Global| Oct 21 2013

Global| Oct 21 2013Japan's Sector Indices Edge up in August

Summary

For only the second month in a row, Japan's all three METI sector indices are rising together year-over-year. The construction index is up 14% year-over-year and its rise has been gaining momentum until this month when the year-over- [...]

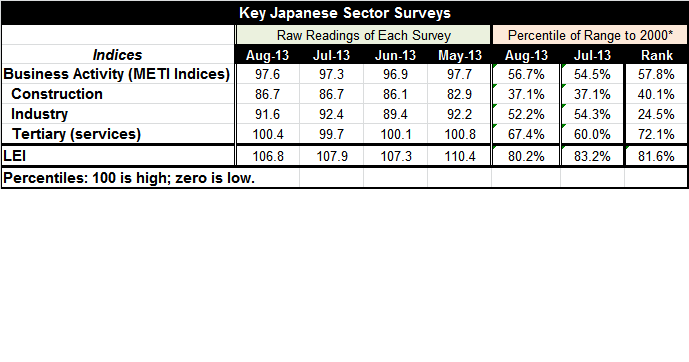

For only the second month in a row, Japan's all three METI sector indices are rising together year-over-year. The construction index is up 14% year-over-year and its rise has been gaining momentum until this month when the year-over-year growth rate backed off to 13.0% from 13.2% in July. The services sector, the least of volatile of sectors, shows an increase of 1.3% year-over-year, its strongest gain since May of this year. Manufacturing (industry) is up by 1% year-over-year, only its second consecutive year-over-year gain.

For only the second month in a row, Japan's all three METI sector indices are rising together year-over-year. The construction index is up 14% year-over-year and its rise has been gaining momentum until this month when the year-over-year growth rate backed off to 13.0% from 13.2% in July. The services sector, the least of volatile of sectors, shows an increase of 1.3% year-over-year, its strongest gain since May of this year. Manufacturing (industry) is up by 1% year-over-year, only its second consecutive year-over-year gain.

Month-to-month trends show that construction was flat this month as industry back-tracked to 91.6 from 92.4. The month's overall activity gain was wholly on the back of the services sector where the index rose from 99.7 to 100.4.

To put the indices is some historic context the activity index is in the 57.8th percentile of its historic queue, above the mid-point which falls at the 50th percentile. Construction, despite its strong momentum, is still at a weak level. Its index stands at the 40.1th percentile of its historic queue. Industry is lagging more than construction. It stands at the 24.5th percentile of its historic queue. It is weaker than this only about 25% of the time - a poor standing. The services sector is the most robust, at a 72.1 percentile standing of its historic queue. This sector is stronger only 28% of the time. It is the main reason that the overall business activity index is above its 50th percentile.

Japan's economy is on the upswing. This month the Bank of Japan upgraded its assessment of all nine regions. This is the first hike in its regional assessment since April of this year. Four regions noted expanding production, four others noted accelerating production and one cited ongoing production at a high level.

On balance Japan is still making progress. But as the sector rankings show, it still has long way to go in order to reassert vigor.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief