Global| Jan 23 2017

Global| Jan 23 2017Japan's Sector Survey Crawls Higher

Summary

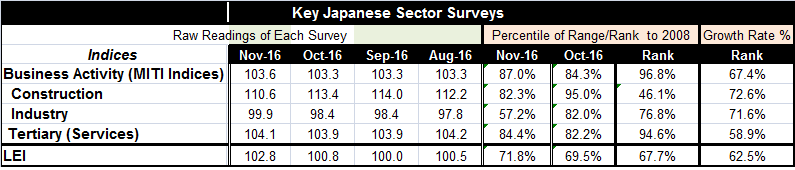

Japan's sector surveys were only able to crawl higher in November as the industrial and services gauges rose while construction slipped to hold the overall advance back. The all-industry index rose to 103.6 in November from 103.3 in [...]

Japan's sector surveys were only able to crawl higher in November as the industrial and services gauges rose while construction slipped to hold the overall advance back. The all-industry index rose to 103.6 in November from 103.3 in October; in October it was flat month-to-month.

Japan's sector surveys were only able to crawl higher in November as the industrial and services gauges rose while construction slipped to hold the overall advance back. The all-industry index rose to 103.6 in November from 103.3 in October; in October it was flat month-to-month.

Sector growth

The all-industry index rose by 1.4% year-over-year as the industrialized sector advanced by 2.9% and construction advanced by 2.8%. The service sector index is up by just 0.9% over the past year.

Sector rankings on growth

The ranking of the growth rates since 2008 (table: far aright-hand column) shows the relative best performance has been from construction whose year-on-year growth rate rank is in its 72.6 percentile, a firm but moderate reading (growth is higher about 27% of the time). Industry is right behind it with a 71.6 percentile standing. The services sector lags with a 58.9 percentile standing.

Levels of output lag past peaks

However, if we re-rank the indices according to their respective levels, the relative best-off sector is services at a 94th percentile standing. Services may not grow strongly, but it does grow more relentlessly. Despite its growth over the past year, the construction index stands only in its 46th percentile, below its median. The industrial gauge is more balanced, standing at its 76th percentile. The sector indices - taken altogether- stand in the 96.8 percentile of their historic queue of values in terms of the level of the all-industry index. This demonstrates that activity is still below its past peak.

Japan's LEI advances

Japan's leading economic index, also released today, was revised slightly higher. The LEI moved up to 102.8 in November from 100.8 in October. It is higher year-on-year by 1.2% and that growth rate has a 62.5 percentile standing in its historic queue of year-on-year rates of growth. That is a middling result.

Japan's government assessment

This month the government did not alter its assessment of the economy's performance, calling the expansion moderate. The MITI sector indices and the LEI seem to confirm that assessment. A separate and slightly more timely set of industry gauges from Teikoku also shows moderate expansion underway as does the economy watchers index, a service sector-focused index.

The government assessment did note that investment may have lost some momentum but that consumption was continuing to advance. Investment is a more or less a global problem with economic slack still so widespread.

Oil

One place that investment is taking place again is in the U.S. in the oil sector now that prices are higher. This confronts OPEC with the 'dark side' of its policies. That is that drilling in the U.S. has picked up and is beginning to have an appreciable impact on global oil supplies. Oil prices were lower today on the observation that U.S. oil production was beginning to swamp some of the output cuts made by OPEC. The oil market continues to be in delicate balance. While there are still different grades, densities sweetness and sourness of crude, after allowing for all that oil is oil. And the short-term demand for oil is inelastic and that keeps prices volatile. OPEC continues pay this dangerous game trying to fine tune oil prices and raise them up from their morbidity. Oil is not simply a one-way way bet in the short and medium term. OPEC has a tiger by the tail.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief