Global| Jul 29 2019

Global| Jul 29 2019Japan's Retail Sales Draw A Blank

Summary

Japan's economy is in the process of navigating a number of potentially wicked twists and turns of fate, some of its own making and some thrust upon it in a region gone topsy turvy. For now retail sales are edging higher year-on-year [...]

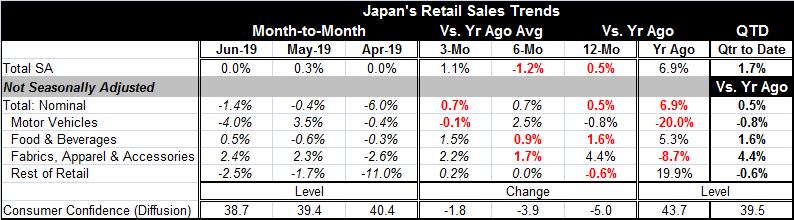

Japan's economy is in the process of navigating a number of potentially wicked twists and turns of fate, some of its own making and some thrust upon it in a region gone topsy turvy. For now retail sales are edging higher year-on-year at a 0.5% pace with a 1.1% annualized growth rate over the last three months. Growth is hanging in there by its fingernails. In June, retail sales growth went dead flat after rising by 0.3% in May and being dead flat in April. Still, with those results, retail sales also are rising at a 1.7% annual rate in the just completed quarter.

Japan faces challengesJapan's population series has a discontinuity in it. But the message is clear that Japan's population is still shrinking. That puts downward pressure on any macroeconomic indicator that Japan reports. Japan also just concluded a national election in which Mr. Abe was returned to office. Despite the unpopularity of his proposed sales tax hike, Abe won with a striking but not overpowering or controlling majority. The Japanese people are not happy about the consumption tax hike that has been postponed but will now go ahead. Yet, the people seem to agree with the Prime Minister that it is a fiscal necessity because of the huge stock of public debt. So they returned him to office despite the plan. The Bank of Japan, of course, still has its extraordinary measures in play. It meets this week ahead of the Fed and will make a policy decision that will have to anticipate what the Fed will do at a time that the Fed is widely believed to be on the brink of its first rate cut in over a decade.

Economic cross currents

Beyond these considerations, Japan has been fighting deflation, disinflation, the ‘zero bound' and weak growth for a decade. In addition to that battle, it has to weather the trade war between its two largest trade partners, the United States and China and risk whatever collateral damage may come of that. Japan has yet to settle its own trade situation with the Trump Administration.

Old issues break anew

Japan and South Korea are in a revival of old WWII disputes that have spilled over into the trade arena and led to retaliatory trade restrictions by Japan that South Korea is protesting stemming Japan's use of forced Korean labor during WWII. Late last year, this old wound was reopened when a South Korean court ordered a Japanese steel firm to pay reparations to Korean forced laborers used during WWII. Japan believes that a post war agreement settled claims for damages sought over the country's former ‘colonial' conquests; yet debate over compensation and reparations obviously has not been eliminated. A South Korean court saying a corporation is responsible for forced labor and that restitution must be paid, no matter what governments have agreed is a real fly in the ointment of international cooperation. In retaliation, Japan has set certain trade restrictions that could hobble the South Korean tech industry and it also plans to remove South Korea from a "white" list of countries with minimum trade restrictions, requiring Japanese exporters to go through a lengthy permit application process each time they want to export restricted items to South Korea. None of this is good for trade or growth let alone mutual cooperation in the region.

At the same time, there are renewed conflicts over a tiny group of disputed islands claimed by South Korea and Japan in the Sea of Japan or the East Sea. South Korea and Japan accused Russia of violating their airspace after Russian A-50 airplane early warning and control aircraft entered airspace claimed by both Seoul and Tokyo. South Korea's Defense Ministry said its jets fired 360 warning shots after the Russian bomber flew over the Dokdo islets, called Takeshima by Japan, which also claims them. Two Chinese warplanes also entered South Korea's air defense identification zone on that same day. Russia denied there was an incursion or any weapons firing.

To add a bit more weirdness to this circumstance, Japanese Foreign Minister Taro Kono said: "It is Japan that should take action against the Russian plane that entered its airspace. It is incompatible with Japan's stance that South Korea takes steps on that" (Source here).

It seems that no old squabble is too old or too small or too meaningless to become an international event. Thanks to Donald Trump, old disputes no long simply fester they manifest themselves as trade restrictions. They are the way to get attention and action for a dispute.

For its part, China is getting ready to run naval drills in the region near Taiwan in the wake of U.S. plans to sell arms to Taiwan. China has asserted that any interference with China's claim on Taiwan would be met as an act of war. It could be that the ongoing unrest and rioting in Hong Kong has made China feel that it must begin to draw some hardlines over important issues.

Under these economic and geopolitical circumstances with North Korea having tested a missile again, it is hard to call the Asian situation stable. And yet it is no more unstable than it has been in other respects. It is at this point unclear what South Korea really wants from Japan or why. The precipitating action on forced labor came from a court decision not from the South Korean government so it may be a bit out of control. But the islands alleged overflight came as Russia and China began to launch joint missions in the region, a new development. And it is clear that Japan feels that this WWII episode has been long closed has no desire to deal with it again in any way. That explains why it has shut the door on such important tradeable goods to South Korea so hard and so firmly and seemingly so unequivocally. Europe has its Brexit. Asia now has its rival to it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief