Global| Oct 15 2020

Global| Oct 15 2020Japan's Surveys: Service Sector Recovery Is Much Less Than Complete

Summary

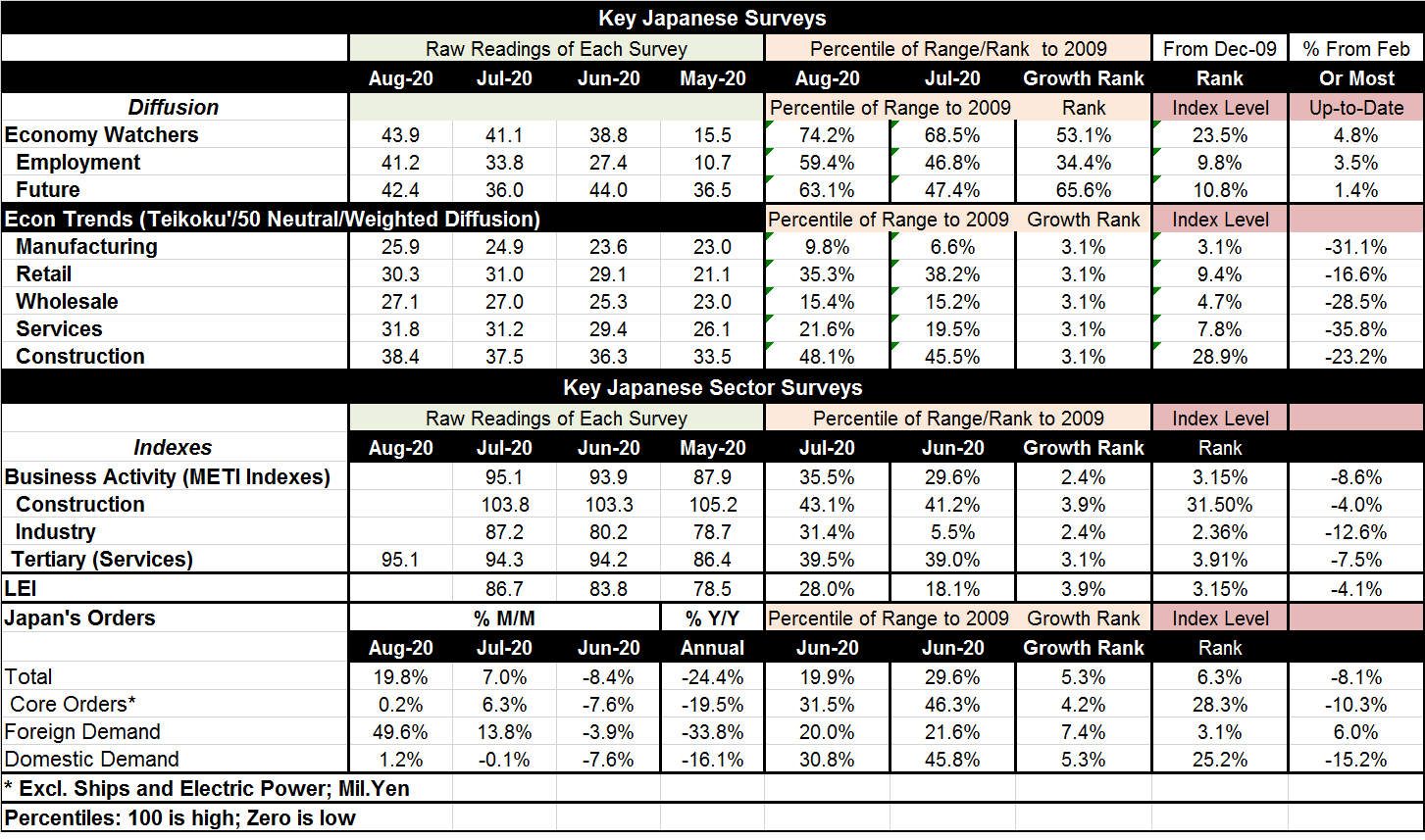

Japan's service sector index (tertiary sector from METI) is the most recent reading on Japan's economy. That index rose to 95.1 in August from 94.3 in July. However, it has a 3.1 percentile standing based on its y/y growth rate and [...]

Japan's service sector index (tertiary sector from METI) is the most recent reading on Japan's economy. That index rose to 95.1 in August from 94.3 in July. However, it has a 3.1 percentile standing based on its y/y growth rate and the index level has a 3.9 percentile standing (comparing its current performance to performance since 1990). Compared to its January 2020 level, the index is still not recovered having advanced to a level that is 7.5% below its January level (far right hand column of data).

Japan's service sector index (tertiary sector from METI) is the most recent reading on Japan's economy. That index rose to 95.1 in August from 94.3 in July. However, it has a 3.1 percentile standing based on its y/y growth rate and the index level has a 3.9 percentile standing (comparing its current performance to performance since 1990). Compared to its January 2020 level, the index is still not recovered having advanced to a level that is 7.5% below its January level (far right hand column of data).

Of the 19 survey indicators in the table, only four are above their respective January levels. Three of those are from the economy watchers index. The final one of the four is from the orders survey representing foreign demand. Apart from the four positive observations, the average across the rest is a shortfall of 14.7% compared to January 2020.

According to most measures, Japan has not recovered back to its pre-covid-19 levels of activity on most of the various measures. The economy watchers index, that is a diffusion index, is the main exception. Diffusion is a measure of breadth rather than strength. However, all the gauges in this table are some sort of diffusion index except the orders data and the LEI which is a weighted index of components. However, several columns report different kinds of assessments such as the growth and level ranking for the various indexes. Assessed over a long period of time, back to 2009, the growth rank of these indexes averages 13.5% and the average percentile queue standing of the gauge levels is 11.5%. Both of these are exceptionally low readings.

Not only has Japan not made recovery from January and the period when the coronavirus struck, but its current gauge assessments are extremely low when a much longer comparisons are made.

Japan is continuing to struggle. The Bank of Japan has not been able to win its battle to hit its inflation target of 2%, but it has been able to expunge deflation. While one of the gauges shows that foreign demand is back above its January 2020 level, that achievement is not saying much since the overall ranking of that concept is only in the 3% to 7% range of queue standings depending on the measure used to assess it. While Japan's virus outbreak is not as severe as in other countries, Japan is a country of high population density and it tends to take even small backtrackings in virus progress as something serious to address.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief