Global| Mar 15 2021

Global| Mar 15 2021Japan's Service Sector Contracts for the Third Month in a Row and Japan Orders Fall in January

Summary

Compare current activity to one year ago Japan continues to have a slow rollout out from under the effects of the coronavirus. The far-right hand column of the table looks at the percentage change in each measure in the table on its [...]

Compare current activity to one year ago

Compare current activity to one year ago

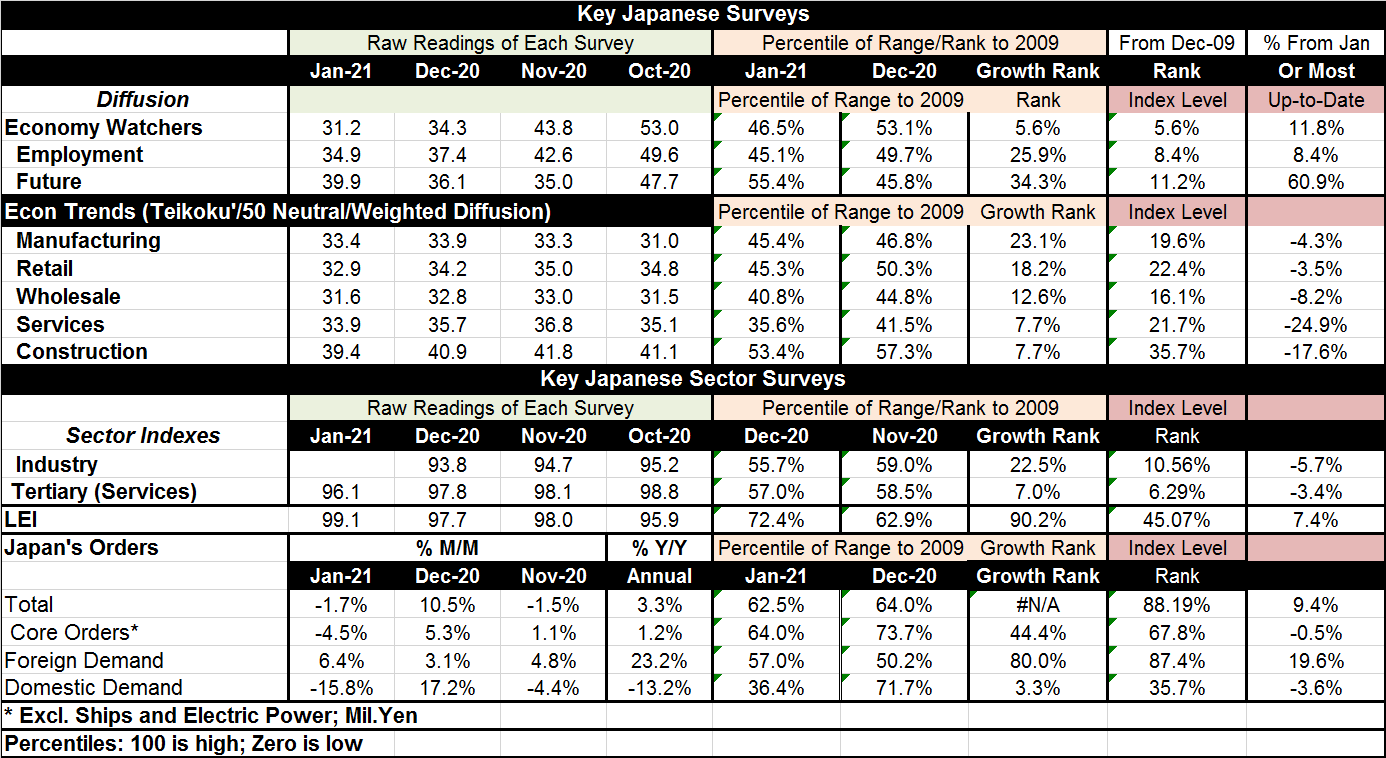

Japan continues to have a slow rollout out from under the effects of the coronavirus. The far-right hand column of the table looks at the percentage change in each measure in the table on its most recent data compared to January 2021. The economy watchers readings all are higher year-on-year with the future index making very strong gains. The Markit sector surveys show stronger manufacturing but still weaker services compared to a year ago. The Teikoku industry readings show shortfalls for all the industries compared to January of last year. The METI sector indexes show weaker industrial sector and weaker services as well. The LEI shows substantial improvement. Japan's orders are mixed with total orders higher and core orders lower; foreign demand is significantly higher but domestic demand is lower on balance.

Survey consistencies

When pooled together, surveys often show some conflicting signals. But in this case, there are a lot of similarities across these surveys. One finding is that the service sector is weaker and is still floundering. Another is that forward-looking measures are generally much better, but nowhere is the future index bearing a strong ranking. Japan's manufacturing sector is better than it was in January a year ago in only one survey. For the most part Japan's manufacturing or industry sector is doing worse than most developed countries (in PMI data). We can get a glimpse of that here in the orders response that shows substantial strength in foreign demand against net weaker conditions in domestic demand. Whoever performed the survey does not matter; Japan's service sector carries weak rankings (ranking data are the second from the end column).

Growth rankings are weak

The third column from the right also ranks data, but it does so based on year-over-year growth comparisons. On that basis, only manufacturing, the LEI and foreign demand (also total orders but only because of foreign demand) have rankings above their respective medians (rankings above the 50% mark).

The virus

Japan continues to have trouble with the virus. And while its domestic infection rate is lower than in many other countries, Japan is worried about its population density and Japan may also benefit on this measure from a low incidence of reported infections because testing is not very widespread. Japan is also trying to clear up its situation on infections as it plans to host the Olympics… one year late.

Momentum on a shorter timeline…still challenged

The economy watchers index has lost substantial momentum since October of last year each for its three readings. The Markit gauge shows industry has been fluctuating. It is higher than its level in October but is lower than it was in December. The service sector reading is on its low reading since October. The Teikoku industry readings are mostly weaker since October with manufacturing as an exception and wholesaling as a one-tick exception. The METI sector indexes are both weaker since October. The LEI is an exception and is up solidly since October. Orders for Japan are higher than their October levels (not seen in table) for three of the four components; domestic demand is the exception and is weaker compared to its October level.

Summing up

Right now Japan is being helped forward by international growth. U.S. stimulus spending should also help Japan exports in the months ahead. Currently Japan's largest trading partner, China, is showing a revival that should help pull Japan along. But Japan's domestic demand and domestic service sector are wavering and weak. The vaccination process has been going slow in Japan and that is hindering the revival of the service sector and of domestic demand in general. If Japan is able to step up the pace of inoculations, its situation should improve. But the coronavirus crisis has been very hard on the elderly and Japan has an extremely large elderly population and that may account for why Japan has been so cautious and is moving so slowly.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief