters. The manufacturing outlook has slipped sharply from a reading of 14 in Q1 2014 to a reading of 8 for Q2 2014. The nonmanufacturing outlook also has slipped from a reading of 17 in Q1 to a reading of 13 in Q2. The manufacturing outlook is still above its four-quarter average while the nonmanufacturing outlook is slightly below its four-quarter average.

Despite the slippage in the outlook, the levels of the indices are still not sharply lower. The drop in manufacturing from 14 to 8 is a relatively sharp month-to-month drop, but that sector had made a three-point increase in the first quarter from 11 to 14 consequently can view this is an unwinding of that increase. In the case of nonmanufacturing, the drop from 17 to 13 is also substantial but the fourth quarter level was only a reading of 14 so that the second quarter of 2014 shows an outlook index that is only slightly below the fourth quarter of 2013.

On balance, I don't think that there is a great draconian downshift in sentiment, but there does appear to be caution and concern on the parts of various firms and a clear downshifting of expectations. Maybe also there is simply wariness.

Medium-sized Japanese firms have their own Tankan readings that are not as closely watched. But they showed sharp increases in the first quarter for both manufacturing and nonmanufacturing activities. The outlook from the sector for manufacturing is flat in the second quarter and for nonmanufacturing there's a considerable downshift. With the downshift for nonmanufacturing, the level for the outlook index is brought down to just two points below the fourth-quarter level for the index.

Small enterprises also contribute to the survey and their manufacturing and nonmanufacturing activity responses for the first quarter were up significantly. Like the larger firms, their outlooks show a loss in confidence, but also outright negative readings for the second quarter. The level of their outlook readings for manufacturing and nonmanufacturing is back to fourth-quarter or third-quarter levels.

Japan's economy had become optimistic upon the implementation of Abe-nomics and its early success. But since its early implementation, there hasn't been the same degree of follow-through although deflation appears to be dissipating. There are lingering concerns about growth in the Japanese economy and these now are becoming more extended as a consumption tax kicks in on April 1.

It is important to note two different things. First, the indices of activity for the first quarter showed improvement. The economy still is carrying momentum up to the brink of the time that the sales tax is being implemented. Secondly, the outlook is being cut back but after substantial elevation in the previous quarter. While the setback for the second quarter outlook generally more than offsets the increase in the outlook for the first quarter, Japan's large enterprises still have a positive number for the outlook in Q2 2014.

The question will be how the Japanese people respond to the consumption tax hike. The question also will be how the global economy responds in Q2 2014 because if Japan is able to increase its exports due to improved global conditions, the bite of the tax hike will not be as severe. This survey like all surveys is subject to the uncertainty of the future. Businesses are somewhat wary the future and that is having some negative impact on their willingness to invest. But if the future turns out to be better than they think, so will their economic responses to it.

We can evaluate the levels of the indices offered in the Tankan this quarter. The total industry large enterprise Tankan index sits in the 85th percentile of its queue, implying that it is higher only 15% of the time. Nonmanufacturing is exceptionally strong in the 97th percentile of its queue; it is higher only 3% of the time. Manufacturing is in the 70th percentile of its historic queue, higher about 30% of the time.

Across sectors, some of the strongest sectors by this queue percentile basis are construction, retailing and services for businesses. Retailing has been fairly strong coming into the tax hike. Among some of the weaker sectors are real estate which is still in the 70th percentile of its historic queue and transportation still in the 76th percentile of its historic queue and wholesaling in the 73rd percentile of its historic queue. We don't find exceptional weakness, just some lagging behavior.

Turning to the outlook indices, the level of the manufacturing outlook sits only in the 60th percentile of its historic queue. For nonmanufacturing the outlook is in the 85th percentile of its historic queue. For all of industry the outlook is in the 62nd percentile of its historic queue. It's in these rankings that we see the somberness of the interpretation of the Tankan. The question is whether we should place an exceptional amount of weight on the outlook contributions from the Tankan or whether we should give a little bit more weight to the momentum expressed in current conditions. Outlooks are by nature speculative.

There's no doubt that the sales tax will deal some kind of negative shock to the economy. The question is how big that shock will be. Is it reasonable that it will take industry performance that now is in the 85th percentile and knock it down to the 62nd percentile as the outlook suggests? Maybe... Right now we see a lack of confidence in Japan and fear that 1997 could repeat itself more that the substance of the current threat.

The problems that the 1997 tax hike created are well known. And the knowledge that there is a tax hike coming that will impart a negative impulse to the economy is known by all. It's not surprising that these factors cause a negative tilt to industry survey responses. The question is whether the tilt of the negative response has gone too far. Is Japan in better shape now than it was in 1997? Is Japan better positioned in the global trading markets? Is global growth picking up? These are questions that will be answered in coming months and quarters.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief