Global| Oct 19 2016

Global| Oct 19 2016Japan's Sector Indices Creep Ahead at Creepy Slow Speed

Summary

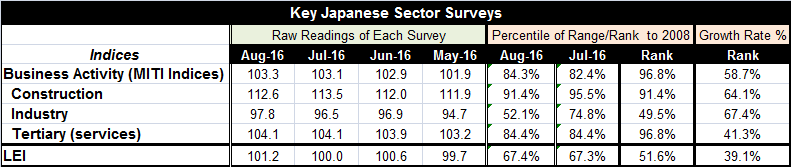

The chart presents the three main sectors: (1) mining and manufacturing, (2) construction and (3) services (tertiary) as year-on-year growth rates. Since early in 2015, the growth rates of all three sectors have been exceptionally [...]

The chart presents the three main sectors: (1) mining and manufacturing, (2) construction and (3) services (tertiary) as year-on-year growth rates. Since early in 2015, the growth rates of all three sectors have been exceptionally flat. The 12-month volatility of the three indices is exceptional ranking in the lower 13% of its queue of such variability measures (standard deviations calculated overall over all overlapping 12-month periods back to January 2010). The LEI in fact expressed as a growth rate has exhibited the least variation in its history back to 2010 while the overall business activity index has been more tranquil on only one occasion (out of 80).

The chart presents the three main sectors: (1) mining and manufacturing, (2) construction and (3) services (tertiary) as year-on-year growth rates. Since early in 2015, the growth rates of all three sectors have been exceptionally flat. The 12-month volatility of the three indices is exceptional ranking in the lower 13% of its queue of such variability measures (standard deviations calculated overall over all overlapping 12-month periods back to January 2010). The LEI in fact expressed as a growth rate has exhibited the least variation in its history back to 2010 while the overall business activity index has been more tranquil on only one occasion (out of 80).

This lack of variability in the overall sector index and LEI growth rates is not indicative of a dynamic economic situation. I have calculated six-month averages of the year-on-year growth rates and find that the current sector growth rates all average in the lower 12.5% of their historic queue of values (back to January 2010) or rank even lower. For construction as well as the overall business activity index, the six-month average of year-on-year growth has never been lower. The Japanese economy is doing next to nothing and is stuck there doing that month in and month out.

None of the policy moves made by the Bank of Japan have had any impact on any of the sector growth rates. This is an exceedingly depressing picture of Japan's economy especially because it reflects all major sectors and the behavior of the LEI as well. Also the deviation from the overall sector average growth has been very small. This month the summed absolute value of all sector deviations from the overall average ranks as the seventh smallest back to January 2010 and only the previous six months of this year have had smaller average deviations.

These statistics are simply devices to point out that the whole economy is moving in a very tight lock-step and it's a very slow pace. The BOJ is trying to jolt the economy into growth and to create some inflation, but there is no leverage for it to gain from any sector. Japan is also plugged into an international economy that has many of the same characteristics slowing down with differences among countries' growth rates diminishing.

China reported a 6.7% growth rate over night; it was about as expected. Its industrial sector was a bit weaker than expected. China is important to Japan as its largest trading partner. There is no evidence from China's GDP report that there will be any added stimulus coming from that direction. On balance, it leaves Japan to rely on its own abilities to generate growth. And it is very hard to use money supply growth as a tool to fight the impact of a shrinking population. The fact seems to be that Japan is relentlessly slowing down and that slowdown is dragging the price level along with it. The BOJ has a huge struggle ahead of it, trying to arrest the weakness in price as Japan's population shrinks and puts downward pressure on all sorts of prices and sector growth rates across the economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief