Global| Mar 29 2016

Global| Mar 29 2016Japan's Retail Sales on Slippery Slope

Summary

Not seasonally adjusted Japanese retail sales rose, but after seasonal adjustment they fell and on that basis they are progressively weakening from 12-months to six-months to three-months. All those growth rates on seasonally adjusted [...]

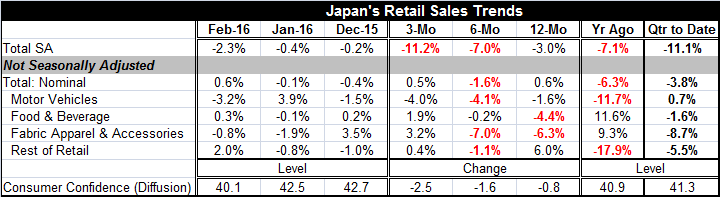

Not seasonally adjusted Japanese retail sales rose, but after seasonal adjustment they fell and on that basis they are progressively weakening from 12-months to six-months to three-months. All those growth rates on seasonally adjusted data are in fact negative. And on a quarter-to-date basis, two months into the quarter, Japanese seasonally adjusted retail sales are falling at an 11.1% annualized rate in Q1 2016.

Not seasonally adjusted Japanese retail sales rose, but after seasonal adjustment they fell and on that basis they are progressively weakening from 12-months to six-months to three-months. All those growth rates on seasonally adjusted data are in fact negative. And on a quarter-to-date basis, two months into the quarter, Japanese seasonally adjusted retail sales are falling at an 11.1% annualized rate in Q1 2016.

Accompanying the drop and deceleration in retail sales is a withering consumer confidence reading. Confidence has eroded to 40.1 in February from 42.5 in January. It is net lower over three-months, six-months and 12-months. The ongoing drop in confidence gives substance to the ongoing drop in retail sales. Consumer attitudes are deteriorating and so is the consumer's propensity to spend.

Unemployment rose in Japan in February, edging up to 3.3% from 3.2%. The 3.3% unemployment rate reverses the one-month drop to 3.2% that was logged in January. Prior to that, the rate had been at 3.3% for two months running. There is no real sense that the unemployment rate is on a new trend move. It has been fluctuating in this range for some months now.

Japan's inflation rate continues to be low in February. The index did rise by 0.3% month-on-month but is up just by 0.3% over 12-months. Japan cannot seem to get into a positive inflation space even after several years of trying and after having launched Abenomics.

Recent Japanese economic readings have been showing weakness. Japanese exports in February fell by 2.4% month-to-month and are accelerating their drop with a -12.9% growth rate over three-months in place. The manufacturing PMI slipped in February to 50.1 from 52.3 in January, its weakest level since June of last year. Japan's service business activity index also fell in February to 51.2 from 52.4 in January to its weakest standing since March 2015. The economy watchers gauge, another service sector barometer, has slipped. But today the small business confidence index showed an unenthusiastic rebound.

On balance, there seems to be an overall loss of momentum in Japan from the factory sector to services to consumer spending and confidence with export flows weakening. This is a pretty full slate of economic weakness. The BOJ does have a relatively new program of negative interest rates in play, but it was not well-received when it was announced. It is not clear that the program is having its intended effect. In Japan, where there is a long tradition of currency usage, the sales of safes have gone up as people have taken to hoarding cash at home to avoid the evils of negative rates at banks. Japan continues to struggle with poor trends in play, few policy levers left to pull and important trade ties to China in place where growth has been faltering. The prognosis is not upbeat.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief