Global| Mar 13 2017

Global| Mar 13 2017Japan's Service Sector Index Comes Up Flat As Core Orders Fall

Summary

Japan is hardly firing on all cylinders these days. Its overall business activity index for January is still not finalized since the construction sector has not reported for January. However, I indicate in the table that the overall [...]

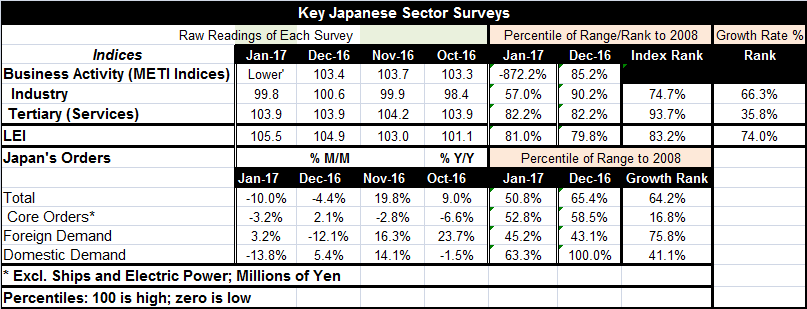

Japan is hardly firing on all cylinders these days. Its overall business activity index for January is still not finalized since the construction sector has not reported for January. However, I indicate in the table that the overall index should be lower since the construction sector is small, the industrial sector is lower, and the services sector (tertiary sector) is unchanged in January. The mining/manufacturing index and the service sector index are plotted on the chart. Services continue to plod while the industrial sector is still pulling back from a one-month spike.

Japan is hardly firing on all cylinders these days. Its overall business activity index for January is still not finalized since the construction sector has not reported for January. However, I indicate in the table that the overall index should be lower since the construction sector is small, the industrial sector is lower, and the services sector (tertiary sector) is unchanged in January. The mining/manufacturing index and the service sector index are plotted on the chart. Services continue to plod while the industrial sector is still pulling back from a one-month spike.

In terms of the height of the raw sector indices, the industrial index (mining and manufacturing) has been higher about 25% of the time (74.7 percentile standing). The services sector has been stronger only about 6% of the time (93.7 percentile standing). But as you can see in the chart, services are not very strong even in index level terms by the standards of the recent few years (the table ranking is over the last eight years, and that is a much easier comparison). However, ranked in terms of the one-year growth rate, the industrial sector index dropped to its 66th percentile (near the border of its top third of growth rates), while the services sector dropped to its 35.8 percentile (just above the bottom one-third of its historic queue of growth rates). Neither is very impressive, but the services reading is also a bit worrisome.

The leading economic index, which was recently revised, shows its growth as at its 83rd percentile in terms of its index standing and at its 74th percentile in terms of its year-on-year growth rate. The index level reading is relatively good, but unimpressive since it is an index level on an LEI index whose components constantly grow. The ranking based on the growth rate of that index is more meaningful and, of course, more moderate.

Japan's machinery orders in January fell for the second month in a row. Core orders, the preferred measure, also fell in January. Core orders, the more stable series, are lower by 6.6% year-on-year and the ranking of that growth rate is only in its 16th percentile historically which is quite poor.

Japan did post a rise in its PPI in February, but it is hard to say that it is out from under the shadow of deflation. Its growth metrics are tepid and their rankings are basically tepid or, where they are firmer, it is only in comparison with growth during a weak period. The inflation measures, to the extent that they show any firmness (such as today's 1% year-on-year PPI gain), are all on the back of higher oil prices, not real progress in moving overall prices higher. Japan is still struggling.

But Europe has been looking a bit better. The Fed is preparing to hike rates this week. A G20 meeting is on tap and global policy seems to be ready to move on to a new phase even if everyone is not on board the same growth path. There is still a lack of substance to the feel-good interpretation of growth. In the U.S., the Atlanta Fed GDP now-cast puts Q1 growth at only 1.2%, hardly robust or at an inflation boosting pace to Keynesians. Who would have thought that the Fed would be hiking rates with a 1.2% growth rate in prospect? Most key measures of inflation, in fact, do not show much acceleration despite gains in oil prices. In Europe, surveys like the Markit PMIs show firmness, but the traditional economic reports have yet to turn the corner. There is a sense that things will fall into place, but we have been disappointed while trying to turn this corner before. It is a good time to wait and see and risky time to throw your lot in with the optimists. They may be right, but the growth step up is not yet a done-deal.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief